Exam 9: Valuation and Analysis of Bonds With Embedded Options

Exam 1: Fixed-Income Securities: Defining Elements28 Questions

Exam 2: Fixed-Income Markets: Issuance, Trading, and Funding31 Questions

Exam 3: Introduction to Fixed-Income Valuation44 Questions

Exam 4: Introduction to Asset-Backed Securities42 Questions

Exam 5: Understanding Fixed Income Risk and Return27 Questions

Exam 6: Fundamentals of Credit Analysis45 Questions

Exam 7: The Term Structure and Interest Rate Dynamics56 Questions

Exam 8: The Arbitrage-Free Valuation Framework17 Questions

Exam 9: Valuation and Analysis of Bonds With Embedded Options36 Questions

Exam 10: Credit Analysis Models30 Questions

Exam 11: Credit Default Swaps15 Questions

Exam 12: Overview of Fixed-Income Portfolio Management12 Questions

Exam 13: Liability-Driven and Index-Based Strategies26 Questions

Exam 14: Yield Curve Strategies32 Questions

Exam 15: Fixed-Income Active Management: Credit Strategies15 Questions

Select questions type

The following information relates to Questions 11-19

Rayes investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm's bond port-folio. Rayes has asked Mingfang Hsu, one of the firm's analysts, to assist her in selecting and analyzing bonds for possible inclusion in the firm's bond portfolio.Hsu first selects two corporate bonds that are callable at par and have the same character-istics in terms of maturity, credit quality and call dates. Hsu uses the option-adjusted spread(oAS) approach to analyse the bonds, assuming an interest rate volatility of 10%. The resultsof his analysis are presented in Exhibit 1.

EXHIBIT 1 Summary Results of Hsu's Analysis Using the OAS Approach

Analysis Using the OAS Approach Bond OAS (in bps) Bond 1 25.5 Bond 2 30.3

Hsu then selects the four bonds issued by Rw, inc. given in Exhibit 2. These bonds all have a maturity of three years and the same credit rating. Bonds 4 and 5 are identical to Bond3, an option-free bond, except that they each include an embedded option.

EXHIBIT 2 Bonds Issued by RW, Inc. Bond Coupon Special Provision Bond 3 4.00\% annual Bond 4 4.00\% annual Callable at par at the end of years 1 and 2 Bond 5 4.00\% annual Putable at par at the end of years 1 and 2 Bond 6 One-year Libor annually, set in arrears

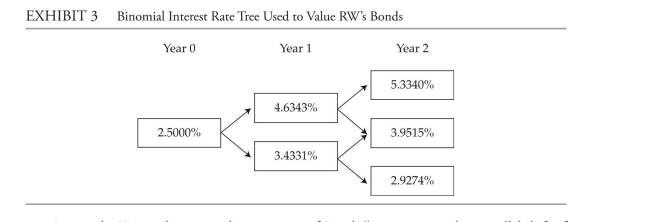

To value and analyze Rw's bonds, Hsu uses an estimated interest rate volatility of 15% and constructs the binomial interest rate tree provided in Exhibit 3.

Rayes asks Hsu to determine the sensitivity of Bond 4's price to a 20 bps parallel shift ofthe benchmark yield curve. The results of Hsu's calculations are shown in Exhibit 4.EXHiBiT 4 Summary Results of Hsu's Analysis about the Sensitivity of Bond 4's Price to a ParallelShift of the Benchmark yield Curve Magnitude of the Parallel Shift in the Benchmark yield Curve +20 bps −20 bps full Price of Bond 4 (% of par) 100.478 101.238 Hsu also selects the two floating-rate bonds issued by Varlep, plc given in Exhibit 5. These

bonds have a maturity of three years and the same credit rating.

EXHIBIT 5 Floating-Rate Bonds Issued by Varlep, plc Bond Coupon Bond 7 One-year Libor annually, set in arrears, capped at 5.00\% Bond 8 One-year Libor annually, set in arrears, floored at 3.50\%

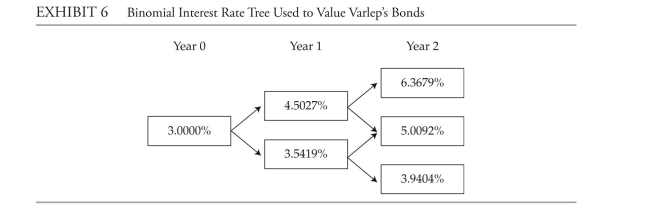

To value Varlep's bonds, Hsu constructs the binomial interest rate tree provided inExhibit 6.

