Exam 14: Financing Liabilities: Bonds and Long-Term Notes Payable

Exam 1: The Demand for and Supply of Financial Accounting Information85 Questions

Exam 2: Financial Reporting: Its Conceptual Framework83 Questions

Exam 3: Review of a Company S Accounting System148 Questions

Exam 4: The Balance Sheet and the Statement of Shareholders Equity127 Questions

Exam 5: The Income Statement and the Statement of Cash Flows Time Value of Money Module136 Questions

Exam 6: Cash and Receivables172 Questions

Exam 7: Inventories: Cost Measurement and Flow Assumptions114 Questions

Exam 8: Inventories: Special Valuation Issues141 Questions

Exam 9: Current Liabilities and Contingent Obligations125 Questions

Exam 10: Property, Plant, and Equipment: Acquisition and Subsequent Investments111 Questions

Exam 11: Depreciation, Depletion, Impairment, and Disposal136 Questions

Exam 12: Intangibles136 Questions

Exam 13: Investments and Long-Term Receivables135 Questions

Exam 14: Financing Liabilities: Bonds and Long-Term Notes Payable192 Questions

Exam 15: Contributed Capital153 Questions

Exam 16: Retained Earnings and Earnings Per Share110 Questions

Exam 17: Advanced Issues in Revenue Recognition103 Questions

Exam 18: Accounting for Income Taxes113 Questions

Exam 19: Accounting for Post-Retirement Benefits94 Questions

Exam 20: Accounting for Leases116 Questions

Exam 21: The Statement of Cash Flows103 Questions

Exam 22: Accounting for Changes and Errors130 Questions

Exam 23: Understanding Time Value of Money Formulas and Concepts142 Questions

Select questions type

Exhibit 14-2

A $500,000, ten-year, 7% bond issue was sold to yield 6% interest payable annually. Actuarial information for 10 periods is as follows:  -Refer to Exhibit 14-2. At date of issuance cash received would be

-Refer to Exhibit 14-2. At date of issuance cash received would be

(Multiple Choice)

4.9/5  (40)

(40)

In the event of a debt restructuring, the required disclosures are only for the related income tax effects associated with the debt.

(True/False)

4.8/5 (26)

The effective interest method of amortization assumes a stable

(Multiple Choice)

4.8/5 (28)

When the market rate of interest is equal to the contract rate of interest, the bonds should sell at

(Multiple Choice)

4.8/5 (43)

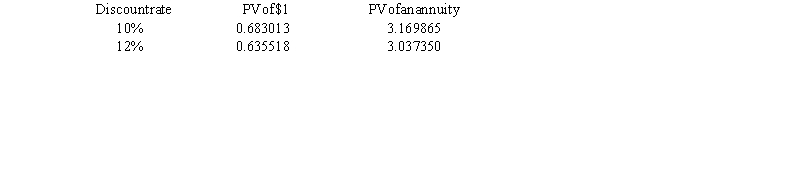

On December 31, 2015, Albright Bank restructures an $800,000, 12% note receivable with $192,000 of accrued interest so that the new principal is $750,000, payable in four years at 10%. Present value factors for n = 4 years are:  Required:

a. Prepare the journal entry to record the loss on restructuring.

b. Prepare the journal entry to record the 2015 interest revenue.

c. Compute the carrying value of the note on December 31, 2013.

d. Compute the carrying value of the note on December 31, 2019 before the payment is received.

Required:

a. Prepare the journal entry to record the loss on restructuring.

b. Prepare the journal entry to record the 2015 interest revenue.

c. Compute the carrying value of the note on December 31, 2013.

d. Compute the carrying value of the note on December 31, 2019 before the payment is received.

(Essay)

4.9/5 (33)

Exhibit 14-10

Hawk issued $500,000 of its ten-year 5% bonds for $463,197 on October 1, 2016 so as to yield an effective rate of 6%. Interest is paid each October 1 and April 1

-Refer to Exhibit 14-9. Assuming Hawk uses the effective interest method, the adjusting entry on December 31, 2016, would include

(Multiple Choice)

4.8/5 (36)

The rate of interest used to compute the present value of an impaired note is the

(Multiple Choice)

4.8/5 (38)

Nassau Co. owes Dominion Ltd. $115,000 on a note payable, plus $7,500 interest. Dominion agrees to accept land in full settlement. The land is recorded on the books of Nassau at $55,600 and is currently worth $85,000.

Required:

Prepare the journal entries to record the debt settlement on the books of Nassau.

(Essay)

4.9/5 (41)

Which of the following is not a reason for the issuance of long-term liabilities?

(Multiple Choice)

4.8/5 (38)

When a company amortizes a premium, the interest expense recorded is

(Multiple Choice)

4.9/5 (33)

Cherry Corporation sold $200,000 of 12% bonds at par. Each $1,000 bond carried ten warrants, each of which allows the holder to acquire one share of $10 par common stock for $30 per share. After issuance, the bonds were quoted at 99 ex rights, and the warrants were quoted at $4 each. Cherry Corporation should have assigned to the rights a value of

(Multiple Choice)

4.9/5 (31)

In June 2016, Goslyn Corporation issued a three-year non-interest-bearing note with a face value of $15,000 and received cash of $11,025.00 in exchange. The difference between the face value and the cash proceeds is accounted for as

(Multiple Choice)

4.8/5 (32)

If a company sells its bonds at face value, the effective interest rate is

(Multiple Choice)

4.8/5 (39)

At issuance, bonds payable with a conversion privilege are accounted for as

(Multiple Choice)

4.9/5 (38)

The Bellefonte Company is delinquent on a $100,000, 12% note plus $20,000 accrued interest to the Hollywood National Bank. The note was due on June 1, 2016. On June 2, 2016, the bank agrees to restructure the debt by forgiving the accrued interest, reducing the face value of the note to $90,000, reducing the interest rate to 7%, and extending the maturity date to June 1, 2019. The interest is due each year on June 1.

Required:

Prepare the journal entries for Bellefonte Company to record the restructuring on June 2, 2016, and the payment of interest on June 1, 2017.

(Essay)

4.7/5 (42)

Sand Castle Co. borrowed $40,000 by issuing a four-year non-interest-bearing note to a customer. In addition, Sand Castle agreed to sell inventory to the same customer at reduced prices over the four-year period. Sand Castle's incremental borrowing rate was 8%, so the present value of the note was $29,400. The customer agreed to purchase an equal amount of inventory each year over the four-year period.

Required:

Prepare journal entries to:

a. Issue the note

b. Adjust at the end of the first year

c. Adjust at the end of the second year

(Essay)

4.8/5 (44)

Exhibit 14-6

Jones Corporation issued $400,000 of its 8%, 10-year bonds, dated January 1, 2016, at face value plus accrued interest on May 1, 2016. Interest is paid on January 1 and July 1. Jones uses the most common method to record the sale of the bonds between interest payment periods.

-Refer to Exhibit 14-6. The entry to record the sale would include a

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)