Exam 15: Auditing the Expenditure Cycle

Exam 1: Auditing and the Public Accounting69 Questions

Exam 2: Financial Statement Audits and84 Questions

Exam 3: Professional Ethics86 Questions

Exam 4: Auditors Legal Liability67 Questions

Exam 5: Overview of the Audit Process49 Questions

Exam 6: Audit Evidence, Audit Objectives,71 Questions

Exam 7: Accepting the Engagement and56 Questions

Exam 8: Materiality Decisions and Performing Analytical Procedures47 Questions

Exam 9: Audit Risk, Including the Risk of Fraud44 Questions

Exam 10: Understanding Internal Controls91 Questions

Exam 11: Audit Procedures in Response to Assessed Risks: Tests of Controls18 Questions

Exam 12: Audit Procedures in Response to Assessed Risks: Substantive Tests82 Questions

Exam 13: Audit Sampling in Substantive Tests72 Questions

Exam 14: Auditing the Revenue Cycle72 Questions

Exam 15: Auditing the Expenditure Cycle80 Questions

Exam 16: Auditing the Production and81 Questions

Exam 17: Auditing the Investing and77 Questions

Exam 18: Auditing Investments and92 Questions

Exam 19: Completing the Audit and Postaudit102 Questions

Exam 20: Attest and Assurance Services, and Related Reports61 Questions

Exam 21: Internal, Operational, and103 Questions

Select questions type

A valid purchase requisition represents the authorization for the receiving department to accept goods delivered by vendors.

(True/False)

4.8/5  (35)

(35)

Discuss the confirmation of accounts payable in terms of:

1.requirements under GAAS;

2.accounts selected for confirmation; and

3.the difference in the form for accounts payable versus accounts receivable confirmations.

(Essay)

4.8/5 (37)

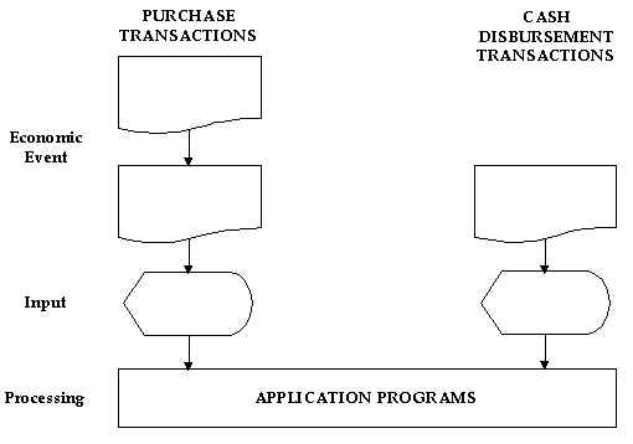

Shown below is a partial flowchart of the overview of a computerized system for purchases transactions and cash disbursements in the expenditure cycle.

REQUIRED: Label the symbols in the partial flowchart.

REQUIRED: Label the symbols in the partial flowchart.

(Essay)

4.7/5 (40)

The employee most likely to be involved in a "kickback" scheme is the:

(Multiple Choice)

4.8/5 (43)

Consider the following procedures for the verification of accounts payable.For each of the following independent exceptions, indicate the most likely and efficient audit procedure that would have detected the error.

Correct Answer: Verified

Verified

Premises:

Responses:

(Matching)

4.8/5 (46)

Examining subsequent payments consists of examining the documentation for checks issued or vouchers paid before the balance sheet date.

(True/False)

4.8/5 (39)

Central Meat Inc. buys and processes livestock for sales to supermarkets. In connection with your examination of the company's financial statements, you accumulate the following information about purchases and cash disbursements transactions in the expenditure cycle.

1.Each livestock buyer submits a daily report of purchases to the plant superintendent. This report shows the dates of purchase and expected delivery, the vendor and the number, weights, and type of livestock purchased. As shipments are received, any available plant employee counts the number of each type received and places a check mark beside this quantity on the buyer's report. When all shipments listed on the report have been received, the report is returned to the buyer.

2.Vendor's invoices, after a clerical check, are sent to the buyer for approval and returned to the accounting department. A disbursement voucher and a check for the approved amount are prepared in the accounting department. Checks are forwarded to the treasurer for signing. The treasurer's office sends signed checks directly to the buyer for delivery to the vendor.

REQUIRED: For each of the numbered notes identify three specific weaknesses. Give your recommended improvement for each weakness. Use a tabular format for your answer with columns for weaknesses and recommended improvements.

