Exam 26: Scarcity and Choice Neoclassical View

Exam 1: Prehistoric Communal Institutions in the Middle East46 Questions

Exam 2: Communal Equality to Slavery in the Middle East44 Questions

Exam 3: Slavery to Feudalism in Western Europe23 Questions

Exam 4: Feudalism and Paternalism in England30 Questions

Exam 5: Feudalism to Capitalism in England43 Questions

Exam 6: Mercantilism in England37 Questions

Exam 7: Pre-Capitalism to Industrial Capitalism in the United States 1776-186542 Questions

Exam 8: Classical Liberalism Defense of Industrial Capitalism27 Questions

Exam 9: Socialist Protest Against Industrial Capitalism27 Questions

Exam 10: Marx Critique and Alternative to Capitalism51 Questions

Exam 11: Rise of Corporate Capitalism in the United States, 1865-190035 Questions

Exam 12: Neoclassical Economics Defense of Corporate Capitalism23 Questions

Exam 13: Veblen Critique of Corporate Capitalism39 Questions

Exam 14: Growth and Depression in the United States, 1900-194038 Questions

Exam 15: Keynesian Economics and the Great Depression21 Questions

Exam 16: The United States and Global Capitalism, 1940-200659 Questions

Exam 17: Robinson Crusoe Two Perspectives on Microeconomics24 Questions

Exam 18: The Two Americas Inequality, Class, and Conflict26 Questions

Exam 19: Inequality, Exploitation, and Economic Institutions38 Questions

Exam 20: Prices, Profits, and Exploitation36 Questions

Exam 21: Market Power and Global Corporations33 Questions

Exam 22: Economics of Racial and Gender Discrimination28 Questions

Exam 23: Environmental Devastation31 Questions

Exam 24: Government and Inequality40 Questions

Exam 25: Economic Democracy33 Questions

Exam 26: Scarcity and Choice Neoclassical View59 Questions

Exam 27: Simple Analytics of Supply and Demand100 Questions

Exam 28: Consumption Theory: Demand39 Questions

Exam 29: Production Theory Supply50 Questions

Exam 30: Costs of Production46 Questions

Exam 31: Work and Wages Neoclassical View of Income Distribution53 Questions

Exam 32: Prices and Profits in Perfect Competition30 Questions

Exam 33: Monopoly, Power, Prices, and Profits27 Questions

Exam 34: Monopolistic Competition and Oligopoly21 Questions

Exam 35: Market Failures Public Goods, Market Power, and Externalities46 Questions

Exam 36: History of Business Cycles and Human Misery25 Questions

Exam 37: National Income Accounting How to Map the Circulation of Money and Goods42 Questions

Exam 38: Money and Profit Says Law and Institutionalist Criticism23 Questions

Exam 39: Neoclassical View of Aggregate Supply and Demand21 Questions

Exam 40: Keynesian View of Aggregate Supply and Demand28 Questions

Exam 41: How to Measure Instability26 Questions

Exam 42: Consumer Spending and Labor Income31 Questions

Exam 43: Investment Spending and Profit22 Questions

Exam 44: The Multiplier27 Questions

Exam 45: Business Cycles and Unemployment33 Questions

Exam 46: Growth and Waste32 Questions

Exam 47: Fiscal Policy45 Questions

Exam 48: Government Spending and Taxes18 Questions

Exam 49: Money, Banking, and Credit42 Questions

Exam 50: Inflation36 Questions

Exam 51: Monetary Policy39 Questions

Exam 52: Exports and Imports19 Questions

Exam 53: International Trade, Investment, and Finance How Instability Spreads Around the World19 Questions

Exam 54: Debate on Globalization24 Questions

Exam 55: Debate on Free Trade51 Questions

Exam 56: Development32 Questions

Select questions type

Explain why and how changes in technology, resources, and institutions influence the PPC.

-What would cause a parallel shift in a PPC? What would cause a change in its slope?

Free

(Essay)

4.9/5  (41)

(41)

Correct Answer: Verified

Verified

A parallel shift in a PPC reflects an equal increase in resources used in the production of both goods A change in slope would result from a greater gain in the resources used for the production of one good compared to the second good

Describe what progressive economists see as the primary shortcomings of the neoclassical scarcity perspective.

-Why is the context in which individuals make decisions important? How do social and cultural norms play into how individuals make decisions? Give an example of how a social norm may influence an economic decision.

Free

(Essay)

4.8/5 (34)

Correct Answer:Verified

Few decisions are made in isolation People often make decisions based on reasons other than self-interest, and sometimes these choices are made without carefully weighing the costs and benefits of a decision

Describe what progressive economists see as the primary shortcomings of the neoclassical scarcity perspective.

-What is the progressive criticism of the analysis of the economy, starting with isolated individuals? What is the critique of the assumptions about individuals and how individuals make decisions? What is the progressive alternative?

Free

(Essay)

4.8/5 (30)

Correct Answer:Verified

The assumption of isolated individuals does not describe life in a highly complex society in which every individual is tied to other individuals within the context of social and cultural norms, laws, and relationships

Describe how the production possibilities curve captures production choices in a society.

-If a society is producing on the frontier, what happens if society decides it wants more of one of the goods being produced?

(Short Answer)

4.8/5 (33)

Use the PPC to illustrate scarcity, choice, constant opportunity costs, and the law of increasing marginal opportunity cost.

-What does it mean when PPCs are illustrated with a straight line?

(Short Answer)

5.0/5 (44)

Which of the following would fall into the category of "resources?"

(Multiple Choice)

4.9/5 (34)

Describe what progressive economists see as the primary shortcomings of the neoclassical scarcity perspective.

-A progressive economist would claim we should not assume a market economy is always producing on the PPC. Explain. What does this mean about the decision to produce additional amounts of one good? Both goods?

(Essay)

4.8/5 (37)

Explain why and how changes in technology, resources, and institutions influence the PPC.

-What kind of institutional changes could cause an increase in production even though no other inputs increased and no technology changed?

(Essay)

4.9/5 (38)

List the assumptions behind the PPC

-What do we assume about inputs, institutions, and technology in building the PPC?

(Essay)

5.0/5 (33)

Use the PPC to illustrate scarcity, choice, constant opportunity costs, and the law of increasing marginal opportunity cost.

-Why are typical textbook PPCs bowed outward?

(Short Answer)

4.9/5 (36)

Explain why and how changes in technology, resources, and institutions influence the PPC.

-Give an example of how a change in technology might have an effect on the production of one good and not the other, and illustrate this situation with a PPC. What changed in the graph?

(Essay)

4.7/5 (38)

List the assumptions behind the PPC

-What does marginal cost mean? Create an example of a marginal cost.

(Short Answer)

4.7/5 (35)

Describe how the production possibilities curve captures production choices in a society.

-What does it mean if a society is producing on the frontier or directly on the PPC?

(Essay)

4.9/5 (40)

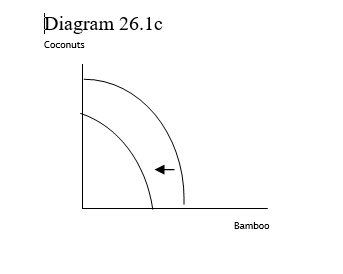

-The shift in the production possibilities curve shown in Diagram 26.1c reflects

-The shift in the production possibilities curve shown in Diagram 26.1c reflects

(Multiple Choice)

4.8/5 (38)

What is the attitude of neoclassical economists toward scarcity?

(Multiple Choice)

4.8/5 (36)

What do progressive economists mean by the term, "institutions?"

(Multiple Choice)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)