Exam 9: Modelling Volatility and Correlation

Exam 1: Introduction12 Questions

Exam 2: Mathematical and Statistical Foundations9 Questions

Exam 3: A Brief Overview of the Classical Linear Regression Model28 Questions

Exam 4: Further Development and Analysis of the Classical Linear Regression Model25 Questions

Exam 5: Classical Linear Regression Model Assumptions and Diagnostic Tests20 Questions

Exam 6: Univariate Time Series Modelling and Forecasting29 Questions

Exam 7: Multivariate Models30 Questions

Exam 8: Modelling Long-Run Relationships in Finance18 Questions

Exam 9: Modelling Volatility and Correlation22 Questions

Exam 10: Switching Models19 Questions

Exam 11: Panel Data and Limited Dependent Variable Models12 Questions

Select questions type

Assume that you are trying to model the relationship between house prices and rents. If you find that both series are non-stationary and a linear combination of the two series is stationary, which of the following is true?

(I) Regressing the levels of house prices on the levels of rents could lead to spurious regressions

(II) House prices and rents are cointegrated

(III) An appropriate linear combination of house prices and rents is I(1)

(IV) House prices and rents are not cointegrated

Free

(Multiple Choice)

4.8/5  (28)

(28)

Correct Answer: Verified

Verified

B

Consider the following matrix:  What are its characteristic roots?

What are its characteristic roots?

Free

(Multiple Choice)

4.9/5 (25)

Correct Answer:Verified

A

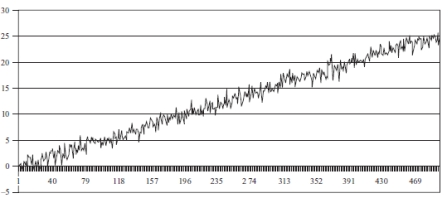

The plotted series in the following graph is an example of a:

Free

(Multiple Choice)

4.8/5 (43)

Correct Answer:Verified

B

Which one of the following best describes most series of asset prices?

(Multiple Choice)

4.8/5 (26)

To induce stationarity in a deterministic trend-stationary process

(Multiple Choice)

4.9/5 (31)

Which criticism of Dickey-Fuller (DF) -type tests is addressed by stationarity tests, such as the KPSS test?

(Multiple Choice)

4.8/5 (40)

Which of the following are problems associated with the Engle-Granger approach to modelling using cointegrated data?

(I) The coefficients in the cointegrating relationship are hard to calculate

(ii) This method requires the researcher to assume that one variable is the dependent variable and the others are independent variables

(iii) The Engle-Granger technique can only detect one cointegrating relationship

(iv) Engle-Granger does not allow the testing of hypotheses involving the actual cointegrating relationship.

(Multiple Choice)

4.9/5 (45)

Consider the following vector error correction (VECM) model: yt =  yt-5 +

yt-5 +  1 yt-1 + 11efcd90_39fd_be4b_b057_81d80004b874_TB7071_002 yt-2 + 11efcd90_39fd_be4b_b057_81d80004b874_TB7071_003 yt-3 + 11efcd90_39fd_be4b_b057_81d80004b874_TB7071_004 yt-4 + ut

Where yt is a k* 1 vector of variables, and ut is a k* 1 vector of disturbances.

Which of the following statements is true of the VECM?

1 yt-1 + 11efcd90_39fd_be4b_b057_81d80004b874_TB7071_002 yt-2 + 11efcd90_39fd_be4b_b057_81d80004b874_TB7071_003 yt-3 + 11efcd90_39fd_be4b_b057_81d80004b874_TB7071_004 yt-4 + ut

Where yt is a k* 1 vector of variables, and ut is a k* 1 vector of disturbances.

Which of the following statements is true of the VECM?

(Multiple Choice)

4.9/5 (35)

If there are three variables that are being tested for cointegration, what is the maximum number of linearly independent cointegrating relationships that there could be?

(Multiple Choice)

4.8/5 (49)

Consider the testing of hypotheses concerning the cointegrating vector(s) under the Johansen approach. Which of the following statements is correct?

(Multiple Choice)

5.0/5 (36)

Which of the following are probably valid criticisms of the Dickey Fuller methodology?

(I) The tests have a unit root under the null hypothesis and this may not be rejected due to insufficient information in the sample

(ii) the tests are poor at detecting a stationary process with a unit root close to the non-stationary boundary

(iii) the tests are highly complex to calculate in practice

(iv) the tests have low power in small samples

(Multiple Choice)

4.8/5 (36)

A researcher would like to test for a unit root in a series. She runs the regression . What should her null hypothesis be assuming that she adopts the Dickey-Fuller test approach?

(Multiple Choice)

4.8/5 (38)

If the number of non-zero eigenvalues of the pi matrix under a Johansen test is 2, this implies that

(Multiple Choice)

4.8/5 (40)

Assuming the researcher in question 19 would like to run an augmented Dickey-Fuller test instead. What is the appropriate regression she would have to run and the null hypothesis of the test?

(Multiple Choice)

4.8/5 (38)

What is the impact of shocks to an AR(1) with no drift if ?

(Multiple Choice)

4.9/5 (29)

Which of the following are consequences of using non-stationary data in regressions?

(I) Shocks will be persistent

(II) It can lead to spurious regressions

(III) t-ratios will not follow a t-distribution

(IV) F-Statistic will not follow an F-distribution

(Multiple Choice)

4.8/5 (27)

What is the impact of shocks to an AR(1) with no drift if ?

(Multiple Choice)

4.9/5 (33)

You have the following data for Johansen's max rank test for cointegration between 4 international equity market indices:  How many cointegrating vectors are there?

How many cointegrating vectors are there?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)