Exam 12: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements

Exam 7: Intercompany Transfers of Services and Noncurrent Assets47 Questions

Exam 8: Intercompany Indebtedness39 Questions

Exam 8: Appendix a Intercompany Indebtedness40 Questions

Exam 9: Consolidation Ownership Issues51 Questions

Exam 10: Additional Consolidation Reporting Issues44 Questions

Exam 11: Multinational Accounting: Foreign Currency Transactions and Financial Instruments62 Questions

Exam 12: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements65 Questions

Exam 13: Segment and Interim Reporting61 Questions

Exam 14: Sec Reporting49 Questions

Exam 15: Partnerships: Formation, Operation, and Changes in Membership55 Questions

Exam 16: Partnerships: Liquidation59 Questions

Exam 17: Governmental Entities: Introduction and General Fund Accounting79 Questions

Exam 18: Governmental Entities: Special Funds and Governmentwide Financial Statements79 Questions

Exam 19: Not-For-Profit Entities121 Questions

Exam 20: Corporations in Financial Difficulty41 Questions

Select questions type

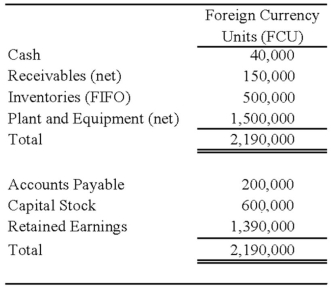

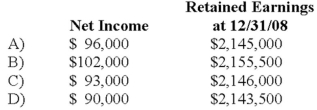

On January 2, 20X8, Johnson Company acquired a 100% interest in the capital stock of Perth Company for $3,100,000. Any excess cost over book value is attributable to a patent with a 10-year remaining life. At the date of acquisition, Perth's balance sheet contained the following information:  Perth's income statement for 20X8 is as follows:

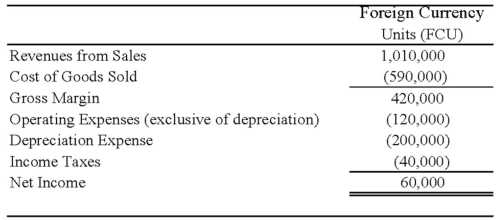

Perth's income statement for 20X8 is as follows:  The balance sheet of Perth at December 31, 20X8, is as follows:

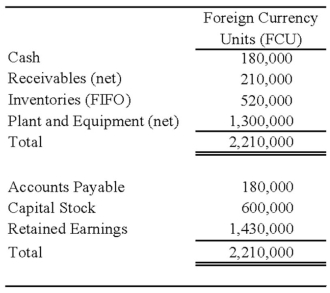

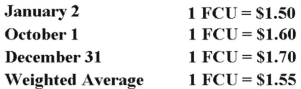

The balance sheet of Perth at December 31, 20X8, is as follows:  Perth declared and paid a dividend of 20,000 FCU on October 1, 20X8. Spot rates at various dates for 20X8 follow:

Perth declared and paid a dividend of 20,000 FCU on October 1, 20X8. Spot rates at various dates for 20X8 follow:  Assume Perth's revenues, purchases, operating expenses, depreciation expense, and income taxes were incurred evenly throughout 20X8.

Refer to the above information. Assuming the local currency of the country in which Perth Company is located is the functional currency, what are the translated amounts for the items below in U.S. dollars?

Assume Perth's revenues, purchases, operating expenses, depreciation expense, and income taxes were incurred evenly throughout 20X8.

Refer to the above information. Assuming the local currency of the country in which Perth Company is located is the functional currency, what are the translated amounts for the items below in U.S. dollars?

