Exam 9: Price Takers and the Competitive Process

Exam 1: The Economic Approach210 Questions

Exam 2: Some Tools of the Economist257 Questions

Exam 3: Demand, Supply, and the Market Process585 Questions

Exam 4: Supply and Demand: Applications and Extensions331 Questions

Exam 5: Difficult Cases for the Market, and the Role of Government168 Questions

Exam 6: The Economics of Political Action360 Questions

Exam 7: Consumer Choice and Elasticity223 Questions

Exam 8: Costs and the Supply of Goods231 Questions

Exam 9: Price Takers and the Competitive Process497 Questions

Exam 10: Price-Searcher Markets With Low Entry Barriers216 Questions

Exam 11: Price-Searcher Markets With High Entry Barriers254 Questions

Exam 12: The Supply of and Demand for Productive Resources200 Questions

Exam 13: Earnings, Productivity, and the Job Market109 Questions

Exam 14: Investment, the Capital Market, and the Wealth of Nations129 Questions

Exam 15: Income Inequality and Poverty136 Questions

Exam 16: Applying the Basics: Special Topics in Economics709 Questions

Select questions type

If a product is manufactured under conditions of constant cost, an increase in the demand for the product will increase

(Multiple Choice)

4.8/5  (37)

(37)

When profits occur in a competitive market, this indicates that

(Multiple Choice)

4.8/5 (35)

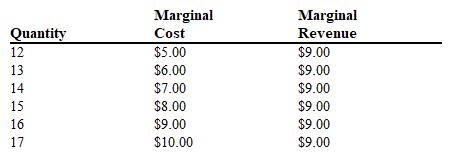

Table 9-2

Refer to Table 9-2. This table provides information on a competitive price-taker firm's output, marginal revenue, and marginal cost. If the firm is currently producing 14 units, what would you advise them to do?

Refer to Table 9-2. This table provides information on a competitive price-taker firm's output, marginal revenue, and marginal cost. If the firm is currently producing 14 units, what would you advise them to do?

(Multiple Choice)

4.7/5 (42)

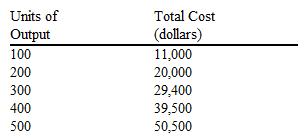

The schedule of total costs for a chair-manufacturing firm is presented in the table below. If the market price of chairs is $100, which output should this price-taker firm produce to maximize profit?

(Multiple Choice)

4.7/5 (34)

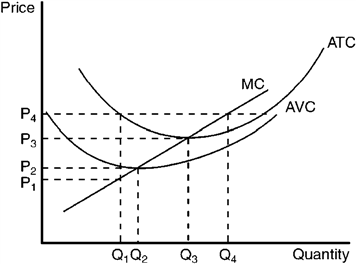

The graph below depicts the cost structure for a firm in a competitive market.

Figure 9-13

Refer to Figure 9-13. When price rises from P3 to P4, the firm finds that

Refer to Figure 9-13. When price rises from P3 to P4, the firm finds that

(Multiple Choice)

4.8/5 (35)

When a firm in a competitive market is earning profits, this indicates that the firm is

(Multiple Choice)

4.9/5 (37)

In general, firms will produce at a rate of output such that marginal revenue equals marginal cost because this output rate will

(Multiple Choice)

4.8/5 (44)

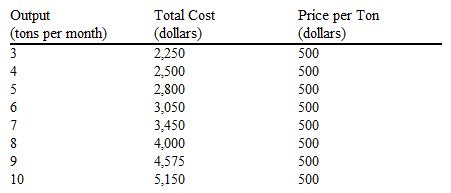

Use the table of expected cost and revenue data for the Tuckers Tomato Farm below to answer the following question(s). The Tuckers produce tomatoes in a greenhouse and sell them wholesale in a competitive price-taker market.

Table 9-1

Refer to Table 9-1. If the market price is $500, what is the maximum economic profit per month the Tuckers can earn?

Refer to Table 9-1. If the market price is $500, what is the maximum economic profit per month the Tuckers can earn?

(Multiple Choice)

4.9/5 (33)

Firms that can choose what price they will charge for their product and can increase the number of units sold by reducing price are called

(Multiple Choice)

4.8/5 (38)

At a firm's profit-maximizing level of output, its price is $200 and its short-run average total cost is $225. The firm

(Multiple Choice)

4.8/5 (28)

If a competitive price-taker firm is currently producing a level of output at which marginal cost exceeds marginal revenue, then

(Multiple Choice)

4.9/5 (37)

Which of the following is true for a constant cost industry?

(Multiple Choice)

4.8/5 (39)

If occupational safety laws were changed so that firms no longer had to take expensive steps to meet regulatory requirements, we would expect

(Multiple Choice)

4.9/5 (31)

Profit-maximizing firms enter a competitive market when, for existing firms in that market,

(Multiple Choice)

4.9/5 (44)

Tom, a math major, examines Jane's economics class notes and observes that when price-taking firms earn economic profit, they do not seem to produce a quantity that minimizes their costs. Is he correct? Is there significance to this observation?

(Essay)

4.8/5 (40)

When consumer demand for a good produced in a price-taker market decreases,

(Multiple Choice)

4.8/5 (43)

A perfectly elastic, long-run market supply curve is most likely to be achieved in

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)