Exam 9: Price Takers and the Competitive Process

Exam 1: The Economic Approach210 Questions

Exam 2: Some Tools of the Economist257 Questions

Exam 3: Demand, Supply, and the Market Process585 Questions

Exam 4: Supply and Demand: Applications and Extensions331 Questions

Exam 5: Difficult Cases for the Market, and the Role of Government168 Questions

Exam 6: The Economics of Political Action360 Questions

Exam 7: Consumer Choice and Elasticity223 Questions

Exam 8: Costs and the Supply of Goods231 Questions

Exam 9: Price Takers and the Competitive Process497 Questions

Exam 10: Price-Searcher Markets With Low Entry Barriers216 Questions

Exam 11: Price-Searcher Markets With High Entry Barriers254 Questions

Exam 12: The Supply of and Demand for Productive Resources200 Questions

Exam 13: Earnings, Productivity, and the Job Market109 Questions

Exam 14: Investment, the Capital Market, and the Wealth of Nations129 Questions

Exam 15: Income Inequality and Poverty136 Questions

Exam 16: Applying the Basics: Special Topics in Economics709 Questions

Select questions type

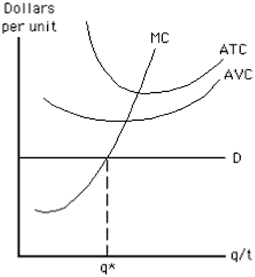

Figure 9-17  Which of the following statements about the competitive price-taker firm represented in Figure 9-17 is false?

Which of the following statements about the competitive price-taker firm represented in Figure 9-17 is false?

(Multiple Choice)

4.8/5  (37)

(37)

If a restaurant in a summer tourist area is highly profitable during the summer months but unable to cover even its variable costs during the winter months, the restaurant should

(Multiple Choice)

4.9/5 (41)

The short-run supply curve in a price-taking industry is the

(Multiple Choice)

4.8/5 (29)

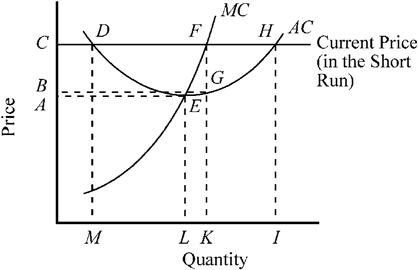

Use the figure to answer the following question(s).

Figure 9-11

Which of the following represents the firm's total cost of producing the profit-maximizing output in Figure 9-11?

Which of the following represents the firm's total cost of producing the profit-maximizing output in Figure 9-11?

(Multiple Choice)

4.9/5 (28)

When new firms have an incentive to enter a competitive price-taker market, their entry will

(Multiple Choice)

5.0/5 (41)

When the conditions in a competitive price-taker market are such that the firms are consistently unable to cover their production costs,

(Multiple Choice)

4.9/5 (31)

In a constant-cost industry, an increase in output that increases the demand for resources used by the industry

(Multiple Choice)

4.8/5 (33)

The price-taker firm should discontinue production immediately if

(Multiple Choice)

4.7/5 (39)

If a decrease in the demand for corn leads to economic losses for corn farmers,

(Multiple Choice)

5.0/5 (35)

In the short run, a perfectly competitive firm will always shut down if total revenue is ____ at all positive output levels.

(Multiple Choice)

4.9/5 (46)

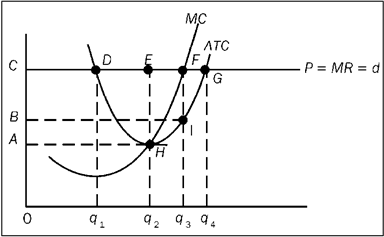

The figure depicts a firm in a price-taker market. Use this figure to answer the following question(s).

Figure 9-18

Refer to Figure 9-18. At the profit-maximizing level of output, the firm will earn an economic (Hint: Areas in the exhibit are referenced by the four letters on the corners of the respective area.)

Refer to Figure 9-18. At the profit-maximizing level of output, the firm will earn an economic (Hint: Areas in the exhibit are referenced by the four letters on the corners of the respective area.)

(Multiple Choice)

4.7/5 (40)

Which of the following business decisions will be made by firms that are price searchers but not those that are price takers?

(Multiple Choice)

4.9/5 (34)

A competitive price-taker firm's marginal cost curve is regarded as its supply curve because

(Multiple Choice)

4.9/5 (42)

Suppose that sharply lower coffee prices lead to a decrease in the demand for tea. Tea price decreases, and the tea producers experience short-run economic losses. If the tea industry is a price-taker market, after sufficient time is allowed for the market to adjust fully to the decrease in the demand for tea, one would expect the tea industry's output to

(Multiple Choice)

4.9/5 (41)

The ability of price-taker firms to freely expand or contract their businesses and to enter or exit the market means that

(Multiple Choice)

4.9/5 (32)

In a constant-cost industry, an increase in output that increases the demand for resources used by the industry

(Multiple Choice)

4.8/5 (29)

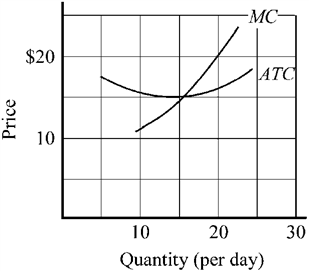

Use the figure to answer the following question(s).

Figure 9-6

The average total cost ( ATC ) and marginal costs ( MC ) of a firm producing in a price-taker industry are depicted in Figure 9-6. If the current market price of the firm's product is $15, what output should this firm produce?

The average total cost ( ATC ) and marginal costs ( MC ) of a firm producing in a price-taker industry are depicted in Figure 9-6. If the current market price of the firm's product is $15, what output should this firm produce?

(Multiple Choice)

4.8/5 (39)

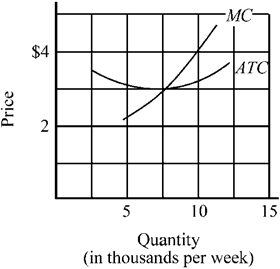

Use the figure to answer the following question(s).

Figure 9-7

The average total cost ( ATC ) and marginal costs ( MC ) of a firm producing in a price-taker industry are depicted in Figure 9-7. If the current market price of the firm's product is $3, what output should this firm produce per week?

The average total cost ( ATC ) and marginal costs ( MC ) of a firm producing in a price-taker industry are depicted in Figure 9-7. If the current market price of the firm's product is $3, what output should this firm produce per week?

(Multiple Choice)

4.9/5 (37)

The usefulness of the price-taker model requires that the firm's decision makers

(Multiple Choice)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)