(Multiple Choice)

4.8/5  (34)

(34)

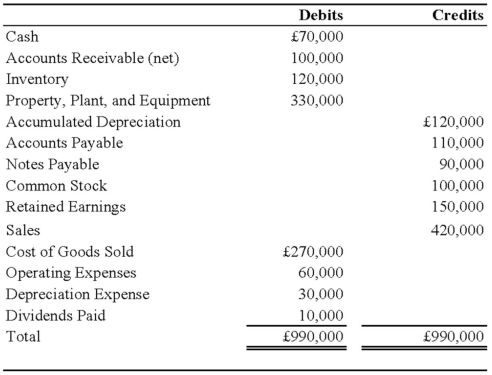

On January 1, 2008, Pace Company acquired all of the outstanding stock of Spin PLC, a British Company, for $350,000. Spin's net assets on the date of acquisition were 250,000 pounds (£). On January 1, 2008, the book and fair values of the Spin's identifiable assets and liabilities approximated their fair values except for property, plant, and equipment and trademarks. The fair value of Spin's property, plant, and equipment exceeded its book value by $25,000. The remaining useful life of Spin's equipment at January 1, 2008, was 10 years. The remainder of the differential was attributable to a trademark having an estimated useful life of 5 years. Spin's trial balance on December 31, 2008, in pounds, follows:  Additional Information

1. Spin uses the FIFO method for its inventory. The beginning inventory was acquired on December 31, 2007, and ending inventory was acquired on December 26, 2008. Purchases of £300,000 were made evenly throughout 2008.

2. Spin acquired all of its property, plant, and equipment on March 1, 2006, and uses straight-line depreciation.

3. Spin's sales were made evenly throughout 2008, and its operating expenses were incurred evenly throughout 2008.

4. The dividends were declared and paid on November 1, 2008.

5. Pace's income from its own operations was $150,000 for 2008, and its total stockholders' equity on January 1, 2008, was $1,000,000. Pace declared $50,000 of dividends during 2008.

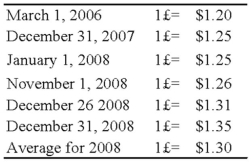

6. Exchange rates were as follows:

Additional Information

1. Spin uses the FIFO method for its inventory. The beginning inventory was acquired on December 31, 2007, and ending inventory was acquired on December 26, 2008. Purchases of £300,000 were made evenly throughout 2008.

2. Spin acquired all of its property, plant, and equipment on March 1, 2006, and uses straight-line depreciation.

3. Spin's sales were made evenly throughout 2008, and its operating expenses were incurred evenly throughout 2008.

4. The dividends were declared and paid on November 1, 2008.

5. Pace's income from its own operations was $150,000 for 2008, and its total stockholders' equity on January 1, 2008, was $1,000,000. Pace declared $50,000 of dividends during 2008.

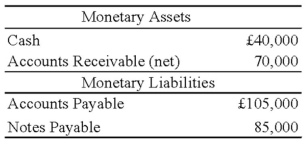

6. Exchange rates were as follows:  Assume the U.S. dollar is the functional currency, not the pound. Prepare a schedule providing a proof of the remeasurement gain or loss. Assume that the British subsidiary had the following monetary assets and liabilities at January 1, 2008:

Assume the U.S. dollar is the functional currency, not the pound. Prepare a schedule providing a proof of the remeasurement gain or loss. Assume that the British subsidiary had the following monetary assets and liabilities at January 1, 2008:

(Essay)

4.9/5 (47)

The gain or loss on the effective portion of a U.S. parent company's hedge of a net investment in a foreign entity should be treated as:

(Multiple Choice)

4.8/5 (30)

When the local currency of the foreign subsidiary is the functional currency, a foreign subsidiary's inventory carried at cost would be converted to U.S. dollars by:

(Multiple Choice)

4.8/5 (40)

The balance in Newsprint Corp.'s foreign exchange loss account was $10,000 on December 31, 20X8, before any necessary year-end adjustment relating to the following:

(1) Newsprint had a $15,000 debit resulting from the restatement in dollars of the accounts of its wholly owned foreign subsidiary for the year ended December 31, 20X8.

