Exam 8: Subsidiary Equity Transactions, Indirect Subsidiary Ownership, and Subsidiary Ownership of Parent Shares

Exam 1: Business Combinations: New Rules for a Long-Standing Business Practice46 Questions

Exam 2: Consolidated Statements: Date of Acquisition41 Questions

Exam 3: Consolidated Statements: Subsequent to Acquisition34 Questions

Exam 4: Intercompany Transactions: Merchandise, Plant Assets, and Notes38 Questions

Exam 5: Intercompany Transactions: Bonds and Leases52 Questions

Exam 6: Cash Flow, Eps, and Taxation46 Questions

Exam 7: Special Issues in Accounting for an Investment in a Subsidiary39 Questions

Exam 8: Subsidiary Equity Transactions, Indirect Subsidiary Ownership, and Subsidiary Ownership of Parent Shares37 Questions

Exam 9: The International Accounting Environment14 Questions

Exam 10: Foreign Currency Transactions67 Questions

Exam 11: Translation of Foreign Financial Statements73 Questions

Exam 12: Interim Reporting and Disclosures About Segments of an Enterprise56 Questions

Exam 13: Partnerships: Characteristics, Formation, and Accounting for Activities45 Questions

Exam 14: Partnerships: Ownership Changes and Liquidations57 Questions

Exam 15: Governmental Accounting: the General Fund and the Account Groups74 Questions

Exam 16: Governmental Accounting: Other Governmental Funds, Proprietary Funds, and Fiduciary Funds58 Questions

Exam 17: Financial Reporting Issues29 Questions

Exam 18: Accounting for Private Not-For-Profit Organizations55 Questions

Exam 19: Accounting for Not-For-Profit Colleges and Universities and Health Care Organizations79 Questions

Exam 20: Estates and Trusts: Their Nature and the Accountants Role52 Questions

Exam 21: Debt Restructuring, Corporate Reorganizations, and Liquidations43 Questions

Exam 22: Accounting for Influential Investments13 Questions

Exam 23: Derivatives and Related Accounting Issues45 Questions

Select questions type

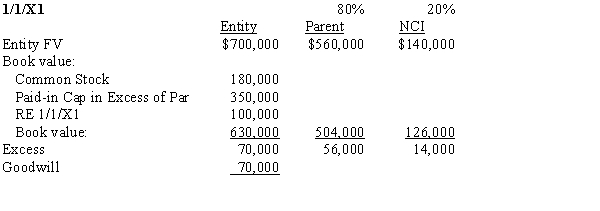

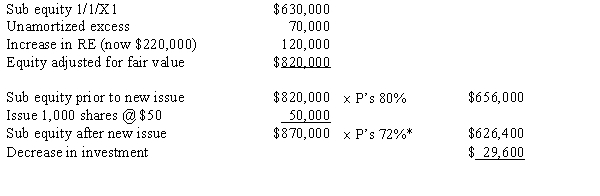

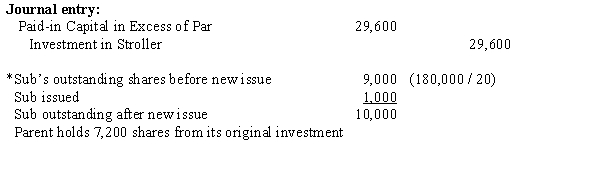

On 1/1/X1 Poncho acquired an 80% interest in Stroller for $560,000 when Stroller's equity consisted of $530,000 paid-in capital and $100,000 Retained Earnings. Any excess of purchase price over was attributed to goodwill.

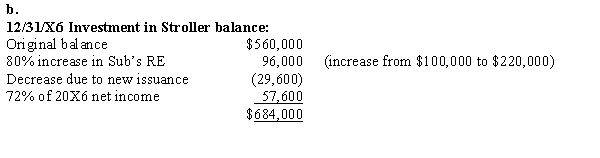

On January 1, 20X6, Stroller had the following stockholders' equity:  On January 2, 20X6, Company S sold 1,000 additional shares to noncontrolling shareholders in a public offering for $50 per share. Stroller's net income for 20X6 was 80,000. Poncho uses the simple equity method to record its investment in Stroller.

Required:

a.Prepare Poncho's journal entry to adjust its Investment in Stroller account on January 2, 20X6. Assume that Poncho has $500,000 additional paid-in capital.

b.Determine the carrying value of Poncho's Investment in Stroller account on December 31, 20X6.

On January 2, 20X6, Company S sold 1,000 additional shares to noncontrolling shareholders in a public offering for $50 per share. Stroller's net income for 20X6 was 80,000. Poncho uses the simple equity method to record its investment in Stroller.

