Exam 24: Portfolio Performance Evaluation

Exam 1: The Investment Environment51 Questions

Exam 2: Financial Markets, Asset Classes and Financial Instruments82 Questions

Exam 3: How Securities Are Traded65 Questions

Exam 4: Mutual Funds and Other Investment Companies59 Questions

Exam 5: Risk, Return, and the Historical Record64 Questions

Exam 6: Capital Allocation to Risky Assets59 Questions

Exam 7: Optimal Risky Portfolios63 Questions

Exam 8: Index Models76 Questions

Exam 9: The Capital Asset Pricing Model71 Questions

Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return62 Questions

Exam 11: The Efficient Market Hypothesis42 Questions

Exam 12: Behavioural Finance and Technical Analysis41 Questions

Exam 13: Empirical Evidence on Security Returns41 Questions

Exam 14: Bond Prices and Yields110 Questions

Exam 15: The Term Structure of Interest Rates58 Questions

Exam 16: Managing Bond Portfolios69 Questions

Exam 17: Macroeconomic and Industry Analysis67 Questions

Exam 18: Equity Valuation Models106 Questions

Exam 19: Financial Statement Analysis71 Questions

Exam 20: Options Markets: Introduction88 Questions

Exam 21: Option Valuation85 Questions

Exam 22: Futures Markets85 Questions

Exam 23: Futures, Swaps, and Risk Management51 Questions

Exam 24: Portfolio Performance Evaluation68 Questions

Exam 25: International Diversification48 Questions

Exam 26: Hedge Funds46 Questions

Exam 27: The Theory of Active Portfolio Management48 Questions

Exam 28: Investment Policy and the Framework of the Cfa Institute76 Questions

Select questions type

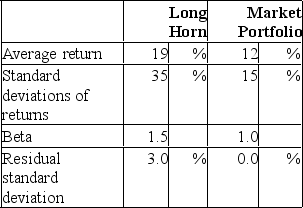

The following data are available relating to the performance of Long Horn Stock Fund and the market portfolio:  The risk-free return during the sample period was 6%.

What is the Sharpe measure of performance evaluation for Long Horn Stock Fund?

The risk-free return during the sample period was 6%.

What is the Sharpe measure of performance evaluation for Long Horn Stock Fund?

(Multiple Choice)

4.9/5  (43)

(43)

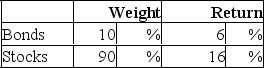

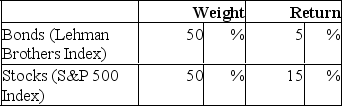

In a particular year, Aggie Mutual Fund earned a return of 15% by making the following investments in the following asset classes:  The return on a bogey portfolio was 10%, calculated as follows:

The return on a bogey portfolio was 10%, calculated as follows:

The contribution of asset allocation across markets to the total excess return was

The contribution of asset allocation across markets to the total excess return was

(Multiple Choice)

4.7/5 (35)

Suppose the risk-free return is 4%.The beta of a managed portfolio is 1.2, the alpha is 1%, and the average return is 14%.Based on Jensen's measure of portfolio performance, you would calculate the return on the market portfolio as

(Multiple Choice)

4.8/5 (30)

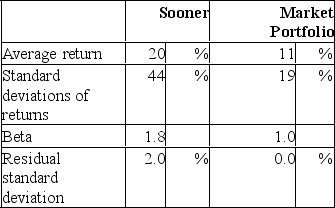

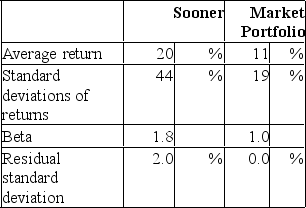

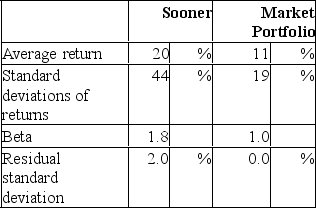

The following data are available relating to the performance of Sooner Stock Fund and the market portfolio:  The risk-free return during the sample period was 3%.

What is the Sharpe measure of performance evaluation for Sooner Stock Fund?

The risk-free return during the sample period was 3%.

What is the Sharpe measure of performance evaluation for Sooner Stock Fund?

(Multiple Choice)

4.9/5 (37)

Suppose you purchase one share of the stock of Volatile Engineering Corporation at the beginning of year 1 for $36.At the end of year 1, you receive a $2 dividend and buy one more share for $30.At the end of year 2, you receive total dividends of $4 (i.e., $2 for each share) and sell the shares for $36.45 each.The dollar-weighted return on your investment is

(Multiple Choice)

4.9/5 (41)

Hedge funds I) are appropriate as a sole investment vehicle for an investor.

