Exam 13: Components; Interim Reports; Reporting for the Sec

Exam 1: Ethical Issues in Advanced Accounting33 Questions

Exam 2: Partnerships: Organization and Operation39 Questions

Exam 3: Partnership Liquidation and Incorporation; Joint Ventures40 Questions

Exam 4: Accounting for Branches; Combined Financial Statements39 Questions

Exam 5: Business Combinations25 Questions

Exam 6: Consolidated Financial Statements: on Date of Business Combination39 Questions

Exam 7: Consolidated Financial Statements: Subsequent to Date of Business Combination39 Questions

Exam 8: Consolidated Financial Statements: Intercompany Transactions49 Questions

Exam 9: Consolidated Financial Statements: Income Taxes, Cash Flows, and Installment Acquisitions31 Questions

Exam 10: Consolidated Financial Statements: Special Problems29 Questions

Exam 11: International Accounting Standards; Accounting for Foreign Currency Transactions24 Questions

Exam 12: Translation of Foreign Currency Financial Statements20 Questions

Exam 13: Components; Interim Reports; Reporting for the Sec40 Questions

Exam 14: Bankruptcy: Liquidation and Reorganization30 Questions

Exam 15: Estates and Trusts39 Questions

Exam 16: Nonprofit Organizations35 Questions

Exam 17: Governmental Entities: General Fund34 Questions

Exam 18: Governmental Entities: Other Governmental Funds and Account Groups31 Questions

Exam 19: Governmental Entities: Proprietary Funds, Fiduciary Funds, and Comprehensive Annual Financial Report29 Questions

Select questions type

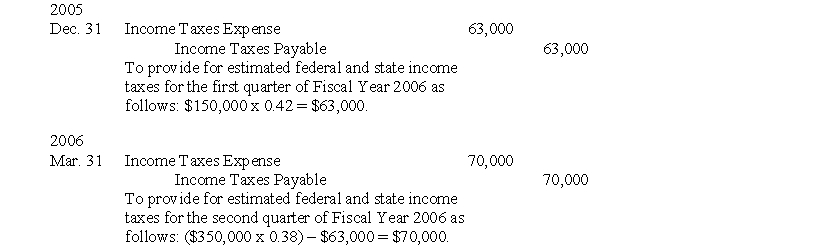

On October 1, 2005, Anaconda Company estimated an effective income tax rate of 42% for the fiscal year ending September 30, 2006. On January 2, 2006, Anaconda changed the estimate to 38%. Pre-tax financial income for Anaconda for the first two quarters of the fiscal year ending September 30, 2006, was as follows:

Prepare journal entries for income taxes expense for Anaconda Company on December 31, 2005, and March 31, 2006. Show supporting computations in explanations for the journal entries.

Prepare journal entries for income taxes expense for Anaconda Company on December 31, 2005, and March 31, 2006. Show supporting computations in explanations for the journal entries.

Free

(Essay)

4.8/5  (39)

(39)

Correct Answer: Verified

Verified

Which of the following SEC requirements generally does not appear in an annual report to stockholders?

Free

(Multiple Choice)

4.8/5 (39)

Correct Answer:Verified

B

For interim reports, an inventory loss from a temporary market decline in the first quarter, which may reasonably be expected to be restored in the fourth quarter, is:

Free

(Multiple Choice)

4.8/5 (34)

Correct Answer:Verified

C

To disclose a recent business combination, a company subject to the jurisdiction of the Securities and Exchange Commission (SEC) reports to the SEC in a:

(Multiple Choice)

4.9/5 (29)

Which of the following is not used as a basis for allocating among interim accounting periods an enterprise's costs and expenses other than product costs?

