Exam 11: Behind the Supply Curve: Inputs and Costs

Exam 1: First Principles233 Questions

Exam 2: Economic Models: Trade-Offs and Trade 25382 Questions

Exam 3: Supply and Demand290 Questions

Exam 4: Consumer and Producer Surplus224 Questions

Exam 5: Price Controls and Quotas: Meddling With Markets227 Questions

Exam 6: Elasticity300 Questions

Exam 7: Taxes298 Questions

Exam 8: International Trade272 Questions

Exam 9: Decision Making by Individuals Firms201 Questions

Exam 10: The Rational Consumer372 Questions

Exam 11: Behind the Supply Curve: Inputs and Costs362 Questions

Exam 12: Perfect Competition and the Supply Curve355 Questions

Exam 13: Monopoly350 Questions

Exam 14: Oligopoly294 Questions

Exam 15: Monopolistic Competition and Product Differentiation262 Questions

Exam 16: Externalities199 Questions

Exam 17: Public Goods Common Resources224 Questions

Exam 18: The Economics of the Welfare140 Questions

Exam 19: Factor Markets and the Distribution of Income369 Questions

Exam 20: Uncertainty, Risk, and Private Information202 Questions

Select questions type

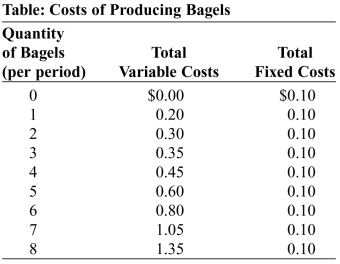

Use the following to answer questions:  -(Table: Costs of Producing Bagels) Look at the table Cost of Producing Bagels. Average total cost reaches its minimum value for the _____ bagel.

-(Table: Costs of Producing Bagels) Look at the table Cost of Producing Bagels. Average total cost reaches its minimum value for the _____ bagel.

(Multiple Choice)

4.9/5  (31)

(31)

The average total cost of producing cell phones in a factory is $20 at the current output level of 100 units per week. If fixed cost is $1,200 per week:

(Multiple Choice)

4.9/5 (35)

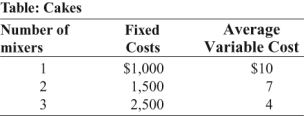

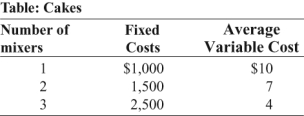

Use the following to answer questions:  -(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special birthday cakes. She is trying to decide how many mixers to purchase. Her estimated fixed and average variable costs if she purchases one, two, or three mixers are shown in the table. Assume that average variable costs do not vary with the quantity of output. If Pat purchases one mixer and bakes 100 cakes per day, what is her average fixed cost?

-(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special birthday cakes. She is trying to decide how many mixers to purchase. Her estimated fixed and average variable costs if she purchases one, two, or three mixers are shown in the table. Assume that average variable costs do not vary with the quantity of output. If Pat purchases one mixer and bakes 100 cakes per day, what is her average fixed cost?

(Multiple Choice)

4.9/5 (35)

The eventual increase in AVC as output increases is the _____ effect.

(Multiple Choice)

4.9/5 (36)

If output increases, a firm will move along its short-run average total cost curve in the short run until it has time to adjust its fixed cost.

(True/False)

4.8/5 (28)

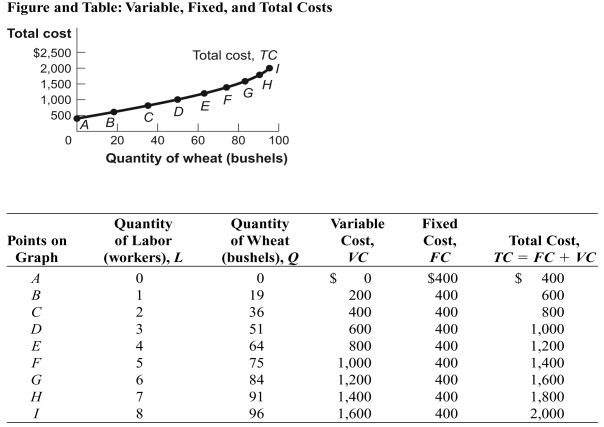

Use the following to answer questions:  -(Figure and Table: Variable, Fixed, and Total Costs) Look at the figure and table Variable, Fixed, and Total Costs. The marginal cost of increasing production from 51 to 64 bushels of wheat is:

