Exam 20: An Introduction to Derivative Markets and Securities

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

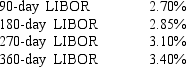

Exhibit 21.12

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Suppose you are a loan officer for a commercial bank and one of your clients has just approached you about a one-year loan for $4,000,000. Interest on the new loan will be paid at the end of each quarter based on the prevailing level of LIBOR at the beginning of each quarter. The LIBOR yield curve in the cash market is as follows:

-The forward market has low liquidity relative to the futures market.

-The forward market has low liquidity relative to the futures market.

(True/False)

4.9/5  (45)

(45)

Exhibit 20.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The current stock price of ABC Corporation is $53.50. ABC Corporation has the following put and call option prices that expire 6 months from today. The risk-free rate of return is 5% and the expected return on the market is 11%.

-You own a call option and put option that both have the same exercise price of $50 and their respective prices are $4 and $3. The stock is currently trading at $60. Calculate the dollar return on this strategy.

-You own a call option and put option that both have the same exercise price of $50 and their respective prices are $4 and $3. The stock is currently trading at $60. Calculate the dollar return on this strategy.

(Multiple Choice)

4.9/5 (37)

Exhibit 20.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

December futures on the S&P 500 stock index trade at 250 times the index value of 1187.70. Your broker requires an initial margin of 10% percent on futures contracts. The current value of the S&P 500 stock index is 1178.

-Refer to Exhibit 20.1. Calculate the return on a cash investment in the S&P 500 stock index if the ending index value is 1170 over the same time period.

(Multiple Choice)

4.8/5 (36)

A one year call option has a strike price of 60, expires in 6 months, and has a price of $2.5. If the risk free rate is 7%, and the current stock price is $55, what should the corresponding put be worth?

(Multiple Choice)

4.9/5 (42)

Exhibit 20.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Sarah Kling bought a 6-month Peppy Cola put option with an exercise price of $55 for a premium of $8.25 when Peppy was selling for $48.00 per share.

-Refer to Exhibit 20.5. What is Sarah's annualized gain/loss?

(Multiple Choice)

4.9/5 (32)

If an investor wants to acquire the right to buy or sell an asset, but not the obligation to do it, the best instrument is an option rather than a futures contract.

(True/False)

4.9/5 (42)

The payoffs diagrams to both long and short positions in a forward contract are asymmetrical around the contract price.

(True/False)

4.8/5 (30)

Exhibit 20.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Sarah Kling bought a 6-month Peppy Cola put option with an exercise price of $55 for a premium of $8.25 when Peppy was selling for $48.00 per share.

-A stock currently trades at $110. June put options on the stock with a strike price of $100 are priced at $5.25. Calculate the dollar return on one put contract.

(Multiple Choice)

4.9/5 (33)

Exhibit 20.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

A futures contract on Treasury bond futures with a December expiration date currently trade at 103:06. The face value of a Treasury bond futures contract is $100,000. Your broker requires an initial margin of 10%.

-Refer to Exhibit 20.2. Calculate the initial margin deposit.

(Multiple Choice)

4.7/5 (40)

Consider a stock that is currently trading at $10. Calculate the intrinsic value for a call option that has an exercise price of $15.

(Multiple Choice)

4.7/5 (40)

The price paid for the option contract is referred to as the

(Multiple Choice)

4.9/5 (42)

A vertical spread involves buying and selling call options in the same stock with

(Multiple Choice)

4.9/5 (28)

Exhibit 20.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The current stock price of Zanco Corporation is $50. Zanco Corporation has the following put and call option prices with exercise prices at $45 and $50.

-Refer to Exhibit 20.7. The intrinsic value for the put option with a $50 exercise price is

-Refer to Exhibit 20.7. The intrinsic value for the put option with a $50 exercise price is

(Multiple Choice)

4.8/5 (42)

There are a number of differences between forward and futures contracts. Which of the following statements is false?

(Multiple Choice)

4.9/5 (48)

Futures contracts are slower to absorb new information than forward contracts.

(True/False)

4.9/5 (37)

A put option is in the money if the current market price is above the strike price.

(True/False)

4.8/5 (40)

An option to sell an asset is referred to as a call, whereas an option to buy an asset is called a put.

(True/False)

4.9/5 (30)

You own a stock that has risen from $10 per share to $32 per share. You wish to delay taking the profit but you are troubled about the short run behavior of the stock market. An effective action on your part would be to

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)