(Multiple Choice)

4.8/5 (34)

Do the disclosures related to segment profit or loss required by FASB Statement No. 131, "Disclosures about Segments . . . ,"include:

(Multiple Choice)

4.7/5 (32)

FASB Statement No. 131, "Disclosures about Segments . . . ," includes a concept of segment reporting termed the:

(Multiple Choice)

4.8/5 (40)

The computation of a business enterprise's third-quarter income taxes expense should be based on pre-tax financial income:

(Multiple Choice)

4.7/5 (35)

Methods that have been used to allocate nontraceable expenses to segments include all the following ratios except:

(Multiple Choice)

4.8/5 (39)

In its interim report for the three months ended January 31, 2006, the first quarter of its fiscal year ending October 31, 2006, Wister Company had income taxes expense of $52,800 ($100,000 x 0.528). On April 30, 2006, Wister estimated that its effective income tax rate for the year ending October 31, 2006, would be 50.9%. If Wister's pre-tax financial income for the three months ended April 30, 2006, was $110,000, Wister's income taxes expense for the three months ended April 30, 2006, is:

(Multiple Choice)

4.7/5 (36)

A company may issue a Form 8-K to the SEC for an event that it is not required legally to report to the SEC but that it considers to be important to its stockholders.

(True/False)

4.7/5 (38)

The Securities Act of 1933 governs interstate issuances of securities to the public.

(True/False)

4.9/5 (38)

In Section 101 of Codification of Financial Reporting Policies, the Securities and Exchange Commission indicated that it would concentrate on pronouncements on disclosures in reports filed by enterprises subject to its jurisdiction, leaving the establishment of financial accounting standards to the Financial Accounting Standards Board.

In your opinion, has the SEC adhered to the policy stated above? Explain.

(Essay)

4.8/5 (40)

Both Regulation S-K and Regulation S-X deal with the form and content of financial statements filed with the SEC.

(True/False)

4.8/5 (28)

Under FASB Statement No. 131, "Disclosures about Segments . . . ," segment profit or loss is measured by:

(Multiple Choice)

4.8/5 (33)

Zero Company had three business segments. Because Garson Segment had been operating at a pre-tax loss during Fiscal Year 2006, Zero accepted an offer to sell the net assets of Garson Segment, which had a carrying amount of $400,000 on October 31, 2006, the end of the fiscal year, to Thrice Company (an unrelated business enterprise) for $340,000 on November 30, 2006. Garson Segment was expected to operate at a loss (before income tax considerations) of $40,000 during the month of November, 2006. Zero's income tax rate is 40%.

Prepare a working paper to compute the loss on the disposal of Garson Segment to be displayed in Zero Company's income statement for the fiscal year ended October 31, 2006.

(Essay)

4.8/5 (43)

In FASB Statement No. 131, "Disclosures about Segments . . . ," the FASB provided accounting standards for allocating nontraceable expenses to segments.

(True/False)

4.8/5 (38)

In APB Opinion No. 28, "Interim Financial Reporting," the Accounting Principles Board adopted the viewpoint that interim accounting periods are to be accounted for as integral parts of the annual accounting period.

(True/False)

4.8/5 (46)

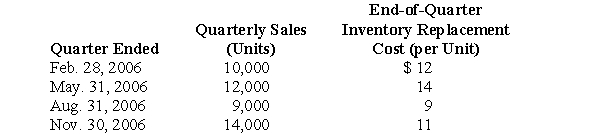

Selected quarterly data for Canby Company were as follows for the fiscal year ended November 30, 2006:  Canby purchased no merchandise during the year ended November 30, 2006. The first-in, first-out cost of its November 30, 2005, inventory of 50,000 units was $500,000.

If the market decline in the quarter ended August 31, 2006, was not considered to be temporary, Canby's cost of goods sold for that quarter is:

Canby purchased no merchandise during the year ended November 30, 2006. The first-in, first-out cost of its November 30, 2005, inventory of 50,000 units was $500,000.

If the market decline in the quarter ended August 31, 2006, was not considered to be temporary, Canby's cost of goods sold for that quarter is:

(Multiple Choice)

4.9/5 (32)

The Forms and proxy statements filed with the SEC are reviewed by the SEC's:

(Multiple Choice)

5.0/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)