Exam 9: Forming and Operating Partnerships

Exam 1: Business Income, Deductions, and Accounting Methods99 Questions

Exam 2: Property Acquisition and Cost Recovery107 Questions

Exam 3: Property Dispositions110 Questions

Exam 4: Entities Overview80 Questions

Exam 5: Corporate Operations106 Questions

Exam 6: Accounting for Income Taxes100 Questions

Exam 7: Corporate Taxation: Nonliquidating Distributions100 Questions

Exam 8: Corporate Formation, Reorganization, and Liquidation100 Questions

Exam 9: Forming and Operating Partnerships106 Questions

Exam 10: Dispositions of Partnership Interests and Partnership Distributions100 Questions

Exam 11: S Corporations134 Questions

Exam 12: State and Local Taxes117 Questions

Exam 13: The Us Taxation of Multinational Transactions89 Questions

Exam 14: Transfer Taxes and Wealth Planning123 Questions

Select questions type

Explain why partners must increase their tax basis for their share of partnership taxable and nontaxable income or gain and reduce their basis by their share of partnership deductible and nondeductible expenses or losses.

(Essay)

4.8/5  (33)

(33)

Which of the following statements regarding capital and profits interests received for services contributed to a partnership is false?

(Multiple Choice)

4.9/5 (43)

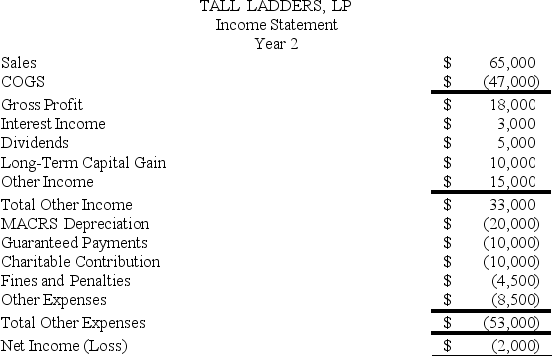

At the end of Year 1, Tony had a tax basis of $40,000 in Tall Ladders, Limited Partnership. Tony has a 20 percent profits interest in Tall Ladders. For Year 2, Tall Ladders will pay Tony a $10,000 guaranteed payment for extra services he provides to the partnership. Given the following income statement and balance sheet from Tall Ladders, what is Tony's adjusted tax basis at the end of Year 2?

(Essay)

4.9/5 (38)

What type of debt is not included in calculating a partner's at-risk amount?

(Multiple Choice)

4.9/5 (38)

Fred has a 45 percent profits interest and 30 percent capital interest in the SAP Partnership, and his tax basis before considering his share of SAP's current-year loss is $11,000. Included in his tax basis is a $2,600 share of recourse debt and a $5,300 share of nonrecourse debt. Fred is a limited partner in SAP. He is not involved in any other activities. If SAP has a $15,000 ordinary loss for the year, how much of the loss can be deducted currently, and how much of the loss is suspended because of the tax basis, at-risk, and passive activity loss limitations?

(Essay)

4.9/5 (34)

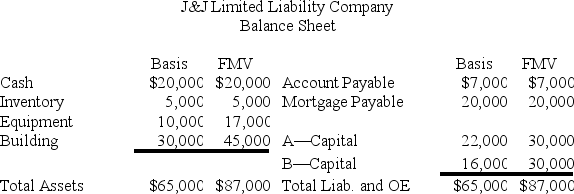

J&J, LLC, was in its third year of operations when J&J decided to expand the number of members from two, A and B, with equal profits and capital interests, to three members, A, B, and C. The third member, C, will contribute her financial expertise to the LLC in exchange for a one-third capital interest in J&J. Given the balance sheet below reflecting the financial position of J&J on the date member C is admitted, what are the tax consequences to members A, B, and C, and to J&J, when C receives her capital interest? If, instead, member C receives a one-third profits interest, what would be the tax consequences to members A, B, and C, and to J&J?

(Essay)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)