(2) Newsprint had an account payable to an unrelated foreign supplier, payable in the supplier's local currency unit (LCU) on January 15, 20X9. The U.S. dollar-equivalent of the payable was $50,000 on the December 1, 20X8, invoice date and $53,000 on December 31, 20X8.

Based on the information provided, in Newsprint's 20X8 consolidated income statement, what amount should be included as foreign exchange loss in computing net income, if the LCU is the functional currency and the translation method is appropriate?

(Multiple Choice)

4.8/5 (41)

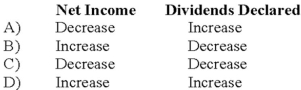

For each of the items listed below, state whether they increase or decrease the balance in cumulative translation adjustments (assuming a credit balance at the beginning of the year) when the foreign currency strengthened relative to the U.S. dollar during the year.

(Multiple Choice)

4.7/5 (33)

If the restatement method for a foreign subsidiary involves remeasuring from the local currency into the functional currency, then translating from functional currency to U.S. dollars, the functional currency of the subsidiary is:

I. U.S. dollar.

II. Local currency unit.

III. A third country's currency.

(Multiple Choice)

4.9/5 (42)

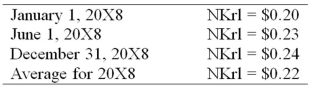

On January 1, 20X8, Transport Corporation acquired 75 percent interest in Steamship Company for $300,000. Steamship is a Norwegian company. The local currency is the Norwegian kroner (NKr). The acquisition resulted in an excess of cost-over-book value of $25,000 due solely to a patent having a remaining life of 5 years. Transport uses the fully adjusted equity method to account for its investment. Steamship's December 31, 20X8, trial balance has been translated into U.S. dollars, requiring a translation adjustment debit of $8,000. Steamship's net income translated into U.S. dollars is $35,000. It declared and paid an NKr 20,000 dividend on June 1, 20X8. Relevant exchange rates are as follows:  Assume the kroner is the functional currency.

Based on the preceding information, in the journal entry to record the receipt of dividend from Steamship,

Assume the kroner is the functional currency.

Based on the preceding information, in the journal entry to record the receipt of dividend from Steamship,

(Multiple Choice)

4.8/5 (32)

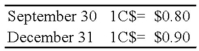

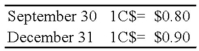

On September 30, 20X8, Wilfred Company sold inventory to Jackson Corporation, its Canadian subsidiary. The goods cost Wilfred $30,000 and were sold to Jackson for $40,000, payable in Canadian dollars. The goods are still on hand at the end of the year on December 31. The Canadian dollar (C$) is the functional currency of the Canadian subsidiary. The exchange rates follow:  Based on the preceding information, at what dollar amount is the ending inventory shown in the trial balance of the consolidated worksheet?

Based on the preceding information, at what dollar amount is the ending inventory shown in the trial balance of the consolidated worksheet?

(Multiple Choice)

4.8/5 (33)

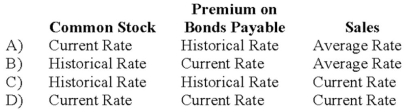

If the functional currency is the local currency of a foreign subsidiary, what exchange rates should be used to translate the items below, assuming the foreign subsidiary is in a country which has not experienced hyperinflation over three years?

(Multiple Choice)

4.9/5 (33)

Under the temporal method, which of the following is usually used to translate monetary amounts to the functional currency?

I. The current exchange rate

II The historical exchange rate

III. Average exchange rate

(Multiple Choice)

4.8/5 (49)

Parisian Co. is a French company located in Paris. Yankee Corp., located in New York City, acquires Parisian Co. Parisian has the Euro as its local currency and the Swiss Franc as its functional currency. Yankee has the U.S. dollar as its local currency and the U.S. dollar as its functional currency.

Required:

a) The year-end consolidated financial statements will be prepared in which currency?

b) Explain which method is appropriate to use to use at year-end: Translation or Remeasurement?