Rayes asks Hsu to determine the sensitivity of Bond 4's price to a 20 bps parallel shift ofthe benchmark yield curve. The results of Hsu's calculations are shown in Exhibit 4.EXHiBiT 4 Summary Results of Hsu's Analysis about the Sensitivity of Bond 4's Price to a ParallelShift of the Benchmark yield Curve Magnitude of the Parallel Shift in the Benchmark yield Curve +20 bps −20 bps full Price of Bond 4 (% of par) 100.478 101.238 Hsu also selects the two floating-rate bonds issued by Varlep, plc given in Exhibit 5. These

bonds have a maturity of three years and the same credit rating.

EXHIBIT 5 Floating-Rate Bonds Issued by Varlep, plc Bond Coupon Bond 7 One-year Libor annually, set in arrears, capped at 5.00\% Bond 8 One-year Libor annually, set in arrears, floored at 3.50\%

To value Varlep's bonds, Hsu constructs the binomial interest rate tree provided inExhibit 6.

last, Hsu selects the two bonds issued by whorton, inc. given in Exhibit 7. These bonds are close to their maturity date and are identical, except that Bond 9 includes a conversion option. whorton's common stock is currently trading at $30 per share.

EXHІВАТ 7 Bonds Issued by Whorton, Inc. Bond Type of Bond Bond 9 Convertible bond with a conversion price of \ 50 Bond 10 Identical to Bond 9 except that it does not include a conversion option

-The value of Bond 7 is closest to:

last, Hsu selects the two bonds issued by whorton, inc. given in Exhibit 7. These bonds are close to their maturity date and are identical, except that Bond 9 includes a conversion option. whorton's common stock is currently trading at $30 per share.

EXHІВАТ 7 Bonds Issued by Whorton, Inc. Bond Type of Bond Bond 9 Convertible bond with a conversion price of \ 50 Bond 10 Identical to Bond 9 except that it does not include a conversion option

-The value of Bond 7 is closest to:

(Multiple Choice)

4.9/5  (34)

(34)

The following information relates to Questions 1-10

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. on 1 october 20X0, Steele ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, inc. The three bonds, whose characteristics are given in Exhibit 1, carry the highest credit rating.

EXHiBiT 1 fixed-Rate Bonds issued by Pro Star, inc.

Bond Maturity Coupon Type of Bond Bond 1 1 October 20X3 4.40\% annual Option-free Bond 2 1 October 20X3 4.40\% annual Callable at par on 1 October 20X1 and on 1 October 20X2 Bond 3 1 October 20X3 4.40\% annual Putable at par on 1 October 20X1 and on 1 October 20X2

