Exam 2: Mathematical and Statistical Foundations

Exam 1: Introduction12 Questions

Exam 2: Mathematical and Statistical Foundations9 Questions

Exam 3: A Brief Overview of the Classical Linear Regression Model28 Questions

Exam 4: Further Development and Analysis of the Classical Linear Regression Model25 Questions

Exam 5: Classical Linear Regression Model Assumptions and Diagnostic Tests20 Questions

Exam 6: Univariate Time Series Modelling and Forecasting29 Questions

Exam 7: Multivariate Models30 Questions

Exam 8: Modelling Long-Run Relationships in Finance18 Questions

Exam 9: Modelling Volatility and Correlation22 Questions

Exam 10: Switching Models19 Questions

Exam 11: Panel Data and Limited Dependent Variable Models12 Questions

Select questions type

Threshold autoregressive and Markov switching models:

Free

(Multiple Choice)

4.7/5  (41)

(41)

Correct Answer: Verified

Verified

A

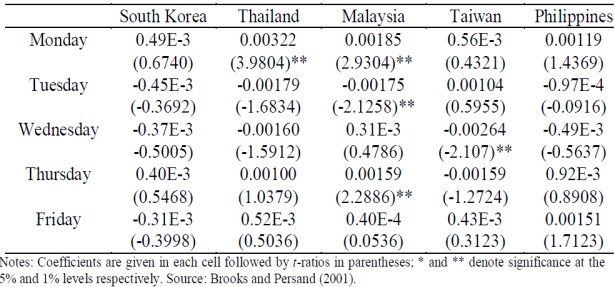

To check for seasonality (day-of-the-week effect) in stock returns of South Korea, Malaysia, the Philippines, Taiwan and Thailand, Brooks and Persand (2001) regress daily returns in each of these countries' stock market on five dummy variables D1 to D5 representing each day of the week i.e. D1 for Mondays, D2 for Tuesdays, D3 for Wednesdays, D4 for Thursdays and D5 for Fridays:  Their results were:

Their results were:  -Which market(s) did not display any evidence of day-of-the-week effect?

-Which market(s) did not display any evidence of day-of-the-week effect?

Free

(Multiple Choice)

4.8/5 (47)

Correct Answer:Verified

D

If a series possesses the "Markov property", what would this imply?

(I) The series is path-dependent

(ii) All that is required to produce forecasts for the series is the current value of the series plus a transition probability matrix

(iii) The state-determining variable must be observable

(iv) The series can be classified as to whether it is in one regime or another regime, but it can only be in one regime at any one time

Free

(Multiple Choice)

4.9/5 (31)

Correct Answer:Verified

A

Which of these equations is a self-exciting threshold autoregressive model?

(Multiple Choice)

4.8/5 (39)

The unknown parameters of a Markov switching model are usually estimated using:

(Multiple Choice)

4.8/5 (38)

The key difference between threshold autoregressive and Markov switching models is that:

(Multiple Choice)

4.8/5 (41)

Suppose that a researcher wishes to test for calendar (seasonal) effects using a dummy variables approach. Which of the following regressions could be used to examine this?

(I) A regression containing intercept dummies

(ii) A regression containing slope dummies

(iii) A regression containing intercept and slope dummies

(iv) A regression containing a dummy variable taking the value 1 for one observation and zero for all others

(Multiple Choice)

4.9/5 (32)

To compare the goodness of fit of Markov switching and threshold autoregressive models with linear models, one can compare the residual sums of squares of the two types of models using an F-test. Is the statement true?

(Multiple Choice)

4.9/5 (48)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)