Required:

a.Prepare Poncho's journal entry to adjust its Investment in Stroller account on January 2, 20X6. Assume that Poncho has $500,000 additional paid-in capital.

b.Determine the carrying value of Poncho's Investment in Stroller account on December 31, 20X6.

Free

(Essay)

4.8/5  (29)

(29)

Correct Answer: Verified

Verified

a.

Pepper Company owned 60,000 of Salt Company's 100,000 outstanding shares. On January 2, 20X3, Salt purchased 20,000 of its outstanding shares from the NCI for $70,000. Pepper purchased its shares on January 1, 20X1, at which time the fair value of Salt exceeded its book value by $50,000. This difference was due to machinery that was undervalued and had a remaining life of 5 years. On December 31, 20X2, Salt Company had the following stockholders' equity:

Common stock, $1 par

$100,000

Paid-in capital in excess of par

50,000

Retained earnings

270,000

Assuming Pepper uses the equity method to account for its investment in Salt, the adjustment to the Pepper's books would include:

Free

(Multiple Choice)

4.8/5 (43)

Correct Answer:Verified

B

On January 1, 20X1, Paris Ltd. paid $600,000 for its 75% interest in the Scott Company when Scott had total equity of $550,000. Any excess of cost over book value was attributed to equipment with a 10-year life. On January 1, 20X3, Scott Company had the following stockholders' equity:  On January 2, 20X3, Scott Company sold 2,500 additional shares of stock for $60 each in a private offering to noncontrolling shareholders. As a result of this sale, which of the following changes would appear in the 20X3 consolidated statements?

On January 2, 20X3, Scott Company sold 2,500 additional shares of stock for $60 each in a private offering to noncontrolling shareholders. As a result of this sale, which of the following changes would appear in the 20X3 consolidated statements?

Free

(Multiple Choice)

4.8/5 (44)

Correct Answer:Verified

C

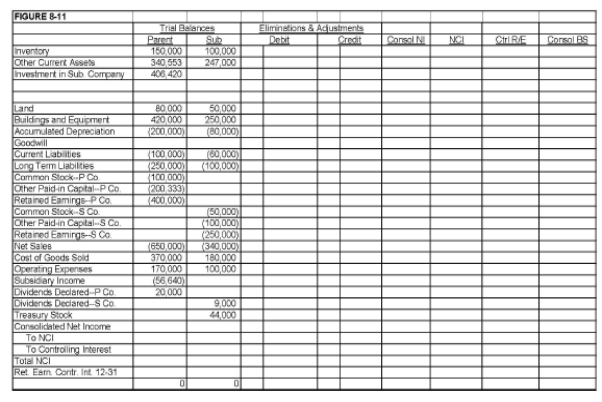

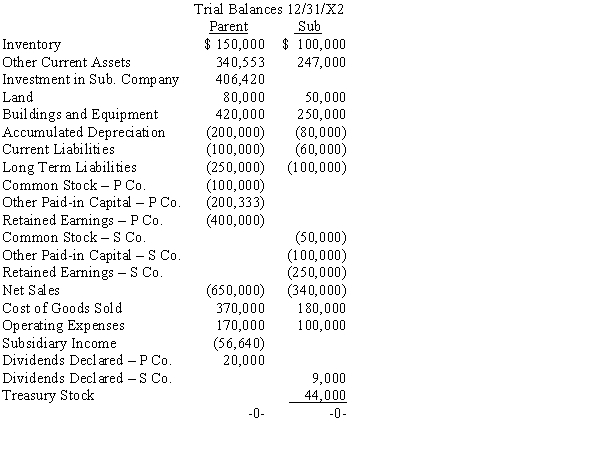

On January 1, 20X1, Parent Company purchased 85% of the common stock, 8,500 shares, of Subsidiary Company for $317,500. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill.

On January 1, 20X2, Subsidiary purchased, from its noncontrolling shareholders, 1,000 shares of its common stock, 10% of the stock outstanding on that date. The price paid was $44,000.

Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.Prepare an analysis to determine Parent's revised ownership interest following Sub's treasury stock transaction.

b.Complete the Figure 8-11 worksheet for consolidated financial statements for 20X2

(Essay)

5.0/5 (37)

Pepper Company owns 60,000 of Salt Company's 100,000 outstanding shares. This year, Salt purchased 20,000 of its outstanding shares from the NCI for $70,000. Pepper's interest after the treasury stock purchase is:

(Multiple Choice)

4.8/5 (29)

Company P purchased a 80% interest in the Company S on January 1, 20X1, for $600,000. Any excess of cost is attributed to the Company's building with a 20-year life. The equity balances of Company S are as follows:  The only change in paid-in capital is a result of a 40% stock dividend paid in 20X3. The cost to simple equity conversion to bring the investment account to its December 31, 20X4, balance is ____.

