Exam 8: Supply in a Competitive Market

Exam 2: Supply and Demand109 Questions

Exam 3: Using Supply and Demand to Analyze Markets104 Questions

Exam 4: Consumer Behavior119 Questions

Exam 5: Individual and Market Demand103 Questions

Exam 6: Producer Behavior102 Questions

Exam 7: Costs102 Questions

Exam 8: Supply in a Competitive Market93 Questions

Exam 9: Market Power and Monopoly97 Questions

Exam 10: Market Power and Pricing Strategies100 Questions

Exam 11: Imperfect Competition99 Questions

Exam 12: Game Theory96 Questions

Exam 13: Factor Markets70 Questions

Exam 14: Investment, Time, and Insurance77 Questions

Exam 15: General Equilibrium79 Questions

Exam 16: Asymmetric Information79 Questions

Exam 17: Externalities and Public Goods80 Questions

Exam 18: Behavioral and Experimental Economics79 Questions

Select questions type

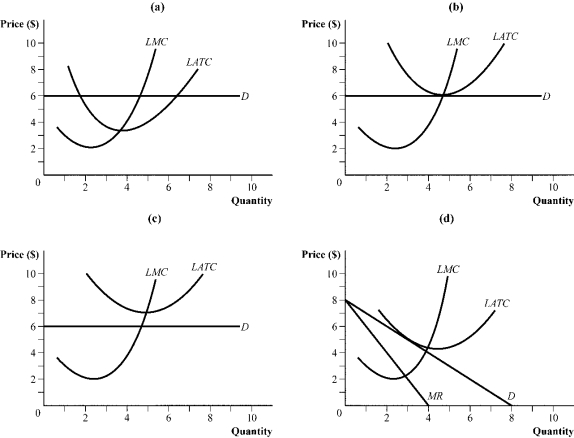

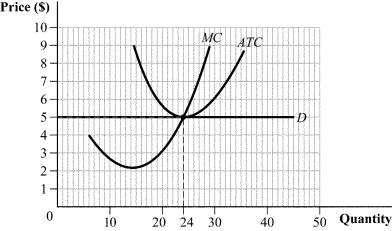

Use the following to answer question:

Figure 8.16  -(Figure 8.16) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

-(Figure 8.16) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

Free

(Multiple Choice)

4.9/5  (36)

(36)

Correct Answer: Verified

Verified

B

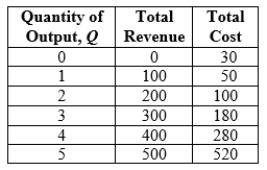

Use the following to answer question:

Table 8.1  -(Table 8.1) The level of output where marginal revenue equals marginal cost is:

-(Table 8.1) The level of output where marginal revenue equals marginal cost is:

Free

(Multiple Choice)

4.8/5 (40)

Correct Answer:Verified

D

Which of the following characteristics relate(s) to perfect competition?

Free

(Multiple Choice)

4.8/5 (34)

Correct Answer:Verified

B

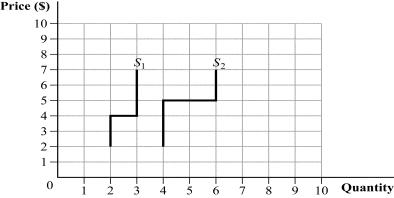

Use the following to answer question:

Figure 8.14  -(Figure 8.14) In this perfectly competitive industry, there are 100 firms with a short-run supply curve represented by S1 and 50 firms with a short-run supply curve represented by S2. At a market price of $4.50, industry output is:

-(Figure 8.14) In this perfectly competitive industry, there are 100 firms with a short-run supply curve represented by S1 and 50 firms with a short-run supply curve represented by S2. At a market price of $4.50, industry output is:

(Multiple Choice)

4.8/5 (42)

Use the following to answer question:

Figure 8.1  -(Figure 8.1) Which of the following statements is (are) TRUE?

-(Figure 8.1) Which of the following statements is (are) TRUE?

(Multiple Choice)

4.9/5 (33)

Use the following to answer question:

Figure 8.8  -(Figure 8.8) Which of the following statements is (are) TRUE?

