Exam 11: Risk and Return: the Capital Asset Pricing Model

Exam 1: Introduction to Corporate Finance38 Questions

Exam 2: Accounting Statements and Cash Flow59 Questions

Exam 3: Financial Planning and Growth39 Questions

Exam 4: Financial Markets and Net Present Value: First Principles of Finance36 Questions

Exam 5: The Time Value of Money73 Questions

Exam 6: How to Value Bonds and Stocks81 Questions

Exam 7: Net Present Value and Other Investment Rules57 Questions

Exam 8: Net Present Value and Capital Budgeting48 Questions

Exam 9: Risk Analysis, Real Options, and Capital Budgeting35 Questions

Exam 10: Risk and Return: Lessons From Market History51 Questions

Exam 11: Risk and Return: the Capital Asset Pricing Model65 Questions

Exam 12: An Alternative View of Risk and Return: the Arbitrage Pricing Theory42 Questions

Exam 13: Risk, Return, and Capital Budgeting63 Questions

Exam 14: Corporate Financing Decisions and Efficient Capital Markets46 Questions

Exam 15: Long-Term Financing: an Introduction46 Questions

Exam 16: Capital Structure: Basic Concepts56 Questions

Exam 17: Capital Structure: Limits to the Use of Debt53 Questions

Exam 18: Valuation and Capital Budgeting for the Levered Firm54 Questions

Exam 19: Dividends and Other Payouts47 Questions

Exam 20: Issuing Equity Securities to the Public43 Questions

Exam 21: Long-Term Debt50 Questions

Exam 22: Leasing42 Questions

Exam 23: Options and Corporate Finance: Basic Concepts63 Questions

Exam 24: Options and Corporate Finance: Extensions and Applications24 Questions

Exam 25: Warrants and Convertibles47 Questions

Exam 26: Derivatives and Hedging Risk50 Questions

Exam 27: Short-Term Finance and Planning51 Questions

Exam 28: Cash Management35 Questions

Exam 29: Credit Management31 Questions

Exam 30: Mergers and Acquisitions55 Questions

Exam 31: Financial Distress22 Questions

Exam 32: International Corporate Finance54 Questions

Select questions type

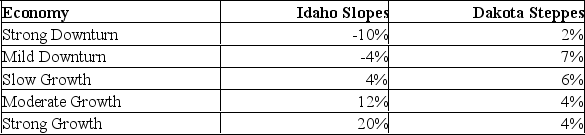

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  The variances of IS and DS are:

The variances of IS and DS are:

(Multiple Choice)

4.9/5  (31)

(31)

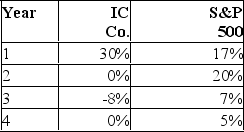

Returns for the IC Company and for the S&P 500 Index over the previous 4-year period are given below:

What are the average returns on IC and on the S&P 500 index? If you had invested $1.00 in IC, how much would you have had after 4 years? What is the correlation between the returns on IC and the S&P?

What are the average returns on IC and on the S&P 500 index? If you had invested $1.00 in IC, how much would you have had after 4 years? What is the correlation between the returns on IC and the S&P?

(Essay)

4.9/5 (37)

Given the following information on 3 stocks:

Using the CAPM, calculate the expected return for Stock's A, B, and

C. Which stocks would you recommend purchasing?

BA = .0070/.0064 = 1.094; ra = .07 + (.18-.07)1.094 = .1903

BB = .0045/.0064 = 0.703; rb = .07 + (.18-.07)0.703 = .1473

BC = .0013/.0064 = 0.203; rc = .07 + (.18-.07)0.203 = .0923

Indifferent on A as .1903 _.19.

Would buy B as.15 > .1473.

Would not buy C as.09 < .0923.

Using the CAPM, calculate the expected return for Stock's A, B, and

C. Which stocks would you recommend purchasing?

BA = .0070/.0064 = 1.094; ra = .07 + (.18-.07)1.094 = .1903

BB = .0045/.0064 = 0.703; rb = .07 + (.18-.07)0.703 = .1473

BC = .0013/.0064 = 0.203; rc = .07 + (.18-.07)0.203 = .0923

Indifferent on A as .1903 _.19.

Would buy B as.15 > .1473.

Would not buy C as.09 < .0923.

(Essay)

4.7/5 (40)

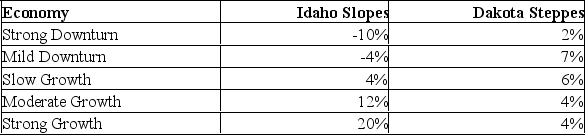

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  The means of IS and DS are:

The means of IS and DS are:

(Multiple Choice)

4.8/5 (37)

A portfolio contains four assets. Asset 1 has a beta of.8 and comprises 30% of the portfolio. Asset 2 has a beta of 1.1 and comprises 30% of the portfolio. Asset 3 has a beta of 1.5 and comprises 20% of the portfolio. Asset 4 has a beta of 1.6 and comprises the remaining 20% of the portfolio. If the riskless rate is expected to be 3% and the market risk premium is 6%, what is the beta of the portfolio, the expected return on the portfolio and the market?

(Multiple Choice)

4.8/5 (38)

The combination of the efficient set of portfolios with a riskless lending and borrowing rate results in:

(Multiple Choice)

4.9/5 (38)

Which one of the following would indicate a portfolio is being effectively diversified?

(Multiple Choice)

4.9/5 (30)

The diagram below represents an opportunity set for a two asset combination. Indicate the correct efficient set with labels; explain why it is so.

(Essay)

4.7/5 (42)

As we add more securities to a portfolio, the ____ will decrease:

(Multiple Choice)

4.8/5 (35)

A portfolio is made up of 75% of stock 1, and 25% of stock 2. Stock 1 has a variance of.08, and stock 2 has a variance of.035. The covariance between the stocks is -.001. Calculate both the variance and the standard deviation of the portfolio.

(Essay)

4.9/5 (43)

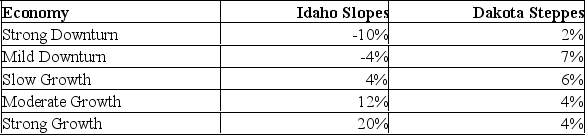

Idaho Slopes (IS) and Dakota Steppes (DS) are both seasonal businesses. IS is a downhill skiing facility, while DS is a tour company that specializes in walking tours and camping. The equally likely returns on each company over the next year is expected to be:  The covariance between the IS and DS returns is:

The covariance between the IS and DS returns is:

(Multiple Choice)

4.8/5 (35)

You have plotted the data for two securities over time on the same graph, ie., the month return of each security for the last 5 years. If the pattern of the movements of the two securities rose and fell as the other did, these two securities would have:

(Multiple Choice)

4.9/5 (27)

The standard deviation of a portfolio will tend to increase when:

(Multiple Choice)

4.9/5 (37)

When a security is added to a portfolio the appropriate return and risk contributions are:

(Multiple Choice)

4.9/5 (35)

Explain in words what beta is and why it is an important tool of security valuation.

(Essay)

4.8/5 (32)

Draw and explain the relationship between the opportunity set for a two asset portfolio when the correlation is: [Choose from -1, -.5, 0, +.5, and +1]

(Essay)

4.9/5 (42)

If the correlation between two stocks is +1, then a portfolio combining these two stocks will have a variance that is:

(Multiple Choice)

5.0/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)