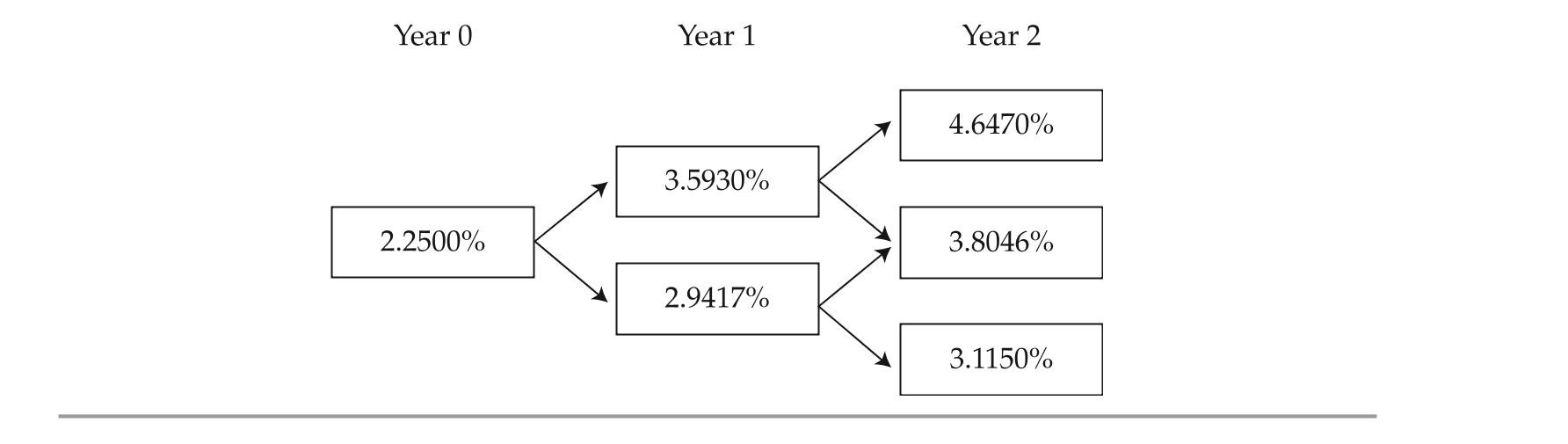

The one-year, two-year, and three-year par rates are 2.250%, 2.750%, and 3.100%, re-spectively. Based on an estimated interest rate volatility of 10%, ferguson constructs the bino-mial interest rate tree shown in Exhibit 2.

EXHiBiT 2 Binomial interest Rate Tree

on 19 october 20X0, ferguson analyzes the convertible bond issued by Pro Star given in Exhibit 3. That day, the option-free value of Pro Star's convertible bond is $1,060 and Pro Star's stock price is $37.50.

EXHiBiT 3 Convertible Bond issued by Pro Star, inc.

Issue Date: 6 December 20X0 Maturity Date: 6 December 20X4 Coupon Rate: 2\% Issue Price: \ 1,000 Conversion Ratio: 31

-A fall in interest rates would most likely result in:

on 19 october 20X0, ferguson analyzes the convertible bond issued by Pro Star given in Exhibit 3. That day, the option-free value of Pro Star's convertible bond is $1,060 and Pro Star's stock price is $37.50.

EXHiBiT 3 Convertible Bond issued by Pro Star, inc.

Issue Date: 6 December 20X0 Maturity Date: 6 December 20X4 Coupon Rate: 2\% Issue Price: \ 1,000 Conversion Ratio: 31

-A fall in interest rates would most likely result in:

(Multiple Choice)

4.8/5 (39)

The following information relates to Questions 11-19

Rayes investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm's bond port-folio. Rayes has asked Mingfang Hsu, one of the firm's analysts, to assist her in selecting and analyzing bonds for possible inclusion in the firm's bond portfolio.Hsu first selects two corporate bonds that are callable at par and have the same character-istics in terms of maturity, credit quality and call dates. Hsu uses the option-adjusted spread(oAS) approach to analyse the bonds, assuming an interest rate volatility of 10%. The resultsof his analysis are presented in Exhibit 1.

EXHIBIT 1 Summary Results of Hsu's Analysis Using the OAS Approach

Analysis Using the OAS Approach Bond OAS (in bps) Bond 1 25.5 Bond 2 30.3

Hsu then selects the four bonds issued by Rw, inc. given in Exhibit 2. These bonds all have a maturity of three years and the same credit rating. Bonds 4 and 5 are identical to Bond3, an option-free bond, except that they each include an embedded option.

EXHIBIT 2 Bonds Issued by RW, Inc. Bond Coupon Special Provision Bond 3 4.00\% annual Bond 4 4.00\% annual Callable at par at the end of years 1 and 2 Bond 5 4.00\% annual Putable at par at the end of years 1 and 2 Bond 6 One-year Libor annually, set in arrears

To value and analyze Rw's bonds, Hsu uses an estimated interest rate volatility of 15% and constructs the binomial interest rate tree provided in Exhibit 3.

Rayes asks Hsu to determine the sensitivity of Bond 4's price to a 20 bps parallel shift ofthe benchmark yield curve. The results of Hsu's calculations are shown in Exhibit 4.EXHiBiT 4 Summary Results of Hsu's Analysis about the Sensitivity of Bond 4's Price to a ParallelShift of the Benchmark yield Curve Magnitude of the Parallel Shift in the Benchmark yield Curve +20 bps −20 bps full Price of Bond 4 (% of par) 100.478 101.238 Hsu also selects the two floating-rate bonds issued by Varlep, plc given in Exhibit 5. These

bonds have a maturity of three years and the same credit rating.

EXHIBIT 5 Floating-Rate Bonds Issued by Varlep, plc Bond Coupon Bond 7 One-year Libor annually, set in arrears, capped at 5.00\% Bond 8 One-year Libor annually, set in arrears, floored at 3.50\%

To value Varlep's bonds, Hsu constructs the binomial interest rate tree provided inExhibit 6.

last, Hsu selects the two bonds issued by whorton, inc. given in Exhibit 7. These bonds are close to their maturity date and are identical, except that Bond 9 includes a conversion option. whorton's common stock is currently trading at $30 per share.