II. should only be added to an already well-diversified portfolio.

III. pose performance-evaluation issues due to nonlinear factor exposures.

IV. have down-market betas that are typically larger than up-market betas.

V. have symmetrical betas.

(Multiple Choice)

4.8/5 (30)

The following data are available relating to the performance of Sooner Stock Fund and the market portfolio:  The risk-free return during the sample period was 3%.

Calculate the information ratio for Sooner Stock Fund.

The risk-free return during the sample period was 3%.

Calculate the information ratio for Sooner Stock Fund.

(Multiple Choice)

4.8/5 (40)

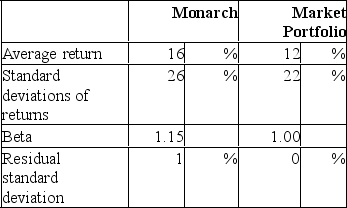

The following data are available relating to the performance of Monarch Stock Fund and the market portfolio:  The risk-free return during the sample period was 4%.

Calculate Sharpe's measure of performance for Monarch Stock Fund.

The risk-free return during the sample period was 4%.

Calculate Sharpe's measure of performance for Monarch Stock Fund.

(Multiple Choice)

4.8/5 (42)

Suppose two portfolios have the same average return and the same standard deviation of returns, but Aggie Fund has a lower beta than Raider Fund.According to the Treynor measure, the performance of Aggie Fund

(Multiple Choice)

4.8/5 (39)

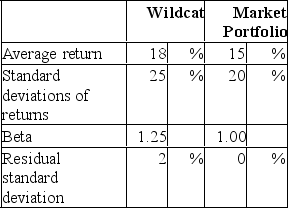

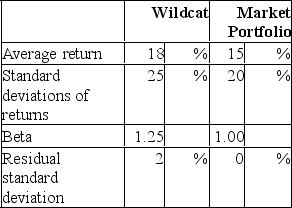

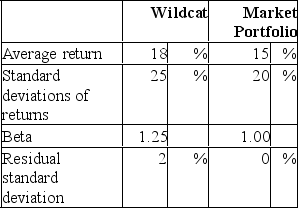

The following data are available relating to the performance of Wildcat Fund and the market portfolio:  The risk-free return during the sample period was 7%.

What is the information ratio measure of performance evaluation for Wildcat Fund?

The risk-free return during the sample period was 7%.

What is the information ratio measure of performance evaluation for Wildcat Fund?

(Multiple Choice)

4.9/5 (31)

The following data are available relating to the performance of Wildcat Fund and the market portfolio:  The risk-free return during the sample period was 7%.

Calculate Treynor's measure of performance for Wildcat Fund.

The risk-free return during the sample period was 7%.

Calculate Treynor's measure of performance for Wildcat Fund.

(Multiple Choice)

4.9/5 (32)

The following data are available relating to the performance of Sooner Stock Fund and the market portfolio:  The risk-free return during the sample period was 3%.

What is the Treynor measure of performance evaluation for Sooner Stock Fund?

The risk-free return during the sample period was 3%.

What is the Treynor measure of performance evaluation for Sooner Stock Fund?

(Multiple Choice)

4.9/5 (30)

Rodney holds a portfolio of risky assets that represents his entire risky investment.To evaluate the performance of Rodney's portfolio, in which order would you complete the steps listed? I) Compare the Sharpe measure of Rodney's portfolio to the Sharpe measure of the best portfolio.

II) State your conclusions.

III) Assume that past security performance is representative of expected performance.

IV) Determine the benchmark portfolio that Rodney would have held if he had chosen a passive strategy.

(Multiple Choice)

4.8/5 (35)

Risk-adjusted mutual fund performance measures have decreased in popularity because

(Multiple Choice)

4.7/5 (33)

Suppose the risk-free return is 3%.The beta of a managed portfolio is 1.75, the alpha is 0%, and the average return is 16%.Based on Jensen's measure of portfolio performance, you would calculate the return on the market portfolio as

(Multiple Choice)

4.8/5 (24)

The following data are available relating to the performance of Wildcat Fund and the market portfolio:  The risk-free return during the sample period was 7%.

Calculate Jensen's measure of performance for Wildcat Fund.

The risk-free return during the sample period was 7%.

Calculate Jensen's measure of performance for Wildcat Fund.

(Multiple Choice)

4.9/5 (39)

Suppose two portfolios have the same average return and the same standard deviation of returns, but Buckeye Fund has a lower beta than Gator Fund.According to the Sharpe measure, the performance of Buckeye Fund

(Multiple Choice)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)