The only change in paid-in capital is a result of a 40% stock dividend paid in 20X3. The cost to simple equity conversion to bring the investment account to its December 31, 20X4, balance is ____.

(Multiple Choice)

4.8/5 (31)

Apple Inc. owns a 90% interest in Banana Company. Banana Company, in turn, owns a 80% interest in Carrot Company. During 20X4, Carrot Company sold $50,000 of merchandise to Apple Inc. at a gross profit of 20%. Of this merchandise, $10,000 was still unsold by Apple Inc. at year end. The adjustment to the controlling interest in consolidated net income for 20X4 is ____.

(Multiple Choice)

4.8/5 (47)

When a parent purchases a portion of the newly issued stock of its subsidiary in a private offering and the ownership interest decreases,

(Multiple Choice)

4.8/5 (38)

On January 1, 20X1, Parent Company purchased 85% of the common stock, 8,500 shares, of Subsidiary Company for $317,500. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill.

On January 1, 20X2, Subsidiary purchased, from its noncontrolling shareholders, 1,000 shares of its common stock, 10% of the stock outstanding on that date. The price paid was $44,000. The trial balances of Parent and Sub as of 12/31/X2 are given below:  Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.Prepare the D&D schedule for the 1/1/X1 acquisition.

b.Prepare a schedule to determine the change in Parent's interest in Sub.

c.Prepare the journal entry the parent needed to adjust its interest in Sub. (Note that it has already been included in the parent's trial balance.)

d.Prepare, in journal form, all elimination entries necessary for the 12/31/X2 consolidation worksheet.

Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.Prepare the D&D schedule for the 1/1/X1 acquisition.

b.Prepare a schedule to determine the change in Parent's interest in Sub.

c.Prepare the journal entry the parent needed to adjust its interest in Sub. (Note that it has already been included in the parent's trial balance.)

d.Prepare, in journal form, all elimination entries necessary for the 12/31/X2 consolidation worksheet.

(Essay)

4.9/5 (38)

Pepper Company owned 60,000 of Salt Company's 100,000 outstanding shares. On January 2, 20X3, Salt purchased 20,000 of its outstanding shares from the NCI for $70,000. Pepper purchased its shares on January 1, 20X1, at which time the fair value of Salt exceeded its book value by $50,000. This difference was due to machinery that was undervalued and had a remaining life of 5 years. On December 31, 20X2, Salt Company had the following stockholders' equity:  The amount of the adjustment to Pepper's equity would be a:

The amount of the adjustment to Pepper's equity would be a:

(Multiple Choice)

4.9/5 (41)

Company P had 300,000 shares of common stock outstanding. It owned 80% of the outstanding common stock of S. S owned 20,000 shares of P common stock. In the consolidated balance sheet, Company P's outstanding common stock may be shown as

(Multiple Choice)

4.8/5 (39)

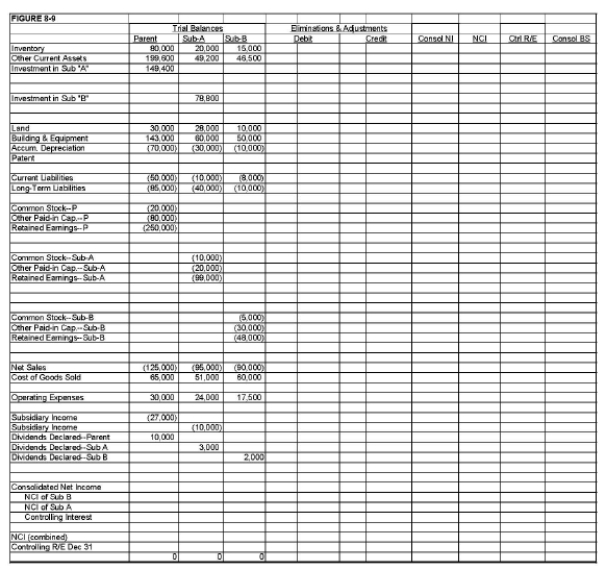

On January 1, 20X1, Parent Company purchased 90% of the common stock of Sub-A Company for $90,000. On this date, Sub-A had common stock, other paid-in capital, and retained earnings of $10,000, $20,000, and $60,000 respectively.