EXHІВАТ 7 Bonds Issued by Whorton, Inc. Bond Type of Bond Bond 9 Convertible bond with a conversion price of \ 50 Bond 10 Identical to Bond 9 except that it does not include a conversion option

-The minimum value of Bond 9 is equal to the greater of:

(Multiple Choice)

4.7/5 (36)

The following information relates to Questions 20-27John Smith, an investment adviser, meets with lydia Carter to discuss her pending retirement

and potential changes to her investment portfolio. domestic economic activity has been weak-ening recently, and Smith's outlook is that equity market values will be lower during the next year. He would like Carter to consider reducing her equity exposure in favor of adding more fixed-income securities to the portfolio.Government yields have remained low for an extended period, and Smith suggests con-sidering investment-grade corporate bonds to provide additional yield above government debt issues. in light of recent poor employment figures and two consecutive quarters of negative GdP growth, the consensus forecast among economists is that the central bank, at its next meeting this month, will take actions that will lead to lower interest rates.

Smith and Carter review par, spot, and one-year forward rates (Exhibit 1) and four fixed- rate investment-grade bonds issued by Alpha Corporation that are being considered for invest-ment (Exhibit 2).

EXHIBTT 1 Par, Spot, and One-Year Forward Rates (annual coupon payments) Maturity (Years) Par Rate (\%) Spot Rate (\%) One-Year Forward (\%) 1 1.0000 1.0000 1.0000 2 1.2000 1.2012 1.4028 3 1.2500 1.2515 1.3522

EXHIBIT 2 Selected Fixed-Rate Bonds of Alpha Corporation

Bond Annual Coupon Type of Bond Bond 1 1.5500\% Straight bond Bond 2 1.5500\% Convertible bond: currently trading out of the money Bond 3 1.5500\% Putable bond: putable at par one year and two years from now Bond 4 1.5500\% Callable bond: callable at par without any lockout periods

Note: All bonds in Exhibit 2 have remaining maturities of exactly three years.

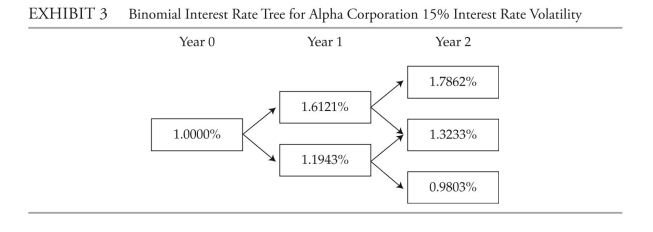

Carter tells Smith that the local news media have been reporting that housing starts,exports, and demand for consumer credit are all relatively strong, even in light of other poor macroeconomic indicators. Smith explains that the divergence in economic data leads him to believe that volatility in interest rates will increase. Smith also states that he recently read a report issued by Brown and Company forecasting that the yield curve could invert within the next six months. Smith develops a binomial interest rate tree with a 15% interest rate volatility assumption to assess the value of Alpha Corporation's bonds. Exhibit 3 presents the interest rate tree.

Carter asks Smith about the possibility of nalyzing bonds that have lower credit rat-ings than the investment-grade Alpha bonds. Smith discusses four other corporate bonds with Carter. Exhibit 4 presents selected data on the four bonds. EXHiBiT 4 Selected information on fixed-Rate Bonds for Beta, Gamma, delta, and Rho

\begin{array}{lllc}\hline\text { Bond } & \text { Issuer } & \text { Bond Features } & \text { Credit Rating } \\\hline \text { Bond 5 } & \text { Beta Corporation } & \text { Coupon 1.70\% } & \text { B } \\& & \text { Callable in Year 2 } & \\& &\text { OAS of } 45 \text { bps } & \\\text { Bond 6 } & \text { Gamma Corporation } & \text { Coupon 1.70\% } \\& & \text { Callable in Year 2 } & \\&& \text { OAS of 65 bps } \\\text { Bond 7 } & \text { Delta Corporation } & \text { Coupon 1.70\% }&\text { B }\\ & & \text { Callable in Year 2 } & \\& & \text { OAS of } 85\\\text { Bond 8 }& \text { Rho Corporation } & \text { Coupon 1.70\% } & \text { CCC } \\&&\text {Callable in Year 2}\\&&\text {OAS of 105 \mathrm{bps} }\\\hline\end{array}

Notes: All bonds have remaining maturities of three years. oAS stands for option-adjusted spread.

