Exam 18: Standard Costing and Variance Analysis 2: Further Aspects

When should a variance be investigated?

Random variations around the standard are expected. When variances are within this range, they are assumed to be caused by random factors. When a variance falls outside of this range, the deviation is likely to be caused by nonrandom factors, either factors that managers can control or factors they cannot control. However, investigating the cause of variances and taking corrective action have a cost associated with them. As a general principle, an investigation should be undertaken only if the anticipated benefits are greater than the expected costs. Assessing the costs and benefits of a variance investigation is not an easy task, however.

Many firms adopt the general guideline of investigating variances only if they fall outside of an acceptable range. They are not investigated unless they are large enough to be of concern. They must be large enough to be caused by something other than random factors and large enough (on average) to justify the costs of investigating and taking corrective action.

Figure 18-3

Pippen Company's activity-based performance report revealed that actual inspection costs totaled £100,000 at an actual activity level of 50 inspections. Further analysis of inspection costs revealed the following:  Fixed inspection costs consist of the salaries of two inspectors, who are paid £14,250. Each inspector is capable of efficiently conducting inspections of 30 batches.

Variable inspection costs consist of materials used during the inspections.

-Refer to Figure 18-3. The fixed spending variance is

Fixed inspection costs consist of the salaries of two inspectors, who are paid £14,250. Each inspector is capable of efficiently conducting inspections of 30 batches.

Variable inspection costs consist of materials used during the inspections.

-Refer to Figure 18-3. The fixed spending variance is

A

Figure 18-2

Allende Company has developed capacity standards. Information is as follows for a value-added activity:  -Refer to Figure 18-2. The unused capacity variance is

-Refer to Figure 18-2. The unused capacity variance is

C

Figure 18-1

Froelech Company has developed capacity standards. Information is as follows:  -Refer to Figure 18-1. The unused capacity variance is

-Refer to Figure 18-1. The unused capacity variance is

Figure 18-3

Pippen Company's activity-based performance report revealed that actual inspection costs totaled £100,000 at an actual activity level of 50 inspections. Further analysis of inspection costs revealed the following: Fixed inspection costs consist of the salaries of two inspectors, who are paid £14,250. Each inspector is capable of efficiently conducting inspections of 30 batches.

Variable inspection costs consist of materials used during the inspections.

-Refer to Figure 18-3. The volume variance is

Figure 18-4

Regis Ltd. uses two materials in the production of its product. The materials, X and Y, have the following standards:  During April, the following actual production information was provided:

During April, the following actual production information was provided:  -Refer to Figure 18-4. What is the materials usage variance?

-Refer to Figure 18-4. What is the materials usage variance?

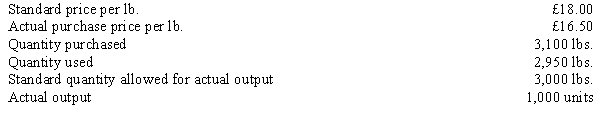

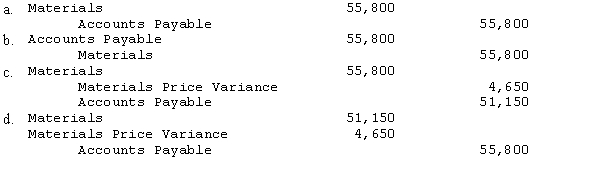

Roberts Company uses a standard costing system. The following information pertains to direct materials for the month of July:  Roberts Company reports its material price variances at the time of purchase. What is the journal entry to record material purchases?

Roberts Company reports its material price variances at the time of purchase. What is the journal entry to record material purchases?

Figure 18-1

Froelech Company has developed capacity standards. Information is as follows:

-Refer to Figure 18-1. The volume variance is

Figure 18-4

Regis Ltd. uses two materials in the production of its product. The materials, X and Y, have the following standards: During April, the following actual production information was provided:

-Refer to Figure 18-4. What is the materials yield variance?

Laune Co.'s standard cost is £200,000, and its allowable deviation is £20,000. Laune's upper and lower control limits are

Figure 18-4

Regis Ltd. uses two materials in the production of its product. The materials, X and Y, have the following standards: During April, the following actual production information was provided:

-Refer to Figure 18-4. What is the materials mix variance?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)