Exam 4: Recognizing Revenues in Governmental Funds

Exam 1: The Government and Not-For-Profit Environment50 Questions

Exam 2: Fund Accounting50 Questions

Exam 3: Issues of Budgeting and Control50 Questions

Exam 4: Recognizing Revenues in Governmental Funds62 Questions

Exam 5: Recognizing Expenditures in Governmental Funds67 Questions

Exam 6: Accounting for Capital Projects and Debt Service69 Questions

Exam 7: Capital Assets and Investments in Marketable Securities58 Questions

Exam 8: Long-Term Obligations53 Questions

Exam 9: Business-Type Activities66 Questions

Exam 10: Pensions and Other Fiduciary Activities64 Questions

Exam 11: Issues of Reporting, Disclosure, and Financial Analysis68 Questions

Exam 12: Not-For-Profit Organizations63 Questions

Exam 13: Colleges and Universities39 Questions

Exam 14: Health Care Providers47 Questions

Exam 15: Managing for Results50 Questions

Exam 16: Auditing Governments and Notforprofit Organizations59 Questions

Exam 17: Federal Government Accounting66 Questions

Select questions type

Under the modified accrual basis of accounting, the amount of property tax revenues that should be recognized by a government in the current year related to the current-year levy will be

(Multiple Choice)

4.9/5  (37)

(37)

A city receives notice of a $150,000 grant from the state to purchase vans to transport physically challenged individuals.Although the city did not receive any of the grant funds during the current year, the city purchased a bus for $65,000 and issued a purchase order for a van for $60,000.The grant revenue that the city should recognize in the government-wide financial statements in the current year is

(Multiple Choice)

4.7/5 (38)

Under the modified accrual basis, revenues are "available" if they are collected within the current period or are expected to be collected soon enough after the end of the period to be used to pay liabilities of the current period.

(True/False)

4.8/5 (42)

At the beginning of its fiscal year, a local government owned an investment with a historical cost of $85 and a fair value of $95.During the year, dividends of $2 were received.At the end of the year, the investment had a fair value of $100.The amount that should be recognized on the governmental fund financial statements for the year as investment income is

(Multiple Choice)

4.8/5 (42)

Endowments are provided to governments with the specification that only the revenues generated from-not the contributed assets-may be used to finance specific programs.A government should recognize revenue from the initial endowment when

(Multiple Choice)

4.7/5 (38)

A local government began the year with a portfolio of securities with an historical cost of $1,200 and a fair value of $1,240.During the year the government acquired an additional security at a cost of $260 and sold for $200 a security that had an historical cost of $172 and a fair value at the beginning of the year of $190.At the end of the year, the securities portfolio had a fair value of $1,330.The amount that should be recognized on the financial statements for the year as investment income is

(Multiple Choice)

4.9/5 (40)

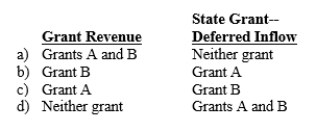

Paul City received payment of two grants from the state during its fiscal year ending September 30, 2013.Grant A can be used to cover any operating expenses incurred during fiscal 2014.Grant B can be used at any time to acquire equipment for the city's fire department.Should the city report these grants as grant revenues or deferred inflows in its government-wide financial statements for fiscal 2013?

(Short Answer)

4.7/5 (33)

A city levies a 2 percent sales tax.Sales taxes must be remitted by the merchants to the city by the twentieth day of the month following the month in which the sale occurred.Cash received by the city related to sales taxes is as follows:  Assuming the city uses the same period to define "available" as the maximum period allowable for property taxes, what amount should it recognize in the government-wide financial statements as sales tax revenue for the fiscal year ended 12/31/14?

Assuming the city uses the same period to define "available" as the maximum period allowable for property taxes, what amount should it recognize in the government-wide financial statements as sales tax revenue for the fiscal year ended 12/31/14?

(Multiple Choice)

4.9/5 (40)

A city that has a 12/31 fiscal year end has adopted a policy of recognizing the maximum amount of property tax revenue allowable under GAAP.Property taxes of $720,000 (of which 10 percent are estimated to be uncollectible)are levied in October 2013 to finance the activities of the fiscal year 2014.During 2014, cash collections related to property taxes levied in October 2013 were $600,000.In 2015the following amounts related to the property taxes levied in October 2013 were collected: January $30,000; March $6,000.For the fiscal year ended 12/31/14, what amount should be recognized as property tax revenues related to the 2013 levy on the government-wide financial statements?

(Multiple Choice)

4.8/5 (39)

Revenues that cannot be classified as general revenues are by default considered program revenues.

(True/False)

4.7/5 (34)

During 2014, a state has the following cash collections related to state income taxes  Assuming that the state defines "available" as the maximum period allowable for property taxes, what is the amount of revenue that will be recognized in the 2014 governmental fund financial statements related to state income taxes?

Assuming that the state defines "available" as the maximum period allowable for property taxes, what is the amount of revenue that will be recognized in the 2014 governmental fund financial statements related to state income taxes?

(Multiple Choice)

4.9/5 (44)

Sales taxes are taxpayer assessed, that is, parties other than the beneficiary government determine the tax base.

(True/False)

4.8/5 (36)

Governmental activities tend to derive the majority of their revenues from exchange transactions.

(True/False)

4.7/5 (39)

Under the accrual basis of accounting, imposed nonexchange revenues (such as fines)should be recognized

(Multiple Choice)

4.8/5 (31)

Under the modified accrual basis of accounting, derived nonexchange revenues are recognized when

(Multiple Choice)

4.7/5 (37)

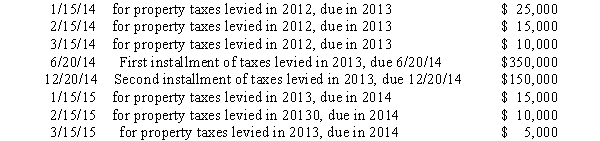

A city that has a 12/31 fiscal year end has adopted a policy of recognizing property tax revenue consistent with the 60-day rule allowable period under GAAP.Property taxes of $600,000 (of which none are estimated to be uncollectible)are levied in October 2013 to finance the activities of fiscal year 2014.Property taxes are due in two installments June 20 and December 20.Cash collections related to property taxes are as follows:  The total amount of property tax revenue that should be recognized in the governmental fund financial statements in 2014 is:

The total amount of property tax revenue that should be recognized in the governmental fund financial statements in 2014 is:

(Multiple Choice)

4.9/5 (44)

Which of the following are not characterized as non-exchange revenues?

(Multiple Choice)

4.7/5 (34)

Payments made to a state pension plan by the state government on behalf of a local government should

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)