Exam 9: Price Takers and the Competitive Process

Exam 1: The Economic Approach210 Questions

Exam 2: Some Tools of the Economist257 Questions

Exam 3: Demand, Supply, and the Market Process585 Questions

Exam 4: Supply and Demand: Applications and Extensions331 Questions

Exam 5: Difficult Cases for the Market, and the Role of Government168 Questions

Exam 6: The Economics of Political Action360 Questions

Exam 7: Consumer Choice and Elasticity223 Questions

Exam 8: Costs and the Supply of Goods231 Questions

Exam 9: Price Takers and the Competitive Process497 Questions

Exam 10: Price-Searcher Markets With Low Entry Barriers216 Questions

Exam 11: Price-Searcher Markets With High Entry Barriers254 Questions

Exam 12: The Supply of and Demand for Productive Resources200 Questions

Exam 13: Earnings, Productivity, and the Job Market109 Questions

Exam 14: Investment, the Capital Market, and the Wealth of Nations129 Questions

Exam 15: Income Inequality and Poverty136 Questions

Exam 16: Applying the Basics: Special Topics in Economics709 Questions

Select questions type

Several producers in industry A developed an improved technology that reduces the quantity of resources used to produce a given output. Which of the following would be expected?

(Multiple Choice)

4.8/5  (50)

(50)

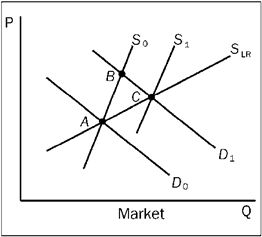

Which of the following best describes the series of events shown in the figure? The original conditions prior to the change are shown by D 0 and S 0 (point A), and S LR is the market long-run supply curve.

(Multiple Choice)

5.0/5 (33)

When competition is present, self-interested business decision makers have a strong incentive to

(Multiple Choice)

4.8/5 (36)

Regardless of quantity in long-run equilibrium, the competitive price-taker market price cannot exceed the

(Multiple Choice)

4.9/5 (39)

Which of the following products would most closely fit the competitive price-taker model?

(Multiple Choice)

4.7/5 (38)

If the market price in a price-taking industry was currently above the average total cost of production for firms in the industry,

(Multiple Choice)

4.9/5 (30)

If a single firm in a price-taker market lowers its price below the market equilibrium price,

(Multiple Choice)

4.8/5 (42)

If marginal revenue exceeds marginal cost, a price-taker firm should

(Multiple Choice)

4.8/5 (32)

When market conditions in a price-taker market are such that firms cannot cover their production costs,

(Multiple Choice)

4.7/5 (41)

If marginal revenue exceeds marginal cost at the current level of output, profit will increase when output is expanded because

(Multiple Choice)

4.8/5 (34)

When firms in a price-taker market are temporarily able to charge prices that exceed their production costs,

(Multiple Choice)

4.7/5 (32)

You are the owner of an ice cream shop that earns a profit most of the year except during the cold winter months. During the month of December, your rent and other fixed costs amount to a total of $200. If you remain open, your total variable costs (workers, ice cream cones, etc.) will amount to $300. If you would be able to sell 100 ice cream cones at $4 each during December, then

(Multiple Choice)

4.8/5 (41)

The short-run supply curve in a price-taking industry is the

(Multiple Choice)

4.7/5 (42)

When new firms have an incentive to enter a competitive price-taker market, their entry will

(Multiple Choice)

4.8/5 (35)

Suppose Thelma and Louise both sell fried green tomatoes in a competitive price-taker market. If Louise increases her output,

(Multiple Choice)

4.8/5 (45)

The market for a competitive price-taker market clears at a price of $3, and the minimum average cost for all firms is $2.50. In the long run, we would expect an increase in

(Multiple Choice)

4.8/5 (36)

If a product is manufactured under conditions of constant cost, an increase in the demand for the product will increase

(Multiple Choice)

4.7/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)