Exam 8: Supply in a Competitive Market

Exam 2: Supply and Demand109 Questions

Exam 3: Using Supply and Demand to Analyze Markets104 Questions

Exam 4: Consumer Behavior119 Questions

Exam 5: Individual and Market Demand103 Questions

Exam 6: Producer Behavior102 Questions

Exam 7: Costs102 Questions

Exam 8: Supply in a Competitive Market93 Questions

Exam 9: Market Power and Monopoly97 Questions

Exam 10: Market Power and Pricing Strategies100 Questions

Exam 11: Imperfect Competition99 Questions

Exam 12: Game Theory96 Questions

Exam 13: Factor Markets70 Questions

Exam 14: Investment, Time, and Insurance77 Questions

Exam 15: General Equilibrium79 Questions

Exam 16: Asymmetric Information79 Questions

Exam 17: Externalities and Public Goods80 Questions

Exam 18: Behavioral and Experimental Economics79 Questions

Select questions type

A firm's short-run total cost is TC = 10,100 + 7,700Q - 100Q2 + Q3/3, and its marginal cost is MC = 7,700 - 200Q + Q2. What is the firm's shutdown price?

(Multiple Choice)

4.8/5  (30)

(30)

In a perfectly competitive industry, there are two types of firms: low-cost producers and high-cost producers. The minimum average total cost of the high-cost producers is $150. The low-cost producers have a long-run total cost curve given by LTC = 150Q - 15Q2 + 0.4Q3, where LMC = 150 - 30Q + 1.2Q2. How much economic rent does the low-cost producer earn?

(Multiple Choice)

4.9/5 (43)

Suppose the market for relay switches is considered perfectly competitive and is in equilibrium at a price of $5,000 per pallet of relay switches. Callahan Relay produces relay switches at an average total cost given by ATC = and marginal cost given by MC = 2Q, where Q measures pallets of relay switches. If Callahan Relay maximizes profit, how much profit will it earn?

(Multiple Choice)

4.8/5 (43)

Why is the type of product sold in an industry an important characteristic?

(Multiple Choice)

4.7/5 (37)

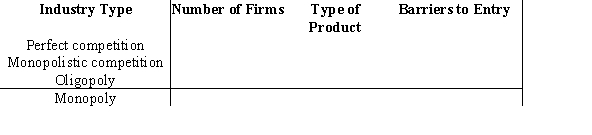

Complete the following table, choosing from this list: one, few, identical, some, unique, differentiated, identical or differentiated, many, none. Some words may be used more than once.

(Essay)

4.9/5 (35)

Use the following to answer question:

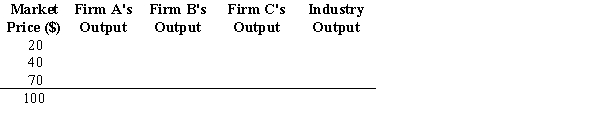

Table 8.2  -(Table 8.2) Suppose that both firms are producing 100 units of output. If the firms want to increase profit, firm A should produce _____ output and firm B should produce _____ output.

-(Table 8.2) Suppose that both firms are producing 100 units of output. If the firms want to increase profit, firm A should produce _____ output and firm B should produce _____ output.

(Multiple Choice)

5.0/5 (33)

Use the following to answer question:

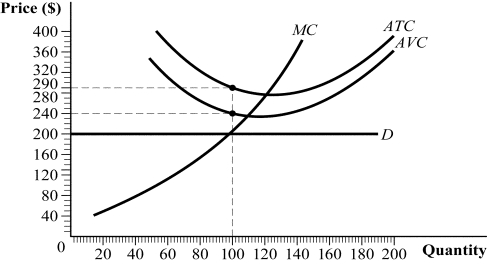

Figure 8.11  -(Figure 8.11) If this firm operates, it earns a profit of _____, but if it shuts down, it earns a profit of _____.

-(Figure 8.11) If this firm operates, it earns a profit of _____, but if it shuts down, it earns a profit of _____.