(Essay)

4.9/5 (37)

On September 30, 20X8, Wilfred Company sold inventory to Jackson Corporation, its Canadian subsidiary. The goods cost Wilfred $30,000 and were sold to Jackson for $40,000, payable in Canadian dollars. The goods are still on hand at the end of the year on December 31. The Canadian dollar (C$) is the functional currency of the Canadian subsidiary. The exchange rates follow:  Based on the preceding information, what amount of unrealized intercompany gross profit is eliminated in preparing the consolidated financial statements for the year?

Based on the preceding information, what amount of unrealized intercompany gross profit is eliminated in preparing the consolidated financial statements for the year?

(Multiple Choice)

4.8/5 (41)

If the functional currency is the local currency of a foreign subsidiary, what exchange rates should be used to translate the items below, assuming the foreign subsidiary is in a country which has not experienced hyperinflation over three years?

(Multiple Choice)

4.7/5 (25)

Note: This is a Kaplan CPA Review Question

Mazeppa, Inc. is a multinational entity with its head office located in Toronto, Canada. Its main foreign subsidiary is in Paris, France, but the primary economic environment in which the foreign subsidiary generates and expends cash is in the United States. Based on this information, which of the following statements is most likely true for Mazeppa, Inc.?

(Multiple Choice)

4.9/5 (45)

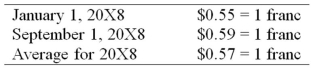

The British subsidiary of a U.S. company reported cost of goods sold of 75,000 pounds (sterling) for the current year ended December 31. The beginning inventory was 10,000 pounds, and the ending inventory was 15,000 pounds. Spot rates for various dates are as follows:  Assuming the dollar is the functional currency of the British subsidiary, the remeasured amount of cost of goods sold that should appear in the consolidated income statement is:

Assuming the dollar is the functional currency of the British subsidiary, the remeasured amount of cost of goods sold that should appear in the consolidated income statement is:

(Multiple Choice)

4.8/5 (29)

The balance in Newsprint Corp.'s foreign exchange loss account was $10,000 on December 31, 20X8, before any necessary year-end adjustment relating to the following:

(1) Newsprint had a $15,000 debit resulting from the restatement in dollars of the accounts of its wholly owned foreign subsidiary for the year ended December 31, 20X8.

(2) Newsprint had an account payable to an unrelated foreign supplier, payable in the supplier's local currency unit (LCU) on January 15, 20X9. The U.S. dollar-equivalent of the payable was $50,000 on the December 1, 20X8, invoice date and $53,000 on December 31, 20X8.

Based on the information provided, in Newsprint's 20X8 consolidated income statement, what amount should be included as foreign exchange loss in computing net income, if the U.S. dollar is the functional currency and the remeasurement method is appropriate?

(Multiple Choice)

4.8/5 (38)

Elan, a U.S. corporation, completed the December 31, 20X8, foreign currency translation of its 70 percent owned Swiss subsidiary's trial balance using the current rate method. The translation resulted in a debit adjustment of $25,000. The subsidiary had reported net income of 800,000 Swiss francs for 20X8 and paid dividends of 50,000 Swiss francs on September 1, 20X8. The translation rates for the year were:  The January 1 balance of the Investment in the Swiss subsidiary account was $1,600,000. Elan acquired its interest in the Swiss subsidiary at book value with no differential or goodwill recorded at acquisition.

Elan's Investment in Swiss subsidiary account at December 31, 20X8, is:

The January 1 balance of the Investment in the Swiss subsidiary account was $1,600,000. Elan acquired its interest in the Swiss subsidiary at book value with no differential or goodwill recorded at acquisition.

Elan's Investment in Swiss subsidiary account at December 31, 20X8, is:

(Multiple Choice)

4.9/5 (41)

All of the following are benefits the U.S. will gain from the adoption of globally consistent accounting standards except for:

(Multiple Choice)

4.7/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)