Exam 10: Multi-Step Binomial Trees

Exam 1: An Introduction to Fixed Income Markets17 Questions

Exam 2: Basics of Fixed Income Securities20 Questions

Exam 3: Basics of Interest Rate Risk Management17 Questions

Exam 4: Basic Refinements in Interest Rate Risk Management18 Questions

Exam 5: Interest Rate Derivatives: Forwards and Swaps15 Questions

Exam 6: Interest Rate Derivatives: Futures and Options15 Questions

Exam 7: Inflation, Monetary Policy, and the Federal Funds Rate15 Questions

Exam 8: Basics of Residential Mortgage Backed Securities21 Questions

Exam 9: One Step Binomial Trees15 Questions

Exam 10: Multi-Step Binomial Trees15 Questions

Exam 11: Risk Neutral Trees and Derivative Pricing18 Questions

Exam 12: American Options19 Questions

Exam 13: Monte Carlo Simulations on Trees18 Questions

Exam 14: Interest Rate Models in Continuous Time15 Questions

Exam 15: No Arbitrage and the Pricing of Interest Rate Securities17 Questions

Exam 16: Dynamic Hedging and Relative Value Trades13 Questions

Exam 17: Dynamic Hedging and Relative Value Trades18 Questions

Exam 18: The Risk and Return of Interest Rate Securities11 Questions

Exam 19: No Arbitrage Models and Standard Derivatives20 Questions

Exam 20: The Market Model for Standard Derivatives19 Questions

Exam 21: Forward Risk Neutral Pricing and the Libor Market Model14 Questions

Exam 22: Multifactor Models16 Questions

Select questions type

Compute the spot rate duration for a straddle on a 1.5 year zero coupon bond with K = 98.00, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

Free

(Short Answer)

4.8/5  (45)

(45)

Correct Answer: Verified

Verified

Spot rate duration is -6.7695.

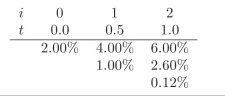

You are given the following interest rate tree. Use it when required in the

exercises.  -Using risk neutral pricing obtain the value for a put option on a 1.5 year zero coupon bond with K = 97.40, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

-Using risk neutral pricing obtain the value for a put option on a 1.5 year zero coupon bond with K = 97.40, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

Free

(Short Answer)

4.9/5 (39)

Correct Answer:Verified

The price is 0.1709.

What is one major drawback from using empirical estimates to fit the "true" interest rate tree?

Free

(Essay)

4.9/5 (34)

Correct Answer:Verified

One major drawback is that it may generate negative nominal interest rates.

Compute the spot rate duration for a put option on a 1.5 year zero coupon bond with K = 97.40, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

(Short Answer)

4.8/5 (45)

You are given the following interest rate tree. Use it when required in the

exercises.

-Using risk neutral pricing obtain the value for a 1.5 year zero coupon bond. Assume that p? = 0.7038 is constant over time.

(Short Answer)

4.8/5 (28)

How realistic is it to speak about negative interest rate in nominal terms?

(Essay)

4.8/5 (38)

You are given the following interest rate tree. Use it when required in the

exercises.

-Using risk neutral pricing obtain the value for a call option on a 1.5 year zero coupon bond with K = 99.00, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

(Short Answer)

4.9/5 (38)

In order to compute the spot rate duration do you use risk neutral prob- abilities or risk natural probabilities?

(Essay)

4.9/5 (40)

Which of the following prices should be higher: a call option, a put option or a straddle. All of them have the same maturity, underlying security and strike price. Explain.

(Essay)

4.7/5 (33)

What is the difference between risk neutral probability and risk natural probability?

(Essay)

4.9/5 (34)

Why do we say that the dynamic replication strategy is self-financing?

(Essay)

4.7/5 (38)

Using risk neutral pricing obtain the value for a straddle on a 1.5 year zero coupon bond with K = 98.00, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

(Short Answer)

4.8/5 (35)

Compute the spot rate duration for a call option on a 1.5 year zero coupon bond with K = 99.00, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

(Short Answer)

4.8/5 (33)

How realistic is it to speak about negative interest rate in real terms?

(Essay)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)