Exam 3: Where Prices Come From: the Interaction of Demand and Supply

Exam 1: Economics: Foundations and Models459 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System492 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply476 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes420 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods262 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply293 Questions

Exam 7: The Economics of Health Care337 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance512 Questions

Exam 9: Comparative Advantage and the Gains From International Trade377 Questions

Exam 10: Consumer Choice and Behavioral Economics304 Questions

Exam 11: Technology, Production, and Costs326 Questions

Exam 12: Firms in Perfectly Competitive Markets296 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting272 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets256 Questions

Exam 15: Monopoly and Antitrust Policy279 Questions

Exam 16: Pricing Strategy258 Questions

Exam 17: The Markets for Labor and Other Factors of Production279 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: Gdp: Measuring Total Production and Income260 Questions

Exam 20: Unemployment and Inflation290 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles251 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies261 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run305 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis286 Questions

Exam 25: Money, Banks, and the Federal Reserve System278 Questions

Exam 26: Monetary Policy280 Questions

Exam 27: Fiscal Policy313 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy277 Questions

Exam 30: The International Financial System258 Questions

Select questions type

An increase in input costs in the production of electric automobiles caused the price of electric automobiles to rise. Holding everything else constant, how would this affect the market for gasoline-powered automobiles (a substitute for electric automobiles)?

(Multiple Choice)

4.7/5  (37)

(37)

The following appeared in a Florida newspaper a week after a hurricane hit the state. "Floridians are relieved that the storm produced no fatalities but homeowners face weeks, if not months, of rebuilding. Matters are made worse by the soaring prices of plywood and other building materials that always follow in a hurricane's path. Complaints of profiteering and price gouging have not deterred firms from raising their prices by over 100 percent." Which of the following offers the best explanation for the price increases referred to in the article?

(Multiple Choice)

4.8/5 (42)

A decrease in the equilibrium price for a product will result

(Multiple Choice)

4.9/5 (37)

Assume that microbrewery beer is a normal good. Prices of microbrewery beer have risen steadily in recent years. Over this same period, prices for fermenting vats used in beer making have also risen and consumer incomes have fallen. Which of the following best explains the rising prices of microbrewery beer?

(Multiple Choice)

4.8/5 (35)

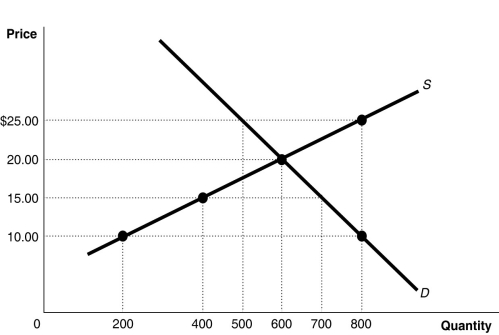

Figure 3-4  -Refer to Figure 3-4. At a price of $20, how many units will be supplied?

-Refer to Figure 3-4. At a price of $20, how many units will be supplied?

(Multiple Choice)

4.8/5 (38)

From a supply perspective, what impact would an increase in the price of motorcycles have on the market for motorcycles?

(Essay)

4.9/5 (33)

For each of the following pairs of products, state which are complements, which are substitutes, and which are unrelated.

a. Digital camera and memory card

b. 7Up and Mountain Dew

c. Swimsuits and flip-flops

d. Tylenol and cat food

e. Photocopier and paper

(Essay)

4.9/5 (37)

How does the decreasing use of traditional cameras affect the market for traditional camera film?

(Multiple Choice)

4.9/5 (40)

Which of the following would cause the equilibrium price of ketchup to increase and the equilibrium quantity of ketchup to decrease?

(Multiple Choice)

4.9/5 (38)

In recent years the cost of producing wines in the U.S. has increased largely due to rising rents for vineyards. At the same time, more and more Americans prefer wine over beer. Which of the following best explains the effect of these events in the wine market?