-(Figure and Table: Variable, Fixed, and Total Costs) Look at the figure and table Variable, Fixed, and Total Costs. The marginal cost of increasing production from 51 to 64 bushels of wheat is:

(Multiple Choice)

4.9/5 (31)

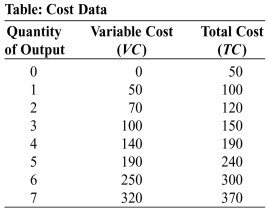

Use the following to answer questions:  -(Table: Cost Data) Look at the table Cost Data. The marginal cost of producing the fourth purse is:

-(Table: Cost Data) Look at the table Cost Data. The marginal cost of producing the fourth purse is:

(Multiple Choice)

4.8/5 (29)

Use the following to answer questions:

-(Table: Cost Data) Look at the table Cost Data. The average fixed cost of producing 5 purses is:

(Multiple Choice)

4.8/5 (36)

A cost that does not depend on the quantity of output produced is:

(Multiple Choice)

4.8/5 (33)

For most restaurants, the average total cost curve _____ at _____ levels of output, then _____ at _____ levels.

(Multiple Choice)

4.8/5 (42)

When an increase in the firm's output reduces its long-run average total cost, it has _____ returns to scale.

(Multiple Choice)

4.7/5 (39)

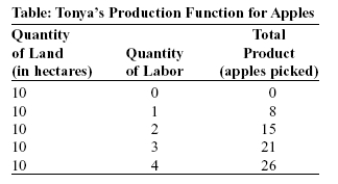

Use the following to answer questions:  -(Table: Tonya's Production Function for Apples) Look at the table Tonya's Production Function for Apples. Tonya's variable:

-(Table: Tonya's Production Function for Apples) Look at the table Tonya's Production Function for Apples. Tonya's variable:

(Multiple Choice)

4.9/5 (37)

Use the following to answer questions:

-(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special birthday cakes. She is trying to decide how many mixers to purchase. Her estimated fixed and average variable costs if she purchases one, two, or three mixers are shown in the table. Assume that average variable costs do not vary with the quantity of output. If Pat purchases three mixers and bakes 400 cakes per day, what is her average fixed cost?

(Multiple Choice)

4.8/5 (34)

Use the following to answer questions:

-(Table: Cost Data) Look at the table Cost Data. When the purse factory produces 5 units of output (purses):

(Multiple Choice)

4.8/5 (31)

When all of a firm's inputs are doubled, input prices do not change, and this results in the firm's level of production more than doubling, a firm is operating:

(Multiple Choice)

5.0/5 (39)

Use the following to answer questions:  -(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special birthday cakes. Her estimated fixed and average variable costs if she purchases one, two, or three mixers are shown in the table. Assume that average variable costs do not vary with the quantity of output. Suppose that Pat used to produce 100 cakes, but she has a sudden increase in demand, so that she begins to produce 200 cakes. Explain how her average total cost will change in the short run and in the long run.

-(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special birthday cakes. Her estimated fixed and average variable costs if she purchases one, two, or three mixers are shown in the table. Assume that average variable costs do not vary with the quantity of output. Suppose that Pat used to produce 100 cakes, but she has a sudden increase in demand, so that she begins to produce 200 cakes. Explain how her average total cost will change in the short run and in the long run.

(Essay)

4.8/5 (32)

Use the following to answer questions:

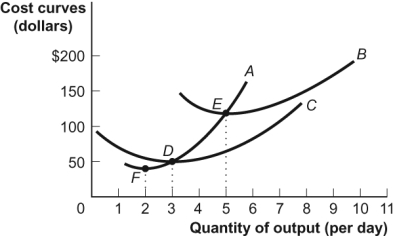

Figure: Short-Run Costs  -(Figure: Short-Run Costs) Look at the figure Short-Run Costs. C is the _____ cost curve.

-(Figure: Short-Run Costs) Look at the figure Short-Run Costs. C is the _____ cost curve.

(Multiple Choice)

4.9/5 (28)

Suppose the marginal cost curve in the short run first decreases and then increases. If marginal cost is decreasing, _____ must be _____ and _____ must be _____.

(Multiple Choice)

4.7/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)