Exam 12: Intangible Assets

Exam 1: Financial Accounting and Accounting Standards103 Questions

Exam 2: Conceptual Framework for Financial Reporting155 Questions

Exam 3: The Accounting Information System144 Questions

Exam 4: Income Statement and Related Information139 Questions

Exam 5: Balance Sheet and Statement of Cash Flows127 Questions

Exam 6: Accounting and the Time Value of Money152 Questions

Exam 7: Cash and Receivables173 Questions

Exam 8: Valuation of Inventories: a Cost-Basis Approach173 Questions

Exam 9: Inventories: Additional Valuation Issues168 Questions

Exam 10: Acquisition and Disposition of Property, Plant, and Equipment170 Questions

Exam 11: Depreciation, Impairments, and Depletion156 Questions

Exam 12: Intangible Assets171 Questions

Exam 13: Current Liabilities and Contingencies170 Questions

Exam 14: Long-Term Liabilities140 Questions

Exam 15: Stockholders Equity155 Questions

Exam 16: Dilutive Securities and Earnings Per Share160 Questions

Exam 17: Investments141 Questions

Exam 18: Revenue Recognition145 Questions

Exam 19: Accounting for Income Taxes127 Questions

Exam 20: Accounting for Pensions and Postretirement Benefits137 Questions

Exam 21: Accounting for Leases128 Questions

Exam 22: Accounting Changes and Error Analysis103 Questions

Exam 23: Statement of Cash Flows143 Questions

Exam 24: Full Disclosure in Financial Reporting108 Questions

Exam 25: Appendix89 Questions

Select questions type

Wriglee, Inc. went to court this year and successfully defended its patent from infringement by a competitor. The cost of this defense should be charged to

(Multiple Choice)

4.8/5  (38)

(38)

Under what circumstances is it appropriate to record goodwill in the accounts? How should goodwill, properly recorded on the books, be written off in accordance with generally accepted accounting principles?

(Essay)

4.9/5 (40)

Dennis Company purchases Miles Company for $5,000,000 cash on January 1, 2015. The book value of Miles Company's net assets reported on its December 31, 2014 financial statement was $3,800,000. An analysis indicated that the fair value of Miles's tangible assets exceeded the book value by $600,000, and the fair value of identifiable intangible assets exceeded book value by $320,000. Determine the fair value of identifiable net assets used to record goodwill.

(Multiple Choice)

4.9/5 (43)

As in U.S. GAAP, under IFRS the costs associated with research and development are segregated into two components.

(True/False)

4.8/5 (30)

Which of the following costs incurred internally to create an intangible asset is generally expensed?

(Multiple Choice)

5.0/5 (43)

IFRS permits some capitalization of internally generated intangible assets, if it is probable there will be a future benefit and the amount can be readily measured.

(True/False)

4.9/5 (29)

The primary IFRS related to intangible assets and impairments is found in

(Multiple Choice)

4.8/5 (37)

If a company constructs a laboratory building to be used as a research and development facility, the cost of the laboratory building is matched against earnings as

(Multiple Choice)

4.8/5 (43)

Impairment of copyrights.Presented below is information related to copyrights owned by Wamser Corporation at December 31, 2014.  Assume Wamser will continue to use this asset in the future. As of December 31, 2014, the copyrights have a remaining useful life of 5 years.

Instructions

(a) Prepare the journal entry (if any) to record the impairment of the asset at December 31, 2014.

(b) Prepare the journal entry to record amortization expense for 2015.

(c) The fair value of the copyright at December 31, 2015 is $2,500,000. Prepare the journal entry (if any) necessary to record this increase in fair value.

Assume Wamser will continue to use this asset in the future. As of December 31, 2014, the copyrights have a remaining useful life of 5 years.

Instructions

(a) Prepare the journal entry (if any) to record the impairment of the asset at December 31, 2014.

(b) Prepare the journal entry to record amortization expense for 2015.

(c) The fair value of the copyright at December 31, 2015 is $2,500,000. Prepare the journal entry (if any) necessary to record this increase in fair value.

(Essay)

4.7/5 (30)

On January 2, 2014, Klein Co. bought a trademark from Royce, Inc. for $1,600,000. An independent research company estimated that the remaining useful life of the trademark was 10 years. Its unamortized cost on Royce's books was $1,200,000. In Klein's 2014 income statement, what amount should be reported as amortization expense?

(Multiple Choice)

4.7/5 (40)

Which characteristic is not possessed by intangible assets?

(Multiple Choice)

4.8/5 (28)

Costs in the research phase are always expensed under both IFRS and U.S. GAAP.

(True/False)

4.7/5 (27)

When a company develops a trademark the costs directly related to securing it should generally be capitalized. Which of the following costs associated with a trademark would not be capitalized?

(Multiple Choice)

4.9/5 (30)

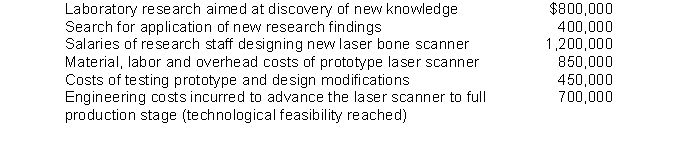

The following costs are incurred during the research and development phases of a laser bone scanner  Identify which of these are development phase items and will be immediately expensed underU.S. GAAP and IFRS.U.S. GAAP IFRS

Identify which of these are development phase items and will be immediately expensed underU.S. GAAP and IFRS.U.S. GAAP IFRS

(Multiple Choice)

4.9/5 (36)

Trademarks, newspaper mastheads, and internet domain names are all examples of

(Multiple Choice)

4.8/5 (34)

The costs of organizing a corporation include legal fees, fees paid to the state of incorporation, fees paid to promoters, and the costs of meetings for organizing the promoters. These costs are said to benefit the corporation for the entity's entire life. These costs should be

(Multiple Choice)

4.9/5 (29)

Why does the accounting profession make a distinction between internally created intangible assets and purchased intangible assets?

(Essay)

4.8/5 (37)

Companies should test indefinite life intangible assets at least annually for

(Multiple Choice)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)