-Based on Exhibit 2, and assuming that the forecast for interest rates and Smith's outlook for equity returns are validated, which bond's option is most likely to be exercised?

Carter asks Smith about the possibility of nalyzing bonds that have lower credit rat-ings than the investment-grade Alpha bonds. Smith discusses four other corporate bonds with Carter. Exhibit 4 presents selected data on the four bonds. EXHiBiT 4 Selected information on fixed-Rate Bonds for Beta, Gamma, delta, and Rho

\begin{array}{lllc}\hline\text { Bond } & \text { Issuer } & \text { Bond Features } & \text { Credit Rating } \\\hline \text { Bond 5 } & \text { Beta Corporation } & \text { Coupon 1.70\% } & \text { B } \\& & \text { Callable in Year 2 } & \\& &\text { OAS of } 45 \text { bps } & \\\text { Bond 6 } & \text { Gamma Corporation } & \text { Coupon 1.70\% } \\& & \text { Callable in Year 2 } & \\&& \text { OAS of 65 bps } \\\text { Bond 7 } & \text { Delta Corporation } & \text { Coupon 1.70\% }&\text { B }\\ & & \text { Callable in Year 2 } & \\& & \text { OAS of } 85\\\text { Bond 8 }& \text { Rho Corporation } & \text { Coupon 1.70\% } & \text { CCC } \\&&\text {Callable in Year 2}\\&&\text {OAS of 105 \mathrm{bps} }\\\hline\end{array}

Notes: All bonds have remaining maturities of three years. oAS stands for option-adjusted spread.

-Based on Exhibit 2, and assuming that the forecast for interest rates and Smith's outlook for equity returns are validated, which bond's option is most likely to be exercised?

(Multiple Choice)

5.0/5 (33)

The following information relates to Questions 11-19

Rayes investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm's bond port-folio. Rayes has asked Mingfang Hsu, one of the firm's analysts, to assist her in selecting and analyzing bonds for possible inclusion in the firm's bond portfolio.Hsu first selects two corporate bonds that are callable at par and have the same character-istics in terms of maturity, credit quality and call dates. Hsu uses the option-adjusted spread(oAS) approach to analyse the bonds, assuming an interest rate volatility of 10%. The resultsof his analysis are presented in Exhibit 1.

EXHIBIT 1 Summary Results of Hsu's Analysis Using the OAS Approach

Analysis Using the OAS Approach Bond OAS (in bps) Bond 1 25.5 Bond 2 30.3

Hsu then selects the four bonds issued by Rw, inc. given in Exhibit 2. These bonds all have a maturity of three years and the same credit rating. Bonds 4 and 5 are identical to Bond3, an option-free bond, except that they each include an embedded option.

EXHIBIT 2 Bonds Issued by RW, Inc. Bond Coupon Special Provision Bond 3 4.00\% annual Bond 4 4.00\% annual Callable at par at the end of years 1 and 2 Bond 5 4.00\% annual Putable at par at the end of years 1 and 2 Bond 6 One-year Libor annually, set in arrears

To value and analyze Rw's bonds, Hsu uses an estimated interest rate volatility of 15% and constructs the binomial interest rate tree provided in Exhibit 3.

Rayes asks Hsu to determine the sensitivity of Bond 4's price to a 20 bps parallel shift ofthe benchmark yield curve. The results of Hsu's calculations are shown in Exhibit 4.EXHiBiT 4 Summary Results of Hsu's Analysis about the Sensitivity of Bond 4's Price to a ParallelShift of the Benchmark yield Curve Magnitude of the Parallel Shift in the Benchmark yield Curve +20 bps −20 bps full Price of Bond 4 (% of par) 100.478 101.238 Hsu also selects the two floating-rate bonds issued by Varlep, plc given in Exhibit 5. These

bonds have a maturity of three years and the same credit rating.

EXHIBIT 5 Floating-Rate Bonds Issued by Varlep, plc Bond Coupon Bond 7 One-year Libor annually, set in arrears, capped at 5.00\% Bond 8 One-year Libor annually, set in arrears, floored at 3.50\%

To value Varlep's bonds, Hsu constructs the binomial interest rate tree provided inExhibit 6.

last, Hsu selects the two bonds issued by whorton, inc. given in Exhibit 7. These bonds are close to their maturity date and are identical, except that Bond 9 includes a conversion option. whorton's common stock is currently trading at $30 per share.