(Essay)

4.9/5 (38)

Cost of Goods Sold divided by Accounts Receivable is the formula for:

(Multiple Choice)

4.9/5 (46)

The specific audit objective that all purchase transactions and cash disbursements are valued using GAAP and correctly journalized, summarized, and posted relates to:

(Multiple Choice)

4.9/5 (37)

The specific audit objective that the entity is liable for the payables resulting from the recorded purchase transactions relates to:

(Multiple Choice)

4.9/5 (40)

Unlike accounts receivable, in accounts payable it is not necessary to segregate transaction duties.

(True/False)

4.8/5 (41)

To reduce the risk of theft or alternations, the department controlling the production of checks should control the mailing of the checks.

(True/False)

4.8/5 (36)

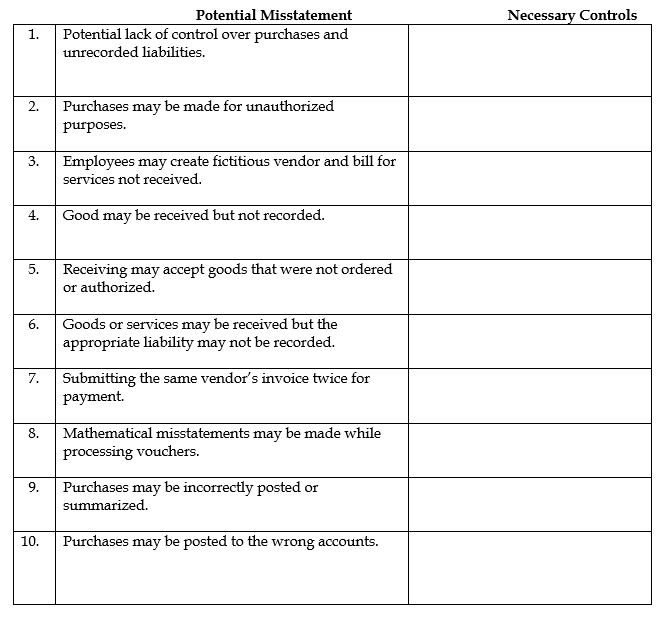

For each of the following potential expenditure cycle misstatements below, indicate the necessary control, which would most likely prevent or detect the misstatement.

(Essay)

4.7/5 (47)

Upon receipt of an invoice from a vendor, it is common for personnel in the accounts receivable department to enter the transaction data via terminals.

(True/False)

4.8/5 (39)

Consider the following procedures for the verification of accounts payable:

-Goods in transit shipped FOB-shipping point were not recorded as purchases in the current period.

_____

(Multiple Choice)

4.8/5 (35)

Consider the following procedures for the verification of accounts payable:

-Numerous debit balances exist in vendor accounts from multiple payments on

invoices.

_____

(Multiple Choice)

4.8/5 (45)

Consider the following procedures for the verification of accounts payable:

-Goods are sometimes ordered by purchasing agents on their own initiative to fill secret agreements with certain vendors.

_____

(Multiple Choice)

4.9/5 (33)

Goods shipped FOB shipping point should remain in the inventory of the seller and be excluded from the buyer's inventory and accounts payable until arrival at the buyer's receiving department.

(True/False)

4.8/5 (46)

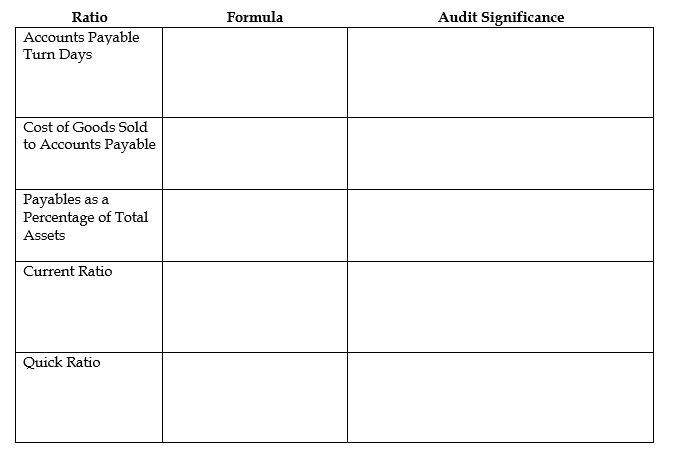

For each one of the following financial ratios, indicate the formula and identify the audit significance.

(Essay)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)