Exam 12: State and Local Taxes

Exam 1: Business Income, Deductions, and Accounting Methods99 Questions

Exam 2: Property Acquisition and Cost Recovery109 Questions

Exam 3: Property Dispositions110 Questions

Exam 4: Entities Overview80 Questions

Exam 5: Corporate Operations109 Questions

Exam 6: Accounting for Income Taxes100 Questions

Exam 7: Corporate Taxation: Nonliquidating Distributions100 Questions

Exam 8: Corporate Formation, Reorganization, and Liquidation100 Questions

Exam 9: Forming and Operating Partnerships106 Questions

Exam 10: Dispositions of Partnership Interests and Partnership Distributions100 Questions

Exam 11: S Corporations134 Questions

Exam 12: State and Local Taxes117 Questions

Exam 13: The U.S. Taxation of Multinational Transactions89 Questions

Exam 14: Transfer Taxes and Wealth Planning123 Questions

Select questions type

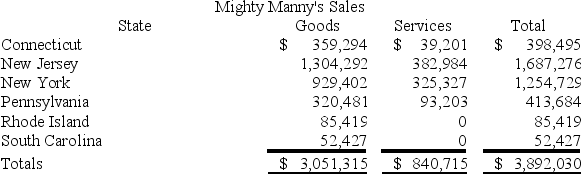

Mighty Manny, Incorporated manufactures and services deli machinery and distributes them across the United States. Mighty Manny is incorporated and headquartered in New Jersey. It has sales tax nexus in Connecticut, New Jersey, New York, Pennsylvania, Rhode Island, and South Carolina. Mighty Manny has sales as follows:

Assume the following sales tax rates: Connecticut (6.75 percent), New Jersey (7.5 percent), New York (8.5 percent), Pennsylvania (6.5 percent), Rhode Island (7.25 percent), and South Carolina (5.5 percent). Assume that Connecticut also taxes Mighty Manny's services. What is Mighty Manny's total sales and use tax liability?

Assume the following sales tax rates: Connecticut (6.75 percent), New Jersey (7.5 percent), New York (8.5 percent), Pennsylvania (6.5 percent), Rhode Island (7.25 percent), and South Carolina (5.5 percent). Assume that Connecticut also taxes Mighty Manny's services. What is Mighty Manny's total sales and use tax liability?

(Essay)

4.9/5  (35)

(35)

Gordon operates the Tennis Pro Shop in Blacksburg, Virginia. The Shop sells, manufacturers, and customizes tennis racquets for serious amateurs. Virginia has a 5 percent sales tax. Assume that a District of Columbia customer picks up a $2,000 racquet order in the Blacksburg store and drives it back to the District of Columbia (where the sales tax rate is 8.5 percent). Determine the sales and use tax liability (assume the Shop has no sales personnel or property in District of Columbia) of the customer?

(Essay)

4.9/5 (28)

Most services are sourced to the state where the services were performed.

(True/False)

4.8/5 (36)

Which of the following activities will create sales tax nexus?

(Multiple Choice)

4.7/5 (35)

The payroll factor includes payments to independent contractors.

(True/False)

4.9/5 (37)

The throwback rule requires a company, for apportionment purposes, to include all sales of inventory sold into a state without income tax nexus rather than from the state from where the inventory was shipped.

(True/False)

4.7/5 (37)

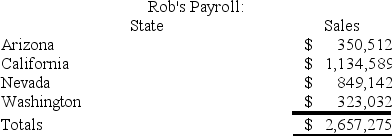

Handsome Rob provides transportation services in several western states. Rob has sales as follows:  Rob is a California Corporation and has the following facts:

Rob has income tax nexus in Arizona, California, Nevada, and Washington. The Washington drivers spend 25 percent of their time driving through Oregon. California payroll includes $200,000 of payroll for services provided in Nevada by California based drivers. What is Rob's California sale numerator?

Rob is a California Corporation and has the following facts:

Rob has income tax nexus in Arizona, California, Nevada, and Washington. The Washington drivers spend 25 percent of their time driving through Oregon. California payroll includes $200,000 of payroll for services provided in Nevada by California based drivers. What is Rob's California sale numerator?

