Exam 8: Supply in a Competitive Market

Exam 2: Supply and Demand109 Questions

Exam 3: Using Supply and Demand to Analyze Markets104 Questions

Exam 4: Consumer Behavior119 Questions

Exam 5: Individual and Market Demand103 Questions

Exam 6: Producer Behavior102 Questions

Exam 7: Costs102 Questions

Exam 8: Supply in a Competitive Market93 Questions

Exam 9: Market Power and Monopoly97 Questions

Exam 10: Market Power and Pricing Strategies100 Questions

Exam 11: Imperfect Competition99 Questions

Exam 12: Game Theory96 Questions

Exam 13: Factor Markets70 Questions

Exam 14: Investment, Time, and Insurance77 Questions

Exam 15: General Equilibrium79 Questions

Exam 16: Asymmetric Information79 Questions

Exam 17: Externalities and Public Goods80 Questions

Exam 18: Behavioral and Experimental Economics79 Questions

Select questions type

Use the following to answer question:

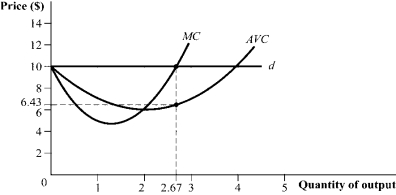

Figure 8.24  -(Figure 8.24) Answer the following questions.

-(Figure 8.24) Answer the following questions.

(Essay)

4.9/5  (38)

(38)

A perfectly competitive industry has 100 high-cost producers, each with a short-run supply curve given by QH = 16P, and 100 low-cost producers, each with a short-run supply curve given by QL = 24P. The industry demand curve is given by Qd = 100,000 - 1,000P. At market equilibrium, industry producer surplus is:

(Multiple Choice)

4.7/5 (46)

Use the following to answer question:

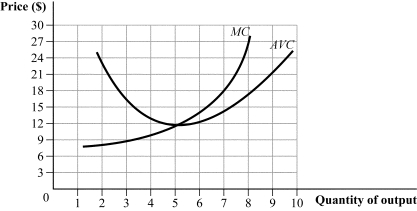

Figure 8.15  -(Figure 8.15) Which of the following statements is (are) TRUE?

-(Figure 8.15) Which of the following statements is (are) TRUE?

(Multiple Choice)

4.9/5 (32)

Pitch (a sticky black substance made from petroleum) is a key input in the production of clay targets. If the price of pitch falls, clay target manufacturers will encounter a(n) _____ shift of their marginal cost curve and a(n)_____ shift of their average variable cost.

(Multiple Choice)

4.8/5 (39)

Suppose that a firm is earning a 12% return on capital in a perfectly competitive industry, and the market return outside the industry is 9.5%. Which of the following statements is (are) TRUE?

(Multiple Choice)

4.8/5 (31)

A March 25, 2010, article at SunSentinel.com reported, "Strawberry farmers in Florida are facing such a sharp collapse in prices for their berries that many are deciding to simply leave huge tracts of the berries to rot in the fields. . . . Wholesale prices that were $17 to $19 for a flat of eight containers have now fallen to $5 to $6 a flat."

(Essay)

4.9/5 (47)

Suppose that the cost curves of the firms do not change when (identical) firms enter or exit the market. Under this scenario, a change in demand will _____ in a change in the market quantity because the number of firms will _____.

(Multiple Choice)

4.7/5 (38)

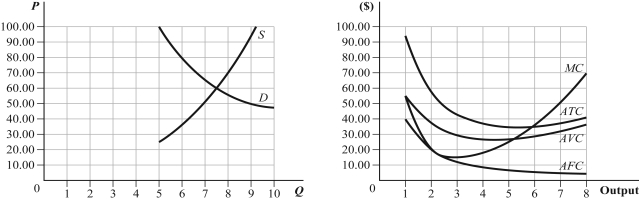

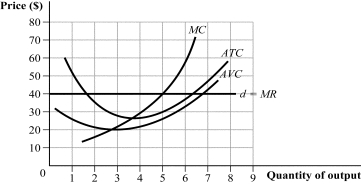

(Graph)  Using the nearby graphs, indicate the short-run equilibrium in this market and calculate any associated profits.

Using the nearby graphs, indicate the short-run equilibrium in this market and calculate any associated profits.

(Essay)

4.9/5 (29)

A firm should _____ output whenever MR exceeds MC because _____.