EXHІВАТ 7 Bonds Issued by Whorton, Inc. Bond Type of Bond Bond 9 Convertible bond with a conversion price of \ 50 Bond 10 Identical to Bond 9 except that it does not include a conversion option

-in Exhibit 2, the bond whose effective duration will lengthen if interest rates rise is:

(Multiple Choice)

4.9/5 (31)

The following information relates to Questions 1-10

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. on 1 october 20X0, Steele ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, inc. The three bonds, whose characteristics are given in Exhibit 1, carry the highest credit rating.

EXHiBiT 1 fixed-Rate Bonds issued by Pro Star, inc.

Bond Maturity Coupon Type of Bond Bond 1 1 October 20X3 4.40\% annual Option-free Bond 2 1 October 20X3 4.40\% annual Callable at par on 1 October 20X1 and on 1 October 20X2 Bond 3 1 October 20X3 4.40\% annual Putable at par on 1 October 20X1 and on 1 October 20X2

The one-year, two-year, and three-year par rates are 2.250%, 2.750%, and 3.100%, re-spectively. Based on an estimated interest rate volatility of 10%, ferguson constructs the bino-mial interest rate tree shown in Exhibit 2.

EXHiBiT 2 Binomial interest Rate Tree

on 19 october 20X0, ferguson analyzes the convertible bond issued by Pro Star given in Exhibit 3. That day, the option-free value of Pro Star's convertible bond is $1,060 and Pro Star's stock price is $37.50.

EXHiBiT 3 Convertible Bond issued by Pro Star, inc.

Issue Date: 6 December 20X0 Maturity Date: 6 December 20X4 Coupon Rate: 2\% Issue Price: \ 1,000 Conversion Ratio: 31

-All else being equal, if the shape of the yield curve changes from upward sloping to flat- tening, the value of the option embedded in Bond 2 will most likely:

(Multiple Choice)

4.9/5 (36)

Based on Exhibit 4, the arbitrage-free value of the Ri bond is closest to:

(Multiple Choice)

4.7/5 (35)

Based on the information in Exhibit 1 and Exhibit 2, the value of the embedded option in Bond 4 is closest to:

(Multiple Choice)

4.7/5 (26)

The following information relates to Questions 1-10

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. on 1 october 20X0, Steele ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, inc. The three bonds, whose characteristics are given in Exhibit 1, carry the highest credit rating.

EXHiBiT 1 fixed-Rate Bonds issued by Pro Star, inc.

Bond Maturity Coupon Type of Bond Bond 1 1 October 20X3 4.40\% annual Option-free Bond 2 1 October 20X3 4.40\% annual Callable at par on 1 October 20X1 and on 1 October 20X2 Bond 3 1 October 20X3 4.40\% annual Putable at par on 1 October 20X1 and on 1 October 20X2

The one-year, two-year, and three-year par rates are 2.250%, 2.750%, and 3.100%, re-spectively. Based on an estimated interest rate volatility of 10%, ferguson constructs the bino-mial interest rate tree shown in Exhibit 2.

EXHiBiT 2 Binomial interest Rate Tree

on 19 october 20X0, ferguson analyzes the convertible bond issued by Pro Star given in Exhibit 3. That day, the option-free value of Pro Star's convertible bond is $1,060 and Pro Star's stock price is $37.50.

EXHiBiT 3 Convertible Bond issued by Pro Star, inc.

Issue Date: 6 December 20X0 Maturity Date: 6 December 20X4 Coupon Rate: 2\% Issue Price: \ 1,000 Conversion Ratio: 31

-The call feature of Bond 2 is best described as:

(Multiple Choice)

4.8/5 (35)

The following information relates to Questions 1-10

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. on 1 october 20X0, Steele ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, inc. The three bonds, whose characteristics are given in Exhibit 1, carry the highest credit rating.

EXHiBiT 1 fixed-Rate Bonds issued by Pro Star, inc.

Bond Maturity Coupon Type of Bond Bond 1 1 October 20X3 4.40\% annual Option-free Bond 2 1 October 20X3 4.40\% annual Callable at par on 1 October 20X1 and on 1 October 20X2 Bond 3 1 October 20X3 4.40\% annual Putable at par on 1 October 20X1 and on 1 October 20X2

The one-year, two-year, and three-year par rates are 2.250%, 2.750%, and 3.100%, re-spectively. Based on an estimated interest rate volatility of 10%, ferguson constructs the bino-mial interest rate tree shown in Exhibit 2.