(Multiple Choice)

4.8/5 (44)

An increase in the price of off-road vehicles will result in

(Multiple Choice)

4.8/5 (29)

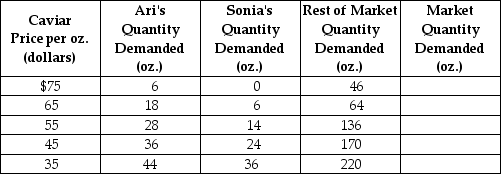

Table 3-2

-Refer to Table 3-2. The table above shows the demand schedules for caviar of two individuals (Ari and Sonia) and the rest of the market. At a price of $55, the quantity demanded in the market would be

-Refer to Table 3-2. The table above shows the demand schedules for caviar of two individuals (Ari and Sonia) and the rest of the market. At a price of $55, the quantity demanded in the market would be

(Multiple Choice)

4.9/5 (45)

How has the growing popularity of factory outlet stores affected the market for clothing at retail department stores?

(Multiple Choice)

5.0/5 (42)

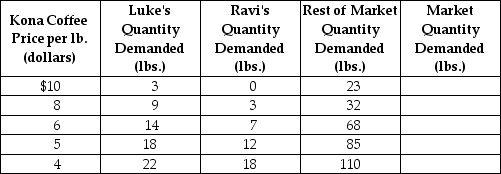

Table 3-3

-Refer to Table 3-3. The table above shows the demand schedules for Kona coffee of two individuals (Luke and Ravi) and the rest of the market. At a price of $6, the quantity demanded in the market would be

-Refer to Table 3-3. The table above shows the demand schedules for Kona coffee of two individuals (Luke and Ravi) and the rest of the market. At a price of $6, the quantity demanded in the market would be

(Multiple Choice)

4.8/5 (45)

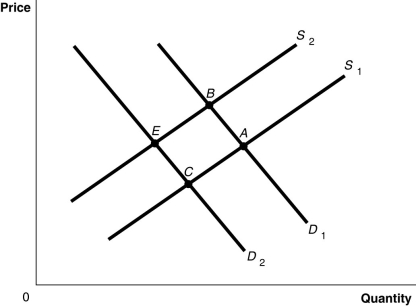

Figure 3-8  -Refer to Figure 3-8. The graph in this figure illustrates an initial competitive equilibrium in the market for motorcycles at the intersection of D2 and S1 (point C). If the price of motorcycle side cars (a complement to motorcycles) decreases, and the wages of motorcycle workers increase, how will the equilibrium point change?

-Refer to Figure 3-8. The graph in this figure illustrates an initial competitive equilibrium in the market for motorcycles at the intersection of D2 and S1 (point C). If the price of motorcycle side cars (a complement to motorcycles) decreases, and the wages of motorcycle workers increase, how will the equilibrium point change?

(Multiple Choice)

4.9/5 (41)

Explain the differences between a change in supply and a change in quantity supplied.

(Essay)

4.8/5 (35)

A change in quantity supplied is represented by a movement along the supply curve.

(True/False)

4.8/5 (29)

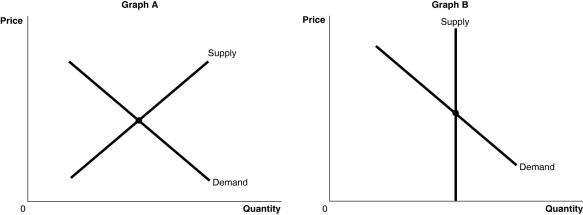

Figure 3-3  -Refer to Figure 3-3. The figure above shows the supply and demand curves for two markets: the market for an original Picasso painting and the market for designer jeans. Which graph most likely represents which market?

-Refer to Figure 3-3. The figure above shows the supply and demand curves for two markets: the market for an original Picasso painting and the market for designer jeans. Which graph most likely represents which market?

(Multiple Choice)

4.8/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)