Exam 8: Supply in a Competitive Market

Exam 2: Supply and Demand109 Questions

Exam 3: Using Supply and Demand to Analyze Markets104 Questions

Exam 4: Consumer Behavior119 Questions

Exam 5: Individual and Market Demand103 Questions

Exam 6: Producer Behavior102 Questions

Exam 7: Costs102 Questions

Exam 8: Supply in a Competitive Market93 Questions

Exam 9: Market Power and Monopoly97 Questions

Exam 10: Market Power and Pricing Strategies100 Questions

Exam 11: Imperfect Competition99 Questions

Exam 12: Game Theory96 Questions

Exam 13: Factor Markets70 Questions

Exam 14: Investment, Time, and Insurance77 Questions

Exam 15: General Equilibrium79 Questions

Exam 16: Asymmetric Information79 Questions

Exam 17: Externalities and Public Goods80 Questions

Exam 18: Behavioral and Experimental Economics79 Questions

Select questions type

Suppose the market for sprouts is in long-run equilibrium. In the short run, what will happen if an E. coli outbreak reduces the demand for sprouts?

(Multiple Choice)

4.9/5  (34)

(34)

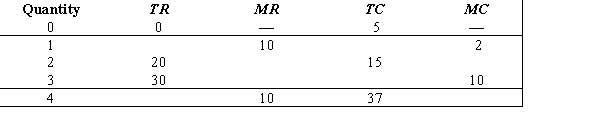

Complete the following table and identify the quantity that maximizes profit.

(Essay)

4.9/5 (34)

Suppose the long-run equilibrium price in a perfectly competitive market is $100. When demand increases, if it is a(n) _____ industry, the long-run equilibrium price will _____ to reflect a _____ long-run average total cost.

(Multiple Choice)

4.8/5 (43)

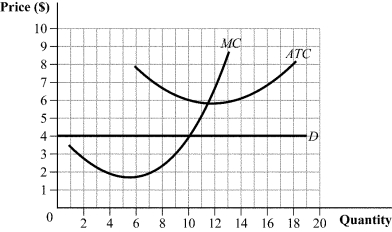

Use the following to answer question:

Figure 8.10  -(Figure 8.10) Economic profit for this firm can be calculated as:

-(Figure 8.10) Economic profit for this firm can be calculated as:

(Multiple Choice)

4.9/5 (35)

Suppose that the market for chocolate milk is perfectly competitive. Companies that produce chocolate milk are identical and have long-run cost functions given by  .

a. Derive the marginal and average cost curves for a firm in this industry.

b. Find the quantity at which average total cost is minimized for each firm.

.

a. Derive the marginal and average cost curves for a firm in this industry.

b. Find the quantity at which average total cost is minimized for each firm.

(Essay)

4.9/5 (28)

Suppose that the identical firms in a perfectly competitive market for cakes have long-run total cost functions given by TC(Q) = 2Q3 - 6Q2 + 10Q. Total cost is independent of the number of firms and total output in the market.

a. Describe the long-run supply curve for this industry.

b. Suppose market demand is  = 2,500 - 30P. Solve for the long-run competitive equilibrium price, output per firm, and number of firms in the market.

= 2,500 - 30P. Solve for the long-run competitive equilibrium price, output per firm, and number of firms in the market.

(Essay)

4.9/5 (47)

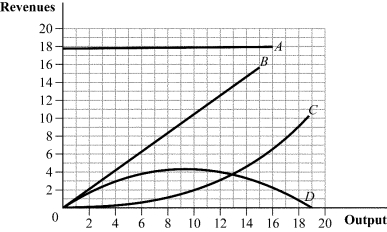

Use the following to answer question:

Figure 8.2  -(Figure 8.2) The total revenue curve for a perfectly competitive firm is represented by curve:

-(Figure 8.2) The total revenue curve for a perfectly competitive firm is represented by curve:

(Multiple Choice)

4.8/5 (41)

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; they have long-run cost functions given by  .

a. Derive the marginal and average total cost curves in this industry. (Hint: Use calculus to find marginal cost.)

b. Find the quantity at which average total cost is minimized.

.

a. Derive the marginal and average total cost curves in this industry. (Hint: Use calculus to find marginal cost.)

b. Find the quantity at which average total cost is minimized.

