Exam 13: Segment and Interim Reporting

Exam 7: Intercompany Transfers of Services and Noncurrent Assets47 Questions

Exam 8: Intercompany Indebtedness39 Questions

Exam 8: Appendix a Intercompany Indebtedness40 Questions

Exam 9: Consolidation Ownership Issues51 Questions

Exam 10: Additional Consolidation Reporting Issues44 Questions

Exam 11: Multinational Accounting: Foreign Currency Transactions and Financial Instruments62 Questions

Exam 12: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements65 Questions

Exam 13: Segment and Interim Reporting61 Questions

Exam 14: Sec Reporting49 Questions

Exam 15: Partnerships: Formation, Operation, and Changes in Membership55 Questions

Exam 16: Partnerships: Liquidation59 Questions

Exam 17: Governmental Entities: Introduction and General Fund Accounting79 Questions

Exam 18: Governmental Entities: Special Funds and Governmentwide Financial Statements79 Questions

Exam 19: Not-For-Profit Entities121 Questions

Exam 20: Corporations in Financial Difficulty41 Questions

Select questions type

Davis Company uses LIFO for all of its inventories. During its second quarter of 20X9, Davis experienced a LIFO liquidation. Davis fully expects to replace the liquidated inventory in the early part of the third quarter. How should Davis report the inventory temporarily liquidated on its income statement for the second quarter?

(Multiple Choice)

4.9/5  (32)

(32)

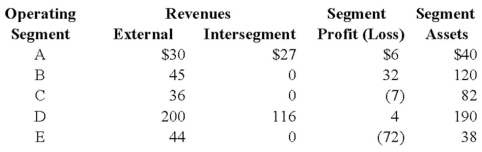

An analysis of Abbey Company's operating segments provides the following information:  Refer to the above information. Which of the operating segments above meet the operating profit (loss) test?

Refer to the above information. Which of the operating segments above meet the operating profit (loss) test?

(Multiple Choice)

4.7/5 (39)

Trevor Company discloses supplementary operating segment information for its three reportable segments. Data for 20X8 are available as follows:  Additional 20X8 expenses include indirect operating expenses of $200,000. Appropriately selected common indirect operating expenses are allocated to segments based on the ratio of each segment's sales to total sales. The 20X8 operating profit for Segment B was:

Additional 20X8 expenses include indirect operating expenses of $200,000. Appropriately selected common indirect operating expenses are allocated to segments based on the ratio of each segment's sales to total sales. The 20X8 operating profit for Segment B was:

(Multiple Choice)

4.9/5 (39)

Note: This is a Kaplan CPA Review Question

Reportable segments are not required to disclose which of the following:

(Multiple Choice)

4.8/5 (36)

ASC 280 requires certain disclosures about major customers. All of the following statements about those disclosures are true with the exception of which statement?

(Multiple Choice)

4.8/5 (34)

Wakefield Company uses a perpetual inventory system. In August, it sold 2,000 units from its LIFO-base inventory, which had originally cost $35 per unit. The replacement cost is expected to be $45 per unit. The company is planning to reduce its inventory and expects to replace only 1,500 of these units by December 31, the end of its fiscal year. The company replaced 1,500 units in November at an actual cost of $50 per unit.

Based on the preceding information, in the entry to record the replacement of the 1,500 units in November, Inventory will be debited for:

(Multiple Choice)

4.9/5 (34)

How would a company report a change in an accounting principle made on the last day of the third quarter?

(Multiple Choice)

4.8/5 (32)

Note: This is a Kaplan CPA Review Question

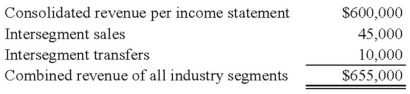

Grum Corp., a publicly-owned corporation, is subject to the requirements for segment reporting. In its income statement for the year ended December 31st, Grum reported consolidated revenues of $50,000,000, operating expenses of $47,000,000, and net income of $3,000,000. Operating expenses include payroll costs of $15,000,000. Grum's combined identifiable assets of all industry segments at December 31st, were $40,000,000. In its year-end financial statements, Grum would be most likely to disclose major customer data if sales to any single customer amounted to at least:

(Multiple Choice)

5.0/5 (46)

All of the following are differences between international standards and U.S. GAAP regarding operating segments, except:

(Multiple Choice)

4.8/5 (40)

ASC 280, Disclosure about Segments of an Enterprise and Related Information, has taken what has been referred to as a "management approach" to the definition of a segment and the allocation of costs to a segment.

Required:

a) What is meant by a management approach? How does this concept of a management approach impact the decision to disclose information?

b) How are decisions about cost allocation handled in segment disclosures?

(Essay)

4.8/5 (39)

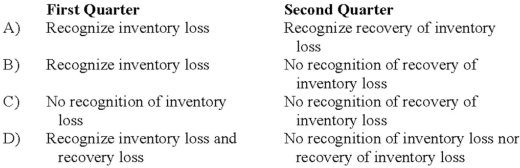

Tyler Company incurred an inventory loss due to a decline in market prices during its first quarter of operations in 20X8. At the end of the first quarter, management of the company believed the decline in market prices to be permanent. In the second quarter, the market prices of Tyler's inventories increased above their acquisition cost. Market prices remained higher than acquisition cost during the remainder of 20X8. How should Tyler report the facts above on its first and second quarter income statements?

