Exam 11: Behind the Supply Curve: Inputs and Costs

Exam 1: First Principles233 Questions

Exam 2: Economic Models: Trade-Offs and Trade 25382 Questions

Exam 3: Supply and Demand290 Questions

Exam 4: Consumer and Producer Surplus224 Questions

Exam 5: Price Controls and Quotas: Meddling With Markets227 Questions

Exam 6: Elasticity300 Questions

Exam 7: Taxes298 Questions

Exam 8: International Trade272 Questions

Exam 9: Decision Making by Individuals Firms201 Questions

Exam 10: The Rational Consumer372 Questions

Exam 11: Behind the Supply Curve: Inputs and Costs362 Questions

Exam 12: Perfect Competition and the Supply Curve355 Questions

Exam 13: Monopoly350 Questions

Exam 14: Oligopoly294 Questions

Exam 15: Monopolistic Competition and Product Differentiation262 Questions

Exam 16: Externalities199 Questions

Exam 17: Public Goods Common Resources224 Questions

Exam 18: The Economics of the Welfare140 Questions

Exam 19: Factor Markets and the Distribution of Income369 Questions

Exam 20: Uncertainty, Risk, and Private Information202 Questions

Select questions type

Firms choose their level of fixed cost in the long run based on the amount of output that they expect to produce.

(True/False)

4.9/5  (42)

(42)

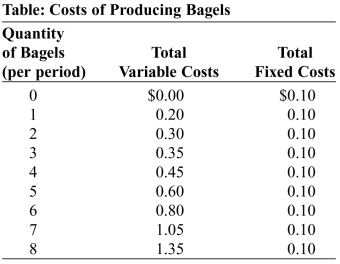

Use the following to answer questions:  -(Table: Costs of Producing Bagels) Look at the table Cost of Producing Bagels. Marginal cost reaches its minimum value for the _____ bagel.

-(Table: Costs of Producing Bagels) Look at the table Cost of Producing Bagels. Marginal cost reaches its minimum value for the _____ bagel.

(Multiple Choice)

5.0/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)