(Multiple Choice)

4.7/5 (45)

In a perfectly competitive market with 50 firms, output is zero at prices less than $20. At prices of $20 to $29.99, each firm will produce 1 unit of output. At any price of $30 or more, each firm will produce 3 units of output. At a price of $27, the industry produces _____ units, and at a price of $35, the industry produces _____units.

(Multiple Choice)

4.8/5 (35)

In the lemonade stand industry, Lucy is representative of a low-cost provider and Charlie is representative of a high-cost provider. The minimum average total cost of the high-cost producers is $5. The low-cost producers have a long-run total cost curve given by LTC = 5Q -1.5Q2 + 0.33Q3, where LMC = 5 - 3Q + Q2. How much economic rent does the low-cost producer, such as Lucy, earn?

(Essay)

4.8/5 (36)

Use the following to answer question:

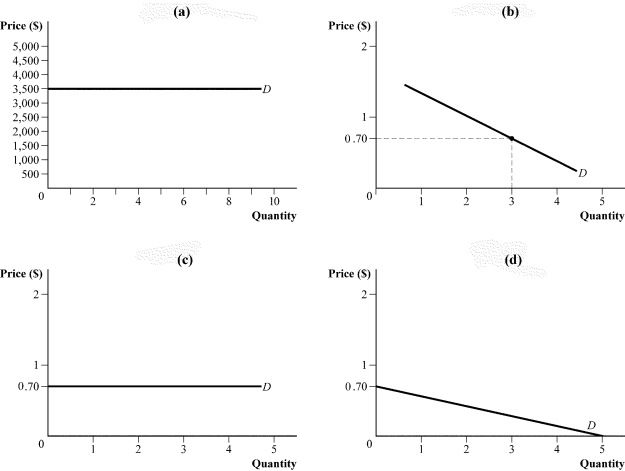

Figure 8.4  -(Figure 8.4) In a perfectly competitive market with 5,000 firms, the equilibrium price and quantity are $0.70 and 3.0 million units. The demand curve facing a firm in this market is represented by:

-(Figure 8.4) In a perfectly competitive market with 5,000 firms, the equilibrium price and quantity are $0.70 and 3.0 million units. The demand curve facing a firm in this market is represented by:

(Multiple Choice)

4.9/5 (33)

If the long-run total cost curve for each firm is given by TC = 1,000 + 100Q - 10Q2 + Q3, in the long run, the marginal cost is:

(Multiple Choice)

5.0/5 (43)

Use the following to answer question:

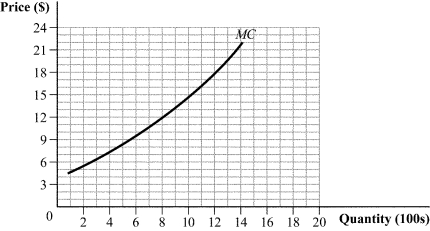

Figure 8.5  -(Figure 8.5) The graph shows a firm's marginal cost curve. This firm operates in a perfectly competitive industry with market demand and supply curves given by Qd = 100 - 8P and QS = -20 + 2P, where Q is measured in millions of units. Based on the figure, how many units of output will the firm produce at the equilibrium price?

-(Figure 8.5) The graph shows a firm's marginal cost curve. This firm operates in a perfectly competitive industry with market demand and supply curves given by Qd = 100 - 8P and QS = -20 + 2P, where Q is measured in millions of units. Based on the figure, how many units of output will the firm produce at the equilibrium price?

(Multiple Choice)

4.8/5 (39)

A street vendor's annual license fee was recently increased by the city. The street vendor's:

(Multiple Choice)

4.9/5 (42)

Use the following to answer question:

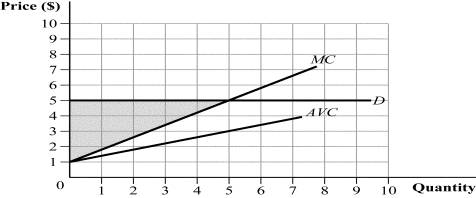

Figure 8.22  -(Figure 8.22) Answer the following questions:

-(Figure 8.22) Answer the following questions:

(Essay)

4.8/5 (42)

Use the following to answer question:

Figure 8.21  -(Figure 8.21) Answer each of the following questions.

-(Figure 8.21) Answer each of the following questions.

(Essay)

4.9/5 (32)

If the long-run total cost curve for each firm is given by TC = 500Q - 20Q2 + Q3, where Q is the quantity of the product, in the long run, the marginal cost is:

(Multiple Choice)

4.8/5 (49)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)