-(Figure 8.8) Which of the following statements is (are) TRUE?

(Multiple Choice)

4.9/5 (41)

Suppose that each firm in a perfectly competitive market has a short-run total cost of TC = 75 + 500Q - 5Q2 + 0.5Q3, where MC = 500 - 10Q + 1.5Q2.

(Essay)

4.9/5 (40)

Use the following to answer question:

Figure 8.26  -(Figure 8.26) The graph shows a perfectly competitive industry in long-run equilibrium. The price is _____. If technology lowers production costs by an average of 50%, the new long-run equilibrium price will be _____.

-(Figure 8.26) The graph shows a perfectly competitive industry in long-run equilibrium. The price is _____. If technology lowers production costs by an average of 50%, the new long-run equilibrium price will be _____.

(Essay)

4.9/5 (46)

Suppose that the market for painting services is perfectly competitive. Painting companies are identical; their long-run cost functions are given by  .

Market demand is

.

Market demand is  .

a. Find the long-run equilibrium price in this industry.

b. Use market demand to find the equilibrium total industry output.

c. Find the equilibrium number of firms.

.

a. Find the long-run equilibrium price in this industry.

b. Use market demand to find the equilibrium total industry output.

c. Find the equilibrium number of firms.

(Essay)

4.9/5 (29)

Stu owns an ice cream parlor that is usually closed during the winter. This winter, however, Stu is considering opening his business in February instead of March. If Stu opens his store in February, he will earn total revenue of $4,000 for the month, incurring variable costs of $3,500 and fixed costs of $1,500. If the store remains closed during February, Stu will earn no revenues and incur fixed costs of $1,500. Stu should:

(Multiple Choice)

4.7/5 (39)

Use the following to answer question:

Figure 8.18  -(Figure 8.18) Which of the following statements is (are) TRUE?

-(Figure 8.18) Which of the following statements is (are) TRUE?

(Multiple Choice)

4.9/5 (42)

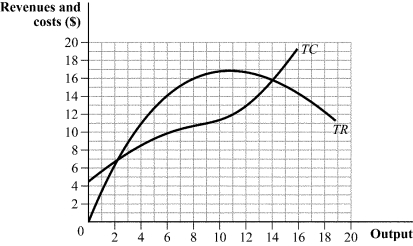

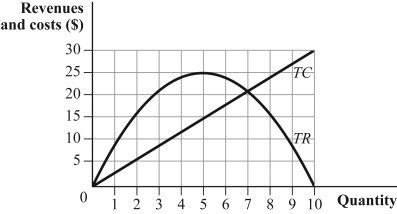

Use the following to answer question:

Figure 8.20  -(Figure 8.20) What is TRUE about the slopes of the total revenue and total cost curves at the firm's profit-maximizing output level? What is the actual slope of the total revenue curve at the profit-maximizing output level? What is the firm's marginal cost at the profit-maximizing output level?

-(Figure 8.20) What is TRUE about the slopes of the total revenue and total cost curves at the firm's profit-maximizing output level? What is the actual slope of the total revenue curve at the profit-maximizing output level? What is the firm's marginal cost at the profit-maximizing output level?

(Essay)

4.9/5 (49)

Suppose that a perfectly competitive firm's AVC curve is given by AVC = WQ, and its marginal cost curve is given by MC = 2WQ, where W is the wage rate.

(Essay)

4.7/5 (39)

In a perfectly competitive industry, the long-run equilibrium price is $12. If a technological innovation lowers production costs, the long-run equilibrium price will:

(Multiple Choice)

4.7/5 (35)

Suppose that demand increases. If the total cost curves for the firms do not change with the number of firms:

(Multiple Choice)

4.8/5 (33)

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; their long-run cost functions are given by  . Market demand is

. Market demand is  .

a. Find the long-run equilibrium price in this industry.

b. Use market demand to find the equilibrium total industry output.

c. Find the equilibrium number of firms.

.

a. Find the long-run equilibrium price in this industry.

b. Use market demand to find the equilibrium total industry output.

c. Find the equilibrium number of firms.

(Essay)

4.8/5 (44)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)