EXHiBiT 2 Binomial interest Rate Tree

on 19 october 20X0, ferguson analyzes the convertible bond issued by Pro Star given in Exhibit 3. That day, the option-free value of Pro Star's convertible bond is $1,060 and Pro Star's stock price is $37.50.

EXHiBiT 3 Convertible Bond issued by Pro Star, inc.

Issue Date: 6 December 20X0 Maturity Date: 6 December 20X4 Coupon Rate: 2\% Issue Price: \ 1,000 Conversion Ratio: 31

-if the market price of Pro Star's common stock falls from its level on 19 october 20X0, the price of the convertible bond will most likely:

(Multiple Choice)

4.8/5 (31)

Based on Exhibit 3, if delille Enterprises pays the dividend expected by Gillette, the con- version price of the dE bond will:

(Multiple Choice)

4.8/5 (32)

The following information relates to Questions 11-19

Rayes investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm's bond port-folio. Rayes has asked Mingfang Hsu, one of the firm's analysts, to assist her in selecting and analyzing bonds for possible inclusion in the firm's bond portfolio.Hsu first selects two corporate bonds that are callable at par and have the same character-istics in terms of maturity, credit quality and call dates. Hsu uses the option-adjusted spread(oAS) approach to analyse the bonds, assuming an interest rate volatility of 10%. The resultsof his analysis are presented in Exhibit 1.

EXHIBIT 1 Summary Results of Hsu's Analysis Using the OAS Approach

Analysis Using the OAS Approach Bond OAS (in bps) Bond 1 25.5 Bond 2 30.3

Hsu then selects the four bonds issued by Rw, inc. given in Exhibit 2. These bonds all have a maturity of three years and the same credit rating. Bonds 4 and 5 are identical to Bond3, an option-free bond, except that they each include an embedded option.

EXHIBIT 2 Bonds Issued by RW, Inc. Bond Coupon Special Provision Bond 3 4.00\% annual Bond 4 4.00\% annual Callable at par at the end of years 1 and 2 Bond 5 4.00\% annual Putable at par at the end of years 1 and 2 Bond 6 One-year Libor annually, set in arrears

To value and analyze Rw's bonds, Hsu uses an estimated interest rate volatility of 15% and constructs the binomial interest rate tree provided in Exhibit 3.

Rayes asks Hsu to determine the sensitivity of Bond 4's price to a 20 bps parallel shift ofthe benchmark yield curve. The results of Hsu's calculations are shown in Exhibit 4.EXHiBiT 4 Summary Results of Hsu's Analysis about the Sensitivity of Bond 4's Price to a ParallelShift of the Benchmark yield Curve Magnitude of the Parallel Shift in the Benchmark yield Curve +20 bps −20 bps full Price of Bond 4 (% of par) 100.478 101.238 Hsu also selects the two floating-rate bonds issued by Varlep, plc given in Exhibit 5. These

bonds have a maturity of three years and the same credit rating.

EXHIBIT 5 Floating-Rate Bonds Issued by Varlep, plc Bond Coupon Bond 7 One-year Libor annually, set in arrears, capped at 5.00\% Bond 8 One-year Libor annually, set in arrears, floored at 3.50\%

To value Varlep's bonds, Hsu constructs the binomial interest rate tree provided inExhibit 6.

last, Hsu selects the two bonds issued by whorton, inc. given in Exhibit 7. These bonds are close to their maturity date and are identical, except that Bond 9 includes a conversion option. whorton's common stock is currently trading at $30 per share.

EXHІВАТ 7 Bonds Issued by Whorton, Inc. Bond Type of Bond Bond 9 Convertible bond with a conversion price of \ 50 Bond 10 Identical to Bond 9 except that it does not include a conversion option

-The value of Bond 8 is closest to:

(Multiple Choice)

4.8/5 (46)

The following information relates to Questions 1-10

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. on 1 october 20X0, Steele ferguson, a senior analyst at Samuel, is reviewing three fixed-rate bonds issued by a local firm, Pro Star, inc. The three bonds, whose characteristics are given in Exhibit 1, carry the highest credit rating.

EXHiBiT 1 fixed-Rate Bonds issued by Pro Star, inc.

