Exam 1: An Introduction to Fixed Income Markets

Exam 1: An Introduction to Fixed Income Markets17 Questions

Exam 2: Basics of Fixed Income Securities20 Questions

Exam 3: Basics of Interest Rate Risk Management17 Questions

Exam 4: Basic Refinements in Interest Rate Risk Management18 Questions

Exam 5: Interest Rate Derivatives: Forwards and Swaps15 Questions

Exam 6: Interest Rate Derivatives: Futures and Options15 Questions

Exam 7: Inflation, Monetary Policy, and the Federal Funds Rate15 Questions

Exam 8: Basics of Residential Mortgage Backed Securities21 Questions

Exam 9: One Step Binomial Trees15 Questions

Exam 10: Multi-Step Binomial Trees15 Questions

Exam 11: Risk Neutral Trees and Derivative Pricing18 Questions

Exam 12: American Options19 Questions

Exam 13: Monte Carlo Simulations on Trees18 Questions

Exam 14: Interest Rate Models in Continuous Time15 Questions

Exam 15: No Arbitrage and the Pricing of Interest Rate Securities17 Questions

Exam 16: Dynamic Hedging and Relative Value Trades13 Questions

Exam 17: Dynamic Hedging and Relative Value Trades18 Questions

Exam 18: The Risk and Return of Interest Rate Securities11 Questions

Exam 19: No Arbitrage Models and Standard Derivatives20 Questions

Exam 20: The Market Model for Standard Derivatives19 Questions

Exam 21: Forward Risk Neutral Pricing and the Libor Market Model14 Questions

Exam 22: Multifactor Models16 Questions

Select questions type

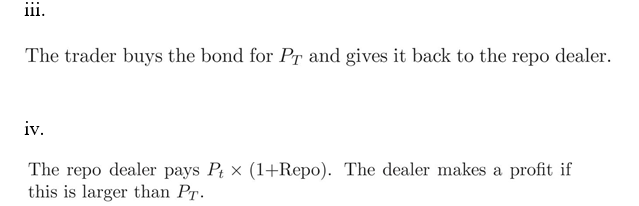

What are the steps to take a short position on a given U.S. security via the repo market?

Free

(Essay)

4.8/5  (43)

(43)

Correct Answer: Verified

Verified

The trader must take the following steps (reverse repo):

At time t:

3

i. Borrows the bond from the repo dealer and sells it at Pt.

ii. Receives Pt which he posts as collateral with the repo dealer.

At time T:

Is the following an arbitrage opportunity? A free car that if I repair well, I won't have to spend money on gasoline or maintenance costs (i.e. repairs) ever.

Free

(Essay)

4.9/5 (44)

Correct Answer:Verified

This is not an arbitrage opportunity, since I have to pay money (to repair the car) in order to be free of future costs.

Is the following an arbitrage opportunity? A bond that cost nothing but will payoff zero with certainty in the future.

Free

(Essay)

4.9/5 (41)

Correct Answer:Verified

This is not an arbitrage opportunity, since it doesn't give a positive payoff in the future.

Is the following an arbitrage opportunity? Suppose you are in the desert and are given a bag of ice with a penny inside. Assume that the ice will melt instantly and the cost of disposing of the bag is zero.

(Essay)

4.9/5 (33)

You are told that there is an ample supply for the bond mentioned in question 13. Does this affect your previous answer?

(Essay)

4.7/5 (48)

What are the steps to take a long position on a given U.S. security via the repo market?

(Essay)

4.9/5 (35)

What steps would you follow in order to take advantage of the following arbitrage opportunity (if there is one)? Security A costs $100 and pays $120 in 3 years. Security B costs $100 and pays $110 in one year. Your friend tells you that he would like you to lend him $110 in a year and that he would give $130 the following year. Finally you know that in two years, with $130, you can invest in a security that will pay you either $140 or $121 (with equal probability) after a year. 2

(Essay)

4.7/5 (42)

You find a bond that has a repo rate substantially lower than the GCR. Is this, for certain, an arbitrage opportunity?

(Essay)

4.9/5 (37)

Intuitively, is the Federal Funds rate generally higher, lower or the same as LIBOR? Why?

(Essay)

4.9/5 (38)

What steps would you follow in order to take advantage of the following arbitrage opportunity (if there is one)? Security A costs $3 and pays $5 in 2 years, while security B costs $3 and pays $4 in 2 years.

(Essay)

4.9/5 (39)

Intuitively, is LIBOR generally higher, lower or the same as the repo rate? Why?

(Essay)

5.0/5 (40)

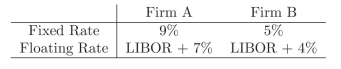

What are the gains from trade of entering into a swap for these two ?rms?

(Short Answer)

4.7/5 (36)

Is the following an arbitrage opportunity? A security that cost zero and might pay a dollar in the future, but pays zero otherwise.

(Essay)

4.9/5 (34)

What are the gains from trade of entering into a swap for these two ?rms?

(Short Answer)

4.9/5 (38)

Is the following an arbitrage opportunity? A gift that makes me feel good just by having it.

(Essay)

4.8/5 (38)

What are the gains from trade of entering into a swap for these two ?rms?

(Essay)

4.9/5 (41)

What steps would you follow in order to take advantage of the following arbitrage opportunity (if there is one)? Security A costs $100 and pays $110 in 2 years. Security B costs $100 and pays $109 in one year. You know that in a year with $109 you can invest in a security that pays $120 or $109 (with equal probability) the following year.

(Short Answer)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)