(Multiple Choice)

4.9/5 (35)

Sales personnel investigating a potential customer's credit worthiness generally are deemed to exceed protected boundaries of solicitation.

(True/False)

4.9/5 (45)

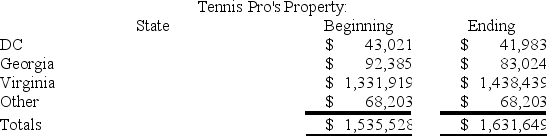

Gordon operates the Tennis Pro Shop in Blacksburg, Virginia. Tennis Pro has property as follows:

Tennis Pro also rents Virginia property at an annual rent of $24,000. What is Tennis Pro's Virginia property numerator and property factor?

Tennis Pro also rents Virginia property at an annual rent of $24,000. What is Tennis Pro's Virginia property numerator and property factor?

(Essay)

5.0/5 (37)

Roxy operates a dress shop in Arlington, Virginia. Roxy also ships dresses nationwide upon request. Roxy's Virginia sales are $1,000,000 and out of state sales are $200,000. Assuming that Virginia's sales tax rate is 5 percent, what is Roxy's Virginia sales and use tax liability?

(Multiple Choice)

4.7/5 (37)

Public Law 86-272 protects solicitation from income taxation. Which of the following activities exceeds the solicitation threshold?

(Multiple Choice)

4.8/5 (39)

Purchases of inventory for resale are typically exempt from sales and use taxes.

(True/False)

4.8/5 (33)

Roxy operates a dress shop in Arlington, Virginia. Lisa, a Maryland resident, comes in for a measurement and purchases a $1,500 dress. Lisa returns to Virginia a few weeks later to pick up the dress and drive it back to her Maryland residence where she will use the property. Assuming that Virginia's sales tax rate is 5 percent and that Maryland's sales tax rate is 6 percent, what is Roxy's sales tax liability?

(Multiple Choice)

4.7/5 (40)

Bethesda Corporation is unprotected from income tax by Public Law 86-272. Which of the following characteristics creates a problem for Bethesda in states other than Maryland?

(Multiple Choice)

4.7/5 (40)

All of the following are False regarding apportionment except?

(Multiple Choice)

4.9/5 (36)

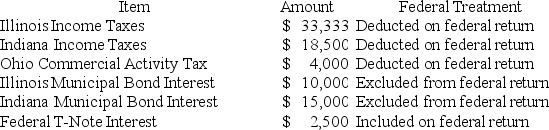

PWD Incorporated is an Illinois corporation. It properly included, deducted, or excluded the following items on its federal tax return in the current year:  PWD's Federal Taxable Income was $100,000. Calculate PWD's Illinois state tax base.

PWD's Federal Taxable Income was $100,000. Calculate PWD's Illinois state tax base.

(Multiple Choice)

4.7/5 (45)

Tennis Pro is headquartered in Virginia. Assume it has a Kentucky state income tax base of $220,000. Of this amount, $40,000 was non-business income. Assume that Tennis Pro's Kentucky sales, payroll and property apportionment factor are 12, 5, and 3 percent, respectively. Assume that Kentucky uses a single-factor sales formula apportionment method. The non-business income allocated to Kentucky was $1,000. Assuming Kentucky's corporate tax rate of 6 percent, what is Tennis Pro's Kentucky state tax liability?

(Essay)

4.8/5 (43)

Tennis Pro has the following sales, payroll and property factors:

What would Tennis Pro's Virginia and Maryland apportionment factors be if Virginia used a double-weighted sales four factor method and Maryland used a single-factor sales formula?

What would Tennis Pro's Virginia and Maryland apportionment factors be if Virginia used a double-weighted sales four factor method and Maryland used a single-factor sales formula?

(Essay)

4.9/5 (42)

Use tax liability accrues in the state where purchased property will be used when the seller of the property is not required to collect sales tax.

(True/False)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)