Bond Maturity Coupon Type of Bond Bond 1 1 October 20X3 4.40\% annual Option-free Bond 2 1 October 20X3 4.40\% annual Callable at par on 1 October 20X1 and on 1 October 20X2 Bond 3 1 October 20X3 4.40\% annual Putable at par on 1 October 20X1 and on 1 October 20X2

The one-year, two-year, and three-year par rates are 2.250%, 2.750%, and 3.100%, re-spectively. Based on an estimated interest rate volatility of 10%, ferguson constructs the bino-mial interest rate tree shown in Exhibit 2.

EXHiBiT 2 Binomial interest Rate Tree

on 19 october 20X0, ferguson analyzes the convertible bond issued by Pro Star given in Exhibit 3. That day, the option-free value of Pro Star's convertible bond is $1,060 and Pro Star's stock price is $37.50.

EXHiBiT 3 Convertible Bond issued by Pro Star, inc.

Issue Date: 6 December 20X0 Maturity Date: 6 December 20X4 Coupon Rate: 2\% Issue Price: \ 1,000 Conversion Ratio: 31

-All else being equal, if ferguson assumes an interest rate volatility of 15% instead of 10%, the bond that would most likely increase in value is:

(Multiple Choice)

5.0/5 (40)

The following information relates to Questions 11-19

Rayes investment Advisers specializes in fixed-income portfolio management. Meg Rayes, the owner of the firm, would like to add bonds with embedded options to the firm's bond port-folio. Rayes has asked Mingfang Hsu, one of the firm's analysts, to assist her in selecting and analyzing bonds for possible inclusion in the firm's bond portfolio.Hsu first selects two corporate bonds that are callable at par and have the same character-istics in terms of maturity, credit quality and call dates. Hsu uses the option-adjusted spread(oAS) approach to analyse the bonds, assuming an interest rate volatility of 10%. The resultsof his analysis are presented in Exhibit 1.

EXHIBIT 1 Summary Results of Hsu's Analysis Using the OAS Approach

Analysis Using the OAS Approach Bond OAS (in bps) Bond 1 25.5 Bond 2 30.3

Hsu then selects the four bonds issued by Rw, inc. given in Exhibit 2. These bonds all have a maturity of three years and the same credit rating. Bonds 4 and 5 are identical to Bond3, an option-free bond, except that they each include an embedded option.

EXHIBIT 2 Bonds Issued by RW, Inc. Bond Coupon Special Provision Bond 3 4.00\% annual Bond 4 4.00\% annual Callable at par at the end of years 1 and 2 Bond 5 4.00\% annual Putable at par at the end of years 1 and 2 Bond 6 One-year Libor annually, set in arrears

To value and analyze Rw's bonds, Hsu uses an estimated interest rate volatility of 15% and constructs the binomial interest rate tree provided in Exhibit 3.

Rayes asks Hsu to determine the sensitivity of Bond 4's price to a 20 bps parallel shift ofthe benchmark yield curve. The results of Hsu's calculations are shown in Exhibit 4.EXHiBiT 4 Summary Results of Hsu's Analysis about the Sensitivity of Bond 4's Price to a ParallelShift of the Benchmark yield Curve Magnitude of the Parallel Shift in the Benchmark yield Curve +20 bps −20 bps full Price of Bond 4 (% of par) 100.478 101.238 Hsu also selects the two floating-rate bonds issued by Varlep, plc given in Exhibit 5. These

bonds have a maturity of three years and the same credit rating.

EXHIBIT 5 Floating-Rate Bonds Issued by Varlep, plc Bond Coupon Bond 7 One-year Libor annually, set in arrears, capped at 5.00\% Bond 8 One-year Libor annually, set in arrears, floored at 3.50\%

To value Varlep's bonds, Hsu constructs the binomial interest rate tree provided inExhibit 6.

last, Hsu selects the two bonds issued by whorton, inc. given in Exhibit 7. These bonds are close to their maturity date and are identical, except that Bond 9 includes a conversion option. whorton's common stock is currently trading at $30 per share.

EXHІВАТ 7 Bonds Issued by Whorton, Inc. Bond Type of Bond Bond 9 Convertible bond with a conversion price of \ 50 Bond 10 Identical to Bond 9 except that it does not include a conversion option

-The effective duration of Bond 4 is closest to:

(Multiple Choice)

4.8/5 (35)

which of the following conclusions regarding the bonds in Exhibit 4 is correct?

(Multiple Choice)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)