(Multiple Choice)

4.7/5 (27)

Use the following to answer question:

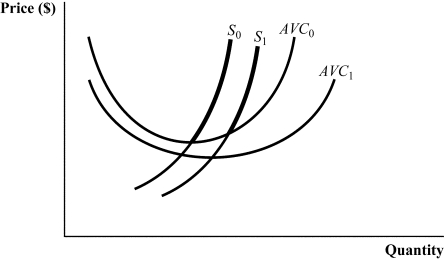

Figure 8.13  -(Figure 8.13) What could have caused the supply and average variable cost curves to shift outward?

-(Figure 8.13) What could have caused the supply and average variable cost curves to shift outward?

(Multiple Choice)

4.8/5 (45)

Use the following to answer question:

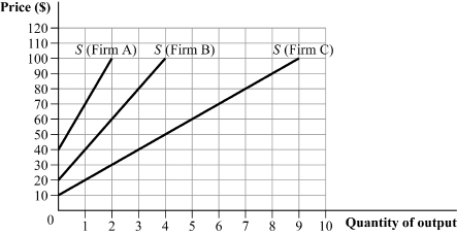

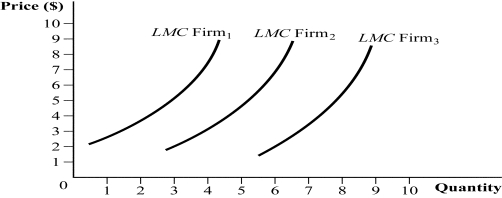

Figure 8.23  -(Figure 8.23) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. Complete the following table.

-(Figure 8.23) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. Complete the following table.

(Essay)

4.7/5 (39)

A perfectly competitive industry consists of many identical firms, each with a long-run average total cost of LATC = 800 - 10Q + 0.1Q2 and long-run marginal cost of LMC = 800 - 20Q + 0.3Q2.

(Essay)

4.8/5 (34)

A perfectly competitive industry consists of 50 East Coast firms and 80 West Coast firms. Each of the East Coast firms has a short-run supply curve of QE = 20P, and each of the West Coast firms has a short-run supply curve of QW = 30P.

(Essay)

4.9/5 (37)

Under free entry and exit, to find the quantity where ATC is minimized, the firm can:

(Multiple Choice)

4.8/5 (36)

A perfectly competitive firm maximizes profit by producing 500 units of output, selling each unit for $10. The firm's average variable cost is $7 and average fixed cost is $2. What is the firm's producer surplus?

(Multiple Choice)

4.8/5 (40)

Which of the following statements is (are) TRUE of price-taking firms?

(Multiple Choice)

4.9/5 (35)

To see how the equilibrium price is affected by the increase in industry output that comes from the entry of new firms, take the derivative of _____ and see whether it is positive or negative.

(Multiple Choice)

4.8/5 (36)

Use the following to answer question:

Figure 8.19

-(Figure 8.19) The graph represents three perfectly competitive firms. Which of the following statements is (are) TRUE?

-(Figure 8.19) The graph represents three perfectly competitive firms. Which of the following statements is (are) TRUE?

(Multiple Choice)

4.7/5 (39)

In a perfectly competitive industry, the equilibrium price is $56 and the minimum average total cost of the industry's firms is $40. If this is a constant-cost industry, we can expect that in the long run, firms will _____ the market, shifting the industry's short-run supply curve _____.

(Multiple Choice)

4.9/5 (36)

Suppose that there are 1,000 firms in a perfectly competitive industry, each with a short-run total cost curve given by TC = 800 + 8Q + 0.1Q2 and marginal cost curve given by MC = 8 + 0.2Q.

(Essay)

4.8/5 (34)

A perfectly competitive industry in long-run equilibrium comprises 200 identical firms. In one of the firms, the workers unionize and receive a 20% wage increase. What happens to the unionized firm in the short run and the long run? Supplement your answer with a graph.

(Essay)

4.7/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)