On January 1, 20X2, Sub-A Company purchased 80% of the common stock of Sub-B Company for $64,000. On this date, Sub-B Company had common stock, other paid-in capital, and retained earnings of $5,000, $30,000, and $40,000 respectively.

Any excess of cost over book value on either purchase is due to a patent, to be amortized over ten years.

Both Parent and Sub-A have accounted for their investments using the simple equity method.

During 20X2, Sub-B sold merchandise to Sub-A for $20,000, of which one-fourth is still held by Sub-B on December 31, 20X2. Sub-B's usual gross profit is 40%. During 20X3, Sub-B sold more goods to Sub-A for $30,000, of which $10,000 is still on hand on December 31, 20X3.

Required:

Complete the Figure 8-9 worksheet for consolidated financial statements for 20X3.

(Essay)

4.9/5 (33)

Company P owns 80% of the 10,000 outstanding common stock of Company S. If Company S issues 2,500 added shares of common stock, and Company P purchases some of the newly issued shares, which of the following statements is true?

(Multiple Choice)

4.8/5 (34)

On January 1, 20X1, Parent Company purchased 9,000 shares of the common stock of Subsidiary Company for $405,000. On this date, Subsidiary had 20,000 shares of $5 par common stock authorized, 10,000 shares issued and outstanding. Other paid-in capital and retained earnings were $150,000 and $200,000 respectively. On January 1, 20X1, any excess of cost over book value is due to a patent, to be amortized over 10 years.

Subsidiary's net income and dividends for two years were:  On January 1, 20X2, Subsidiary Company sold an additional 2,000 shares of common stock for $50 per share. Parent purchased 1,200 shares of the new issue, and noncontrolling shareholders purchased the other 800.

For both 20X1 and 20X2, Parent Company has applied the simple equity method.

Required:

a.Prepare a schedule that measures Parent's change in interest ownership effective with Sub's issuance of the 2,000 shares and Parent's acquisition of 1,200 of those shares.

b.Prepare Parent's journal entry to record its purchase of the 1,200 shares on 1/1/X2

c.Prepare a schedule showing the 12/31/X2 balance of Parent's Investment in Sub account

On January 1, 20X2, Subsidiary Company sold an additional 2,000 shares of common stock for $50 per share. Parent purchased 1,200 shares of the new issue, and noncontrolling shareholders purchased the other 800.

For both 20X1 and 20X2, Parent Company has applied the simple equity method.

Required:

a.Prepare a schedule that measures Parent's change in interest ownership effective with Sub's issuance of the 2,000 shares and Parent's acquisition of 1,200 of those shares.

b.Prepare Parent's journal entry to record its purchase of the 1,200 shares on 1/1/X2

c.Prepare a schedule showing the 12/31/X2 balance of Parent's Investment in Sub account

(Essay)

4.9/5 (42)

When a parent purchases a portion of the newly issued stock of its subsidiary and the ownership interest increases,

(Multiple Choice)

4.9/5 (32)

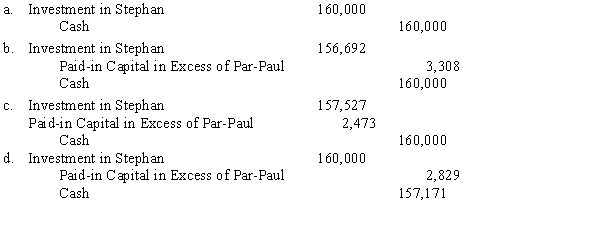

On January 1, 20X1, Paul, Inc. acquired a 90% interest in Stephan Company. The $45,000 excess of purchase price (parent's share only) was attributable to goodwill. On January 1, 20X3, Stephan Company had the following stockholders' equity:  On January 2, 20X3, Stephan sold 2,000 additional shares in a private offering. Stephan issued the new shares for $80 per share; Paul, Inc. purchased all the shares. What is the journal entry that Paul will prepare to record this investment?

On January 2, 20X3, Stephan sold 2,000 additional shares in a private offering. Stephan issued the new shares for $80 per share; Paul, Inc. purchased all the shares. What is the journal entry that Paul will prepare to record this investment?

(Short Answer)

5.0/5 (40)

When a subsidiary purchases shares of the parent, on a consolidated basis:

(Multiple Choice)

4.9/5 (27)

Which of the following situations is viewed as the parent having treasury stock?

(Multiple Choice)

4.9/5 (36)

Able Company owns an 80% interest in Barns Company and a 20% interest in Carns Company. Barns owns a 40% interest in Carns Company.

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)