Exam 9: Price Takers and the Competitive Process

Exam 1: The Economic Approach210 Questions

Exam 2: Some Tools of the Economist257 Questions

Exam 3: Demand, Supply, and the Market Process585 Questions

Exam 4: Supply and Demand: Applications and Extensions331 Questions

Exam 5: Difficult Cases for the Market, and the Role of Government168 Questions

Exam 6: The Economics of Political Action360 Questions

Exam 7: Consumer Choice and Elasticity223 Questions

Exam 8: Costs and the Supply of Goods231 Questions

Exam 9: Price Takers and the Competitive Process497 Questions

Exam 10: Price-Searcher Markets With Low Entry Barriers216 Questions

Exam 11: Price-Searcher Markets With High Entry Barriers254 Questions

Exam 12: The Supply of and Demand for Productive Resources200 Questions

Exam 13: Earnings, Productivity, and the Job Market109 Questions

Exam 14: Investment, the Capital Market, and the Wealth of Nations129 Questions

Exam 15: Income Inequality and Poverty136 Questions

Exam 16: Applying the Basics: Special Topics in Economics709 Questions

Select questions type

When firms have an incentive to exit a competitive price-taker market, their exit will

(Multiple Choice)

4.8/5  (32)

(32)

If the ice cream industry is a competitive price-taker market and all ice cream producers are earning zero economic profit, what will be the impact of an increase in the demand for ice cream?

(Multiple Choice)

4.8/5 (30)

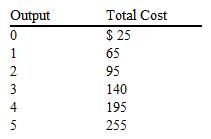

The schedule of total cost for a firm in a price-taker market is given in the table. If the market price for this product is $50, which of the following output levels should this firm produce if it wants to maximize its profit?

(Multiple Choice)

4.7/5 (35)

If there is an increase in market demand in a competitive price-taker market, then in the short run

(Multiple Choice)

4.8/5 (33)

The intersection of a firm's marginal revenue and marginal cost curves determines the level of output at which

(Multiple Choice)

4.8/5 (32)

Suppose sharply higher coffee prices lead to an increase in demand for tea. As tea prices increase, tea producers experience short-run economic profits. If the tea industry is a price-taker industry and if sufficient time is allowed for the market to adjust fully to the increase in demand for tea, one would expect the tea industry's output to

(Multiple Choice)

4.8/5 (36)

Which of the following best explains why a firm in a competitive price-taker market must take the price determined in the market?

(Multiple Choice)

4.9/5 (36)

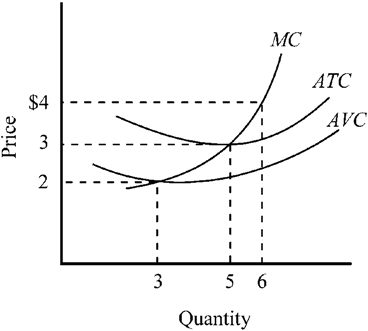

Use the figure to answer the following question(s).

Figure 9-5

If the market price in Figure 9-5 fell to $2.50, what should the firm do?

If the market price in Figure 9-5 fell to $2.50, what should the firm do?

(Multiple Choice)

4.8/5 (29)

To maximize profits, a firm should always produce the level of output where

(Multiple Choice)

4.7/5 (36)

If long-run equilibrium is present in a competitive market, the typical firm in the market will be

(Multiple Choice)

4.9/5 (32)

When the marginal cost of a price-taker firm is more than the market price of its product, the firm should

(Multiple Choice)

4.9/5 (34)

There are 1,000 identical firms in a price-taker industry. In the short run, the total revenues of each firm are less than total costs. What will happen in the long run?

(Multiple Choice)

4.9/5 (26)

Which of the following best explains why price in competitive price-taker markets will tend to be driven to the minimum per-unit cost?

(Multiple Choice)

4.8/5 (31)

Suppose antitheft auto alarms are produced in a price-taker market that is initially in long-run equilibrium. It is estimated that only 23 percent of all autos have alarms. Due to rising auto theft, Congress mandates alarms in every vehicle. Assume complete compliance. If the industry is an increasing cost industry, price will

(Multiple Choice)

4.8/5 (32)

If resource prices rise and the per-unit cost of producing a product increases as the firms in an industry expand output in response to an increase in demand, the long-run market supply curve for the product will

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)