Exam 8: Supply in a Competitive Market

Exam 2: Supply and Demand109 Questions

Exam 3: Using Supply and Demand to Analyze Markets104 Questions

Exam 4: Consumer Behavior119 Questions

Exam 5: Individual and Market Demand103 Questions

Exam 6: Producer Behavior102 Questions

Exam 7: Costs102 Questions

Exam 8: Supply in a Competitive Market93 Questions

Exam 9: Market Power and Monopoly97 Questions

Exam 10: Market Power and Pricing Strategies100 Questions

Exam 11: Imperfect Competition99 Questions

Exam 12: Game Theory96 Questions

Exam 13: Factor Markets70 Questions

Exam 14: Investment, Time, and Insurance77 Questions

Exam 15: General Equilibrium79 Questions

Exam 16: Asymmetric Information79 Questions

Exam 17: Externalities and Public Goods80 Questions

Exam 18: Behavioral and Experimental Economics79 Questions

Select questions type

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that the wages increase as the industry output increases. Delis in this market face the following total cost:  where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals  , where N is the number of firms.

a. How does average total cost for the firm change as industry output increases?

b. What does this relationship imply for industry's long-run supply curve?

, where N is the number of firms.

a. How does average total cost for the firm change as industry output increases?

b. What does this relationship imply for industry's long-run supply curve?

(Essay)

4.8/5  (35)

(35)

Use the following to answer question:

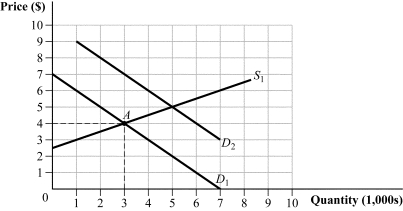

Figure 8.17  -(Figure 8.17) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

-(Figure 8.17) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

(Multiple Choice)

4.9/5 (38)

In a perfectly competitive market, each firm has a long-run total cost given by LTC = 100Q - 10Q2 + 1/3Q3 and long-run marginal cost curve given by LMC = 100 - 20Q + Q2. What is the market's long-run equilibrium price?

(Multiple Choice)

4.9/5 (38)

If the long-run total cost curve for each firm is given by TC = 60Q - 70Q2 + 4Q3, in the long run, the marginal cost is:

(Multiple Choice)

4.9/5 (32)

In the market for lock washers, a perfectly competitive market, the current equilibrium price is $5 per box. Washer King, one of the many producers of washers, has a daily short-run total cost given by TC = 190 + 0.20Q + 0.0025Q2, where Q measures boxes of washers. Washer King's corresponding marginal cost is MC = 0.20 + 0.005Q. How many boxes of washers should Washer King produce per day to maximize profit?

(Multiple Choice)

4.9/5 (35)

Explain what will happen in each of the following scenarios in a long run constant cost competitive industry.

a. The market price is $50 and firms are earning positive profits.

b. The market price is $25 and firms are earning zero profits.

c. The market price is $15 and firms are earning negative profits.

(Essay)

4.9/5 (33)

Use the following to answer question:

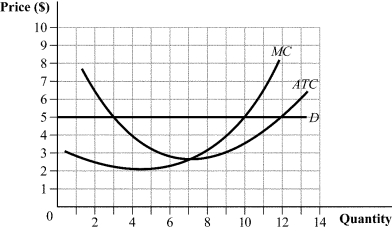

Figure 8.7  -(Figure 8.7) If the market price is $6, this perfectly competitive firm will earn profits of:

-(Figure 8.7) If the market price is $6, this perfectly competitive firm will earn profits of:

(Multiple Choice)

4.8/5 (38)

Use the following to answer question:

Figure 8.6  -(Figure 8.6) This firm maximizes profit by producing _____ units of output.

-(Figure 8.6) This firm maximizes profit by producing _____ units of output.

(Multiple Choice)

4.9/5 (36)

Use the following to answer question:

Figure 8.12  -(Figure 8.12) The perfectly competitive firm's short-run supply curve is represented by points:

-(Figure 8.12) The perfectly competitive firm's short-run supply curve is represented by points:

(Multiple Choice)

4.9/5 (49)

Suppose that the long-run total cost curve for each firm is given by TC = 500Q - 20Q2 + Q3, where Q is the quantity of the product. Also suppose there is free entry and exit. To find the quantity where ATC is minimized, the firm would need to solve the following equation for Q:

(Multiple Choice)

4.7/5 (41)

Suppose a perfectly competitive industry has 300 firms, and the short-run supply curve for each firm is given by Q = 2P. What is the short-run industry supply curve?

(Multiple Choice)

4.9/5 (47)

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that wages increase as industry output increases. Delis in this market face the following total cost:  where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals  , where N is the number of firms. Market demand is

, where N is the number of firms. Market demand is  .

a. Find the long-run equilibrium output for each firm.

b. How does the long-run equilibrium price change as the number of firms increases?

c. Find the long-run equilibrium number of firms and total industry output.

d. Find the long-run equilibrium price.

.

a. Find the long-run equilibrium output for each firm.

b. How does the long-run equilibrium price change as the number of firms increases?

c. Find the long-run equilibrium number of firms and total industry output.

d. Find the long-run equilibrium price.

(Essay)

4.9/5 (36)

Suppose that the market for painting services is perfectly competitive. Painting companies are identical and have long-run cost functions given by  .

a. Derive the marginal and average cost curves for a firm in this industry.

b. Find the quantity at which average total cost is minimized for each firm.

.

a. Derive the marginal and average cost curves for a firm in this industry.

b. Find the quantity at which average total cost is minimized for each firm.

(Essay)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)