Exam 6: Interest Rate Derivatives: Futures and Options

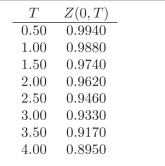

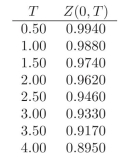

You are given the following discount factors:  You are told that the price of a European Call option on a 2-year ?xed rate bond paying 5% semiannually, with T =2andK = 101 is 4.6155. While the price of a European Put option with the exact same speci?cation is: 3.0500. Are the securities adequately priced?

You are told that the price of a European Call option on a 2-year ?xed rate bond paying 5% semiannually, with T =2andK = 101 is 4.6155. While the price of a European Put option with the exact same speci?cation is: 3.0500. Are the securities adequately priced?

Yes, according to the Put-Call parity the price of the Call option should be 4.6155.

What is an American Call option?

Given an underlying variable F (t), maturity T and strike price K;an American Call option is a contract between two counterparties, option buyer and option seller, according to which:

i. At any time before maturity T the option buyer has the right to ask the option seller for the payment of the following e?ective payo?: Payo? = (max(F (t) ? K, 0)

ii. The option seller has the obligation to pay this amount to the option buyer at T.

iii. In return for this right to obtain this payment (exercise) at T,the option buyer pays an option premium to the option seller at time 0.

What is a margin call?

When someone enters a futures contract, they must put up a specific amount with the exchange in order to meet the possible losses accrued from the contract. If this account declines below a specific amount, called maintenance margin, the exchange issues a margin call and the trader must replenish the account to the initial margin.

Under what conditions are futures and forwards the same? Is this realistic?

What are the shortcomings of futures, when compared to forward con- tracts?

What are the advantages of futures contracts, when compared to forward contracts?

You are given the following discount factors:  You are told that the price of a European Call option on a 6-month zero coupon bond, with T =0.5andK =99.35 is 0.13. While the price of a European Put option with the exact same specification is: 0.11. Are the securities adequately priced?

You are told that the price of a European Call option on a 6-month zero coupon bond, with T =0.5andK =99.35 is 0.13. While the price of a European Put option with the exact same specification is: 0.11. Are the securities adequately priced?

What are the main di?erences between a forward contract and a futures contract?

What is the difference between a European option and an American op- tion?

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)