Exam 15: Monopolistic Competition and Product Differentiation

Exam 1: First Principles246 Questions

Exam 2: Economic Models: Trade-Offs and Trade72 Questions

Exam 3: Supply and Demand266 Questions

Exam 4: Consumer and Producer Surplus196 Questions

Exam 5: Price Controls and Quotas: Meddling With Markets203 Questions

Exam 6: Elasticity329 Questions

Exam 7: Taxes284 Questions

Exam 8: International Trade265 Questions

Exam 9: Decision Making by Individuals and Firms209 Questions

Exam 10: The Rational Consumer477 Questions

Exam 11: Behind the Supply Curve: Inputs and Costs282 Questions

Exam 12: Perfect Competition and the Supply Curve320 Questions

Exam 13: Monopoly258 Questions

Exam 14: Oligopoly212 Questions

Exam 15: Monopolistic Competition and Product Differentiation223 Questions

Exam 16: Externalities234 Questions

Exam 17: Public Goods and Common Resources237 Questions

Exam 18: The Economics of the Welfare State144 Questions

Exam 19: Factor Markets and the Distribution of Income241 Questions

Exam 20: Uncertainty, Risk, and Private Information199 Questions

Select questions type

A monopolistically competitive firm is operating in the short run at the optimal level of output and earns negative economic profits.Describe how this industry will adjust in the long run.

(Essay)

4.7/5  (25)

(25)

Industries that are made up of many competing producers, each selling a differentiated product, and whose firms eventually earn zero economic profits in the long run are:

(Multiple Choice)

4.8/5 (35)

The demand curve for a firm under monopolistic competition is:

(Multiple Choice)

4.8/5 (36)

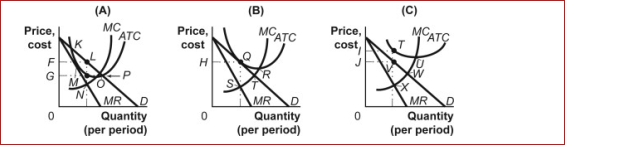

Figure: Profit Maximization in Monopolistic Competition

(Figure: Profit Maximization in Monopolistic Competition) Look at the figure Profit Maximization in Monopolistic Competition.In monopolistic competition, long-run equilibrium is characterized by:

(Figure: Profit Maximization in Monopolistic Competition) Look at the figure Profit Maximization in Monopolistic Competition.In monopolistic competition, long-run equilibrium is characterized by:

(Multiple Choice)

4.8/5 (41)

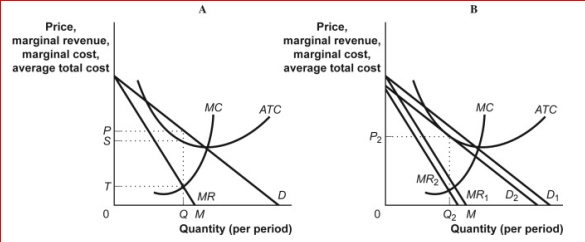

Figure: Profits in Monopolistic Competition

(Figure: Profits in Monopolistic Competition) In panel B of the figure Profits in Monopolistic Competition, the profit-maximizing quantity of output is determined by the intersection at point:

(Figure: Profits in Monopolistic Competition) In panel B of the figure Profits in Monopolistic Competition, the profit-maximizing quantity of output is determined by the intersection at point:

(Multiple Choice)

4.8/5 (33)

An industry with a large number of small firms producing a standardized product in a market with easy entry and exit of firms is:

(Multiple Choice)

4.9/5 (45)

Figure: Profit Maximization in Monopolistic Competition

(Figure: Profit Maximization in Monopolistic Competition) In panel B of the figure Profit Maximization in Monopolistic Competition, the profit-maximizing price is P₂ and the ATC curve is tangent to the new demand curve.The portion of the ATC that lies to the right of the tangency and continues down to the intersection of MC with ATC indicates:

(Multiple Choice)

4.9/5 (39)

The demand curve for a firm operating in a monopolistically competitive market is best described as:

(Multiple Choice)

4.8/5 (38)

General Snacks is a typical firm in a market characterized by the model of monopolistic competition.Initially, the market is in long-run equilibrium, and then there is an increase in demand for snacks.In the short run the price of snacks will and the output of services will _.

(Multiple Choice)

4.8/5 (42)

Monopolistic competition is a market structure that shares some characteristics with perfect competition and monopoly.Explain where these market structures are similar and where they differ.

(Essay)

4.8/5 (42)

Suppose a monopolistically competitive firm is in long-run equilibrium.Then:

(Multiple Choice)

4.9/5 (39)

(Figure: Monopolistic Competition III) The figure Monopolistic Competition III shows the demand, marginal revenue, marginal cost, and average total cost curves for Pat's Pizza Parlor, a monopolistic competitor in the food-to-go industry.The optimal level of output for Pat's Pizza Parlor is ________ and the profit-maximizing price is _.

(Multiple Choice)

4.9/5 (34)

A monopolistically competitive firm may have positive or negative profits in the short run but will have zero profits in the long run.False

(True/False)

4.7/5 (38)

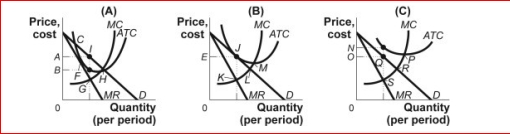

Figure: Firms in Monopolistic Competition  (Figure: Firms in Monopolistic Competition) Look at the figure Firms in Monopolistic Competition.There will be a negative economic profit (or an economic loss) earned at the profit-maximizing price ________ in panel _.

(Figure: Firms in Monopolistic Competition) Look at the figure Firms in Monopolistic Competition.There will be a negative economic profit (or an economic loss) earned at the profit-maximizing price ________ in panel _.

(Multiple Choice)

4.9/5 (25)

When Henry Ford produced his cars, he ________, while GM produced its cars _.

(Multiple Choice)

5.0/5 (39)

The model of monopolistic competition can characterize the market for plumbing services in a city.This market is initially in long-run equilibrium, but then there is an increase in demand for plumbing services.We expect that in the long run:

(Multiple Choice)

4.7/5 (38)

Figure: The Market for Gas Stations

(Figure: The Market for Gas Stations) Look at the figure The Market for Gas Stations.Assume that the market for gas stations is characterized by many firms, differentiated products, easy entry, and easy exit.For the typical gas station the profit-maximizing price would be:

(Multiple Choice)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)