(Essay)

4.9/5 (32)

Suppose that the long-run total cost curve for each firm is given by TC = 1,000 + 100Q - 10Q2 + Q3. Also suppose there is free entry and exit. To find the quantity where ATC is minimized, solve the following equation for Q:

(Multiple Choice)

5.0/5 (40)

With which of the following scenarios should a perfectly competitive firm shut down in the short run?

(Multiple Choice)

4.9/5 (40)

In a perfectly competitive market with 2,000 firms, output is zero at prices less than $10. At prices of $10 to $19.99, each firm will produce 100 units of output. At any price of $20 or more, each firm will produce 300 units of output. As this industry expands output, however, prices of the key inputs to production increase substantially. The total industry output at a market price of $33 is:

(Multiple Choice)

4.8/5 (40)

Suppose that the perfectly competitive market for granola bars is made up of identical firms with long-run total cost functions given by TC(Q) = 8Q3-  Q2 + 200Q. Assume that these cost functions are independent of the number of firms in the market and that firms may enter or exit the market freely. Market demand is

Q2 + 200Q. Assume that these cost functions are independent of the number of firms in the market and that firms may enter or exit the market freely. Market demand is  , where price is in cents.

a. Using calculus, find the long-run equilibrium price, the quantity produced by each firm, and the number of firms in the industry.

b. Suppose that market demand decreases to

, where price is in cents.

a. Using calculus, find the long-run equilibrium price, the quantity produced by each firm, and the number of firms in the industry.

b. Suppose that market demand decreases to  . Solve for the new long-run competitive equilibrium.

. Solve for the new long-run competitive equilibrium.

(Essay)

4.9/5 (31)

Use the following to answer question:

Figure 8.25  -(Figure 8.25) Answer the following questions.

-(Figure 8.25) Answer the following questions.

(Essay)

4.8/5 (44)

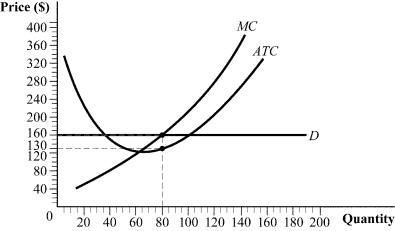

Use the following to answer question:

Figure 8.9  -(Figure 8.9) At the profit-maximizing output level, this firm earns profit of:

-(Figure 8.9) At the profit-maximizing output level, this firm earns profit of:

(Multiple Choice)

4.8/5 (36)

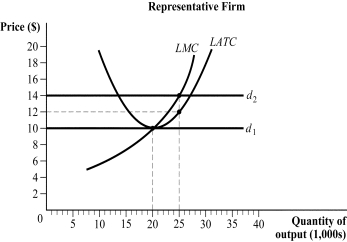

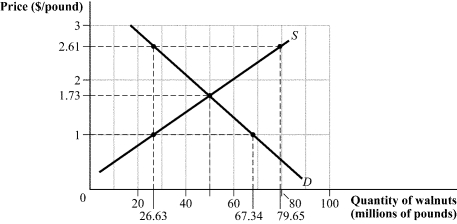

Use the following to answer question:

Figure 8.3  -(Figure 8.3) The graph depicts the perfectly competitive market for walnuts. Which of the following statements is (are) TRUE?

-(Figure 8.3) The graph depicts the perfectly competitive market for walnuts. Which of the following statements is (are) TRUE?

(Multiple Choice)

4.9/5 (25)

A perfectly competitive industry consists of 500 identical firms, each with a short-run supply curve given by Qs = -20 + 15P. What is the equation for the industry's short-run supply curve?

(Essay)

4.7/5 (37)

Suppose that the perfectly competitive market for coffee beans is made up of identical firms with long-run total cost functions given by TC = 2Q3 - 24Q2 + 80Q, where Q is 100,000 pounds of coffee beans. Assume that these cost functions are independent of the number of firms in the market and that firms may enter or exit the market freely. Market demand is  .

a. Find the long-run equilibrium price, the quantity produced by each firm, and the number of firms in the industry.

b. Suppose that market demand increases to

.

a. Find the long-run equilibrium price, the quantity produced by each firm, and the number of firms in the industry.

b. Suppose that market demand increases to  .

Solve for the new long-run competitive equilibrium and the number of firms in the industry under the new market demand condition.

.

Solve for the new long-run competitive equilibrium and the number of firms in the industry under the new market demand condition.

(Essay)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)