Exam 4: Recognizing Revenues in Governmental Funds

Exam 1: The Government and Not-For-Profit Environment50 Questions

Exam 2: Fund Accounting50 Questions

Exam 3: Issues of Budgeting and Control50 Questions

Exam 4: Recognizing Revenues in Governmental Funds62 Questions

Exam 5: Recognizing Expenditures in Governmental Funds67 Questions

Exam 6: Accounting for Capital Projects and Debt Service69 Questions

Exam 7: Capital Assets and Investments in Marketable Securities58 Questions

Exam 8: Long-Term Obligations53 Questions

Exam 9: Business-Type Activities66 Questions

Exam 10: Pensions and Other Fiduciary Activities64 Questions

Exam 11: Issues of Reporting, Disclosure, and Financial Analysis68 Questions

Exam 12: Not-For-Profit Organizations63 Questions

Exam 13: Colleges and Universities39 Questions

Exam 14: Health Care Providers47 Questions

Exam 15: Managing for Results50 Questions

Exam 16: Auditing Governments and Notforprofit Organizations59 Questions

Exam 17: Federal Government Accounting66 Questions

Select questions type

A city is the recipient of a cash bequest of $500,000 that must be used to plant flowers and shrubs in the city parks.During the year only $200,000 is actually received from the bequest and $150,000 is spent on shrubs.The amount that should be recognized as revenue by the city in its government-wide financial statements in the current year is

Free

(Multiple Choice)

4.9/5  (38)

(38)

Correct Answer: Verified

Verified

C

As used in defining the modified accrual basis of accounting, the term "available" means

Free

(Multiple Choice)

4.9/5 (34)

Correct Answer:Verified

D

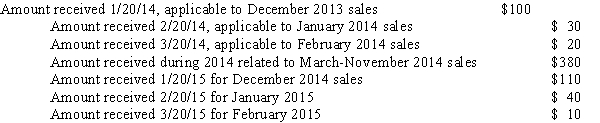

A city with a 12/31 fiscal year-end requires that restaurants buy a license, renewable yearly.Proceeds of the license fees are intended to pay the salaries of inspectors in the health department.Licenses are issued for a fiscal year from October 1 to September 30.During 2014, cash collections related to licenses were as follows  It is anticipated that during 2015 the amount collected on licenses for the 10/1/14-9/30/15 fiscal year will be $45.In September 2013 the amount collected related to 10/1/13-9/30/14 licenses was $144.What amount should be recognized as revenue in the fund financial statements for the fiscal year ended 12/31/14?

It is anticipated that during 2015 the amount collected on licenses for the 10/1/14-9/30/15 fiscal year will be $45.In September 2013 the amount collected related to 10/1/13-9/30/14 licenses was $144.What amount should be recognized as revenue in the fund financial statements for the fiscal year ended 12/31/14?

Free

(Multiple Choice)

4.8/5 (37)

Correct Answer:Verified

C

Taxes that are imposed on the reporting government's citizens are considered general revenues, even if they are restricted to specific programs.

(True/False)

4.8/5 (30)

Under the modified accrual basis of accounting, license fees, permits, and other miscellaneous revenue are generally recognized for practical purposes

(Multiple Choice)

4.8/5 (44)

A city levies a 2 percent sales tax that is collected for them by the state.Sales taxes must be remitted by the merchants to the state by the twentieth day of the month following the month in which the sale occurred.The state has a policy of remitting sales taxes to the city within 30 days of collection by the state.Cash received by the state related to sales taxes is as follows:  Assuming the city uses the same period to define "available" as the maximum period allowable for property taxes, what amount should it recognize as sales tax revenue in its government-wide financial statements for the fiscal year ended 12/31/14?

Assuming the city uses the same period to define "available" as the maximum period allowable for property taxes, what amount should it recognize as sales tax revenue in its government-wide financial statements for the fiscal year ended 12/31/14?

(Multiple Choice)

5.0/5 (38)

During 2014, a state has the following cash collections related to state income taxes  Assuming that the state defines "available" as the maximum period allowable for property taxes, what is the amount of revenue that will be recognized in the 2014 government-wide financial statements related to state income taxes?

Assuming that the state defines "available" as the maximum period allowable for property taxes, what is the amount of revenue that will be recognized in the 2014 government-wide financial statements related to state income taxes?

(Multiple Choice)

4.9/5 (48)

During 2014, the city issued $300 in fines for failure to keep real property in 'acceptable' condition.During that period the city spent $200 to mow and clean up the unoccupied properties for which the fines were assessed.The city estimates that $30 of the fines issued in 2014 will be uncollectible.During 2014 the city collected $230 related to 2014 fines and $20 related to 2013 fines.The amount of revenue that the city should recognize in its 2014 governmental fund financial statements related to fines is

(Multiple Choice)

4.8/5 (45)

Reimbursement-type grant revenues are recognized in the accounting period in which

(Multiple Choice)

4.9/5 (51)

Under the accrual basis of accounting used by governments, investment revenues for the current period should include

(Multiple Choice)

4.7/5 (34)

If an entity elects to focus on all economic resources, then it should adopt a modified accrual basis of accounting.

(True/False)

4.9/5 (35)

A government is the recipient of a bequest of a multi-story office building that the government intends to use as a new city hall.The building has a historical cost of $850,000; a book value in the hands of the benefactor of $700,000; and a fair value of $1,050,000.The city should recognize on its governmental fund financial statements donations revenue of

(Multiple Choice)

4.7/5 (30)

The modified accrual basis of accounting is used in presenting the fund financial statements of the governmental funds because

(Multiple Choice)

4.8/5 (38)

Under the modified accrual basis of accounting, gains and losses on disposal of capital assets

(Multiple Choice)

4.9/5 (45)

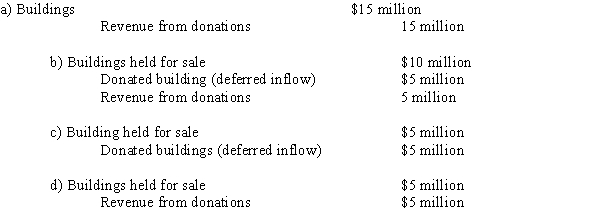

A wealthy philanthropist donates three buildings to H-Town.Each building has a fair market value of $5 million.The town plans to use Building 1 as a new fire station and sell Buildings 2 and 3. Building 2 is sold after year-end, but within the availability period.Building 3 fails to sell by the time the town issues the financial statements.Which of the following correctly records revenue from these donations in the governmental fund financial statements?

(Short Answer)

4.9/5 (40)

Under the modified accrual basis of accounting, imposed nonexchange revenues (such as fines)should be recognized

(Multiple Choice)

4.9/5 (42)

Under GAAP, property taxes levied in one fiscal period to finance the activities of the following fiscal period are recognized as revenue in the governmental fund financial statements

(Multiple Choice)

4.9/5 (31)

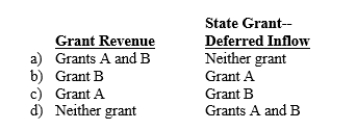

Paul City received payment of two grants from the state during its fiscal year ending September 30, 2013.Grant A can be used to cover any operating expenses incurred during fiscal 2014.Grant B can be used at any time to acquire equipment for the city's fire department.Should the city report these grants as grant revenues or deferred inflows in its governmental fund financial statements for fiscal 2013?

(Short Answer)

4.9/5 (49)

The budgetary measurement focus of governments is determined by applicable state or local laws.

(True/False)

4.7/5 (38)

Under the accrual basis of accounting, property tax revenues are recognized

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)