(Multiple Choice)

4.9/5 (45)

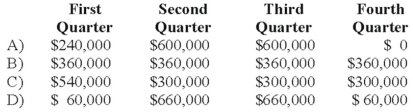

Mason Company paid its annual property taxes of $240,000 on February 15, 20X9. Mason also anticipates that its annual repairs expense for 20X9 will be $1,200,000. This amount is usually incurred and paid in July and August when operations are shut down so that machinery and equipment can be repaired. What amount should Mason deduct for property taxes and repairs in each quarter for 20X9?

(Multiple Choice)

4.7/5 (29)

Note: This is a Kaplan CPA Review Question

Which of the following characteristics would render the operating unit "reportable"? The operating unit comprises at least:

(Multiple Choice)

4.7/5 (36)

Note: This is a Kaplan CPA Review Question

The following information pertains to Aria Co. (Aria) and its operating segments for the year ended December 31, 20X6:

Sales to unaffiliated customers $2,000,000

Intersegment sales of products $600,000

Interest earned on loans to other industry segments $40,000

Aria and all its divisions are engaged solely in manufacturing operations. Aria evaluates divisional performance based on controllable contribution by segments. Aria has a reportable segment if that segment's revenue exceeds:

(Multiple Choice)

4.9/5 (29)

Trimester Corporation's revenue for the year ended December 31, 20X8, was as follows:  Trimester has a reportable operating segment if that segment's revenue exceeds:

Trimester has a reportable operating segment if that segment's revenue exceeds:

(Multiple Choice)

5.0/5 (43)

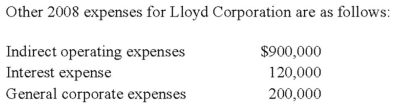

Lloyd Corporation reports the following information for 20X8 for its three operating segments:

Indirect operating expenses are allocated to segments based upon the ratio of each segment's traceable operating expenses to total traceable operating expenses. Interest expense is allocated to segments based upon the ratio of each segment's sales to total sales.

Required:

a) Calculate the operating profit or loss for each of the segments for 20X8.

b) Determine which segments are reportable, applying the operating profit or loss test.

Indirect operating expenses are allocated to segments based upon the ratio of each segment's traceable operating expenses to total traceable operating expenses. Interest expense is allocated to segments based upon the ratio of each segment's sales to total sales.

Required:

a) Calculate the operating profit or loss for each of the segments for 20X8.

b) Determine which segments are reportable, applying the operating profit or loss test.

(Essay)

4.9/5 (35)

Note: This is a Kaplan CPA Review Question

The following information pertains to revenue earned by Timm Co.'s industry segments for the year ended December 31st:  In conformity with the revenue test, Timm's reportable segments were

In conformity with the revenue test, Timm's reportable segments were

(Multiple Choice)

4.9/5 (37)

Iona Corporation is in the process of preparing its financial statements for the first quarter of 20X9 and has asked your advice as to how to report several items. These items include the following events which took place during the first quarter of 20X9 (assume all amounts are material):

1) Iona redeemed bonds with a carrying value of $4,000,000 at a cost of $3,760,000. This early extinguishment occurred because Iona wants to issue new debt at lower interest rates.

2) Iona uses the LIFO method for its inventories. On January 1, 20X9, inventories amounted to $10,000,000, while, on March 31, 20X9, inventories totaled $9,200,000. Iona expects to replace the liquidated inventory at the beginning of the second quarter at a cost of $1,000,000.

3) Iona changed its depreciation method on $4,000,000 of its delivery trucks from the declining balance method to the straight-line method. On January 1, 20X9, accumulated depreciation under the declining balance method was $2,800,000. Had the straight-line method been used, accumulated depreciation on January 1, 20X9, would have been $2,300,000. The remaining life of the trucks is two years.

4) Iona pays its top executives a bonus at year-end of 6 percent of operating income before bonus and income taxes. Operating income before bonus and income taxes for the three months ended March 31, 20X9, was $10,000,000. Iona estimates that its yearly operating income before bonus and income taxes will be $60,000,000.

5) Iona closes its manufacturing operations in July of each year in order to make its major annual repairs. Iona estimates that the cost of these repairs in 20X9 will be $1,000,000.

Required:

For each of the events numbered 1 through 5, indicate how that event should be reported on Iona's income statement for the three months ended March 31, 20X9, and the balance sheet accounts effects at March 31, 20X9. Ignore income taxes.

(Essay)

4.9/5 (38)

During the third quarter of 20X8, Pride Company sold a piece of equipment at an $8,000 gain. What portion of the gain should Pride report in its income statement for the third quarter of 20X8?

(Multiple Choice)

4.9/5 (30)

Which of the following are established by ASC 280 as "enterprisewide disclosure" standards to provide more information about the risks to a company?

I. Information about dominant industry segments.

II. Information about major customers.

III. Information about geographic areas

(Multiple Choice)

4.9/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)