Exam 9: Forming and Operating Partnerships

Exam 1: Business Income, Deductions, and Accounting Methods99 Questions

Exam 2: Property Acquisition and Cost Recovery107 Questions

Exam 3: Property Dispositions110 Questions

Exam 4: Entities Overview80 Questions

Exam 5: Corporate Operations106 Questions

Exam 6: Accounting for Income Taxes100 Questions

Exam 7: Corporate Taxation: Nonliquidating Distributions100 Questions

Exam 8: Corporate Formation, Reorganization, and Liquidation100 Questions

Exam 9: Forming and Operating Partnerships106 Questions

Exam 10: Dispositions of Partnership Interests and Partnership Distributions100 Questions

Exam 11: S Corporations134 Questions

Exam 12: State and Local Taxes117 Questions

Exam 13: The Us Taxation of Multinational Transactions89 Questions

Exam 14: Transfer Taxes and Wealth Planning123 Questions

Select questions type

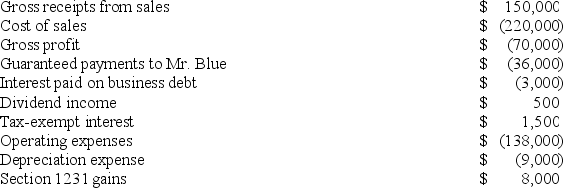

On January 1, 20X9, Mr. Blue and Mr. Grey each contributed $100,000 to form the B&G General Partnership. Their partnership agreement states that they will each receive a 50 percent profits and loss interest. The partnership agreement also provides that Mr. Blue will receive an annual $36,000 guaranteed payment. B&G began business on January 1, 20X9. For its first taxable year, its accounting records contained the following information:

The $3,000 of interest was paid on a $60,000 loan made to B&G by Key Bank on June 30, 20X9. B&G repaid $10,000 of the loan on December 15, 20X9. Neither of the partners received a cash distribution from B&G in 20X9.

Complete the following table related to Mr. Blue's interest in B&G partnership:

The $3,000 of interest was paid on a $60,000 loan made to B&G by Key Bank on June 30, 20X9. B&G repaid $10,000 of the loan on December 15, 20X9. Neither of the partners received a cash distribution from B&G in 20X9.

Complete the following table related to Mr. Blue's interest in B&G partnership:

(Essay)

4.8/5  (40)

(40)

Which of the following would not be classified as a material participant in an activity?

(Multiple Choice)

4.9/5 (38)

How does additional debt or relief of debt affect a partner's basis?

(Multiple Choice)

4.9/5 (44)

Clint noticed that the Schedule K-1 he just received from ABC Partnership included a $20,000 ordinary business loss allocation. His tax basis in ABC at the beginning of ABC's most recent tax year was $10,000. Comparing the Schedule K-1 he recently received from ABC with the Schedule K-1 he received from ABC last year, Clint noted that his share of ABC partnership debt changed as follows: recourse debt increased from $0 to $2,000, qualified nonrecourse debt increased from $0 to $3,000, and nonrecourse debt increased from $0 to $3,000. Finally, the Schedule K-1 Clint recently received from ABC reflected a $1,000 cash contribution he made to ABC during the year.

Clint is not a material participant in ABC Partnership, and he received $10,000 of passive income from another investment during the same year he received the loss allocation from ABC. How much of the $20,000 loss from ABC can Clint deduct currently, and how much of the loss is suspended because of the tax basis, at-risk, and passive activity loss limitations?

(Essay)

4.7/5 (40)

If partnership debt is reduced and a partner is deemed to receive a cash distribution, what impact does the deemed distribution have on the partner if it is in excess of her tax basis?

(Multiple Choice)

4.8/5 (43)

Nonrecourse debt is generally allocated according to the profit-sharing ratios of the partnership.

(True/False)

4.7/5 (41)

XYZ, LLC, has several individual and corporate members. Abe and Joe, individuals with 4/30 year-ends, each have a 23 percent profits and capital interest. RST, Inc., a corporation with a 6/30 year-end, owns a 4 percent profits and capital interest, while DEF, Inc., a corporation with an 8/30 year-end, owns a 4.9 percent profits and capital interest. Finally, 30 other calendar year-end individual partners (each with less than a 2 percent profits and capital interest) own the remaining 45 percent of the profits and capital interests in XYZ. What tax year-end should XYZ use, and which test or rule requires this year-end?

(Multiple Choice)

4.9/5 (37)

What is the difference between the aggregate and entity theories of partnership taxation? Provide two examples of how partnership tax rules reflect the aggregate theory and two examples of how they reflect the entity theory.

(Essay)

4.9/5 (29)

What is the rationale for the specific rules partnerships must follow in determining a partnership's taxable year-end?

(Multiple Choice)

5.0/5 (37)

Partners must generally treat the value of profits interests they receive in exchange for services as ordinary income.

(True/False)

4.8/5 (39)

Bob is a general partner in Fresh Foods Partnership and is trying to determine if the income reported on his K-1 should be classified as passive or active trade or business income. List three different criteria that, if met, would allow Bob to treat the income from Fresh Foods as active trade or business income.

(Essay)

4.8/5 (36)

For partnership tax years ending after December 31, 2015, when must a partnership file its return?

(Multiple Choice)

4.9/5 (39)

Partnership tax rules incorporate both the entity and aggregate approaches.

(True/False)

4.8/5 (32)

Which person would generally be treated as a material participant in an activity?

(Multiple Choice)

4.8/5 (34)

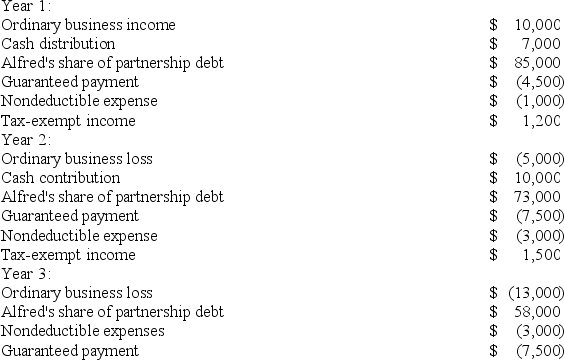

Alfred, a one-third profits and capital partner in Pizzeria Partnership, needs help in adjusting his tax basis to reflect the information contained in his most recent Schedule K-1 from the partnership. Unfortunately, the Schedule K-1 he recently received was for Year 3 of the partnership, but Alfred only knows that his tax basis at the beginning of Year 2 of the partnership was $23,000. Thankfully, Alfred still has his Schedule K-1 from the partnership for Years 1 and 2.

Using the following information from Alfred's Year 1, Year 2, and Year 3 Schedule K-1, calculate his tax basis the end of Year 2 and Year 3.

(Essay)

4.9/5 (37)

The main difference between a partner's tax basis and at-risk amount is that qualified nonrecourse financing is not included in the at-risk basis amount.

(True/False)

4.8/5 (26)

Which of the following statements exemplifies the entity theory of partnership taxation?

(Multiple Choice)

4.9/5 (45)

An additional allocation of partnership debt or relief of partnership debt is considered to be a deemed cash contribution or cash distribution, respectively.

(True/False)

4.8/5 (36)

A partner's tax basis or at-risk amount can be increased by making capital contributions, by paying off partnership debt, or by increasing the profitability of the partnership.

(True/False)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)