Exam 5: Business Combinations

Exam 1: Ethical Issues in Advanced Accounting33 Questions

Exam 2: Partnerships: Organization and Operation39 Questions

Exam 3: Partnership Liquidation and Incorporation; Joint Ventures40 Questions

Exam 4: Accounting for Branches; Combined Financial Statements39 Questions

Exam 5: Business Combinations25 Questions

Exam 6: Consolidated Financial Statements: on Date of Business Combination39 Questions

Exam 7: Consolidated Financial Statements: Subsequent to Date of Business Combination39 Questions

Exam 8: Consolidated Financial Statements: Intercompany Transactions49 Questions

Exam 9: Consolidated Financial Statements: Income Taxes, Cash Flows, and Installment Acquisitions31 Questions

Exam 10: Consolidated Financial Statements: Special Problems29 Questions

Exam 11: International Accounting Standards; Accounting for Foreign Currency Transactions24 Questions

Exam 12: Translation of Foreign Currency Financial Statements20 Questions

Exam 13: Components; Interim Reports; Reporting for the Sec40 Questions

Exam 14: Bankruptcy: Liquidation and Reorganization30 Questions

Exam 15: Estates and Trusts39 Questions

Exam 16: Nonprofit Organizations35 Questions

Exam 17: Governmental Entities: General Fund34 Questions

Exam 18: Governmental Entities: Other Governmental Funds and Account Groups31 Questions

Exam 19: Governmental Entities: Proprietary Funds, Fiduciary Funds, and Comprehensive Annual Financial Report29 Questions

Select questions type

Slocum Corporation and Merton Company, both publicly owned companies, are planning a merger, with Slocum being the survivor. Which of the following is a requirement of the merger?

Free

(Multiple Choice)

4.9/5  (36)

(36)

Correct Answer: Verified

Verified

D

In a statutory merger, all except one of the constituent companies are liquidated.

Free

(True/False)

4.7/5 (34)

Correct Answer:Verified

True

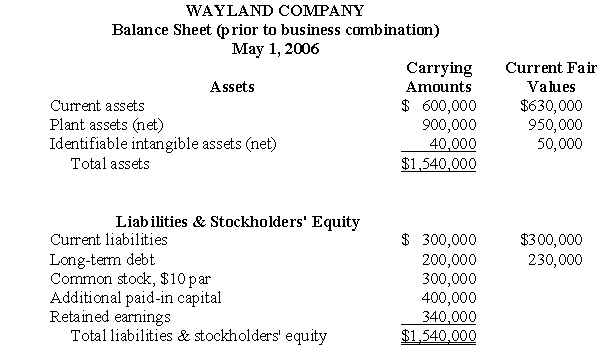

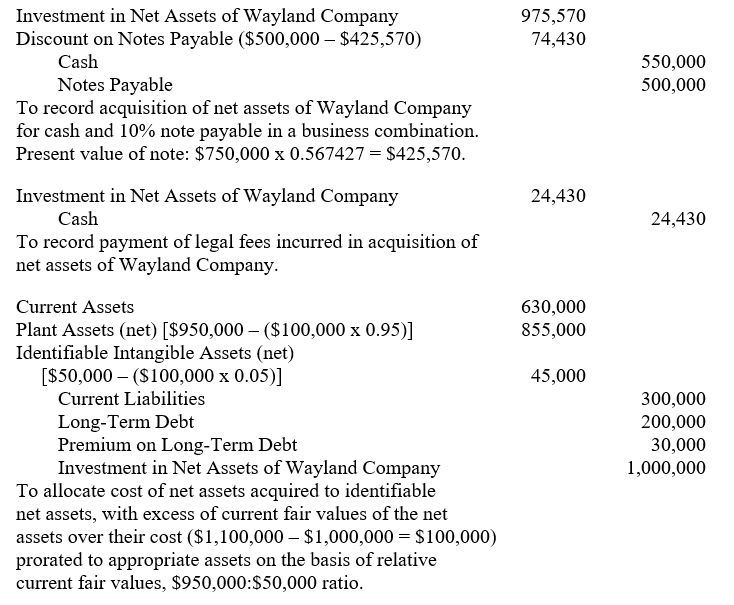

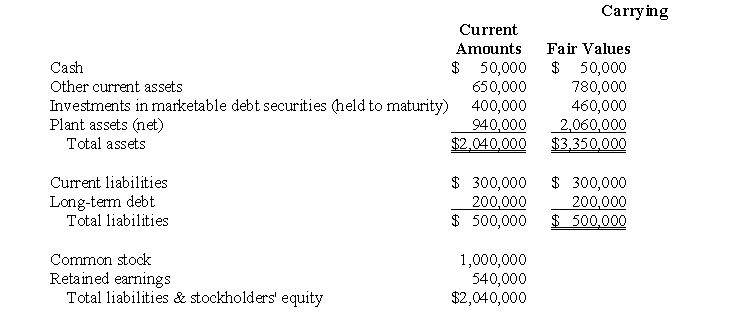

On May 1, 2006, Regis Corporation acquired all the net assets of Wayland Company for $550,000 cash and a $500,000, 10% promissory note due May 1, 2011. The total interest of $250,000 also was due on May 1, 2008. The current fair rate of interest for the promissory note was 12%. The balance sheet of Wayland and the related current fair values of its identifiable assets and liabilities on the date of the business combination follow:

Legal fees of $24,430 incurred by Regis to effect the business combination were paid by Regis on May 1, 2006. The present value of 1 due in five years at 12% is 0.567427.

Prepare journal entries on May 1, 2006, to record Regis Corporation's acquisition of the net assets of Wayland Company. Disregard income taxes.

Legal fees of $24,430 incurred by Regis to effect the business combination were paid by Regis on May 1, 2006. The present value of 1 due in five years at 12% is 0.567427.

Prepare journal entries on May 1, 2006, to record Regis Corporation's acquisition of the net assets of Wayland Company. Disregard income taxes.

Free

(Essay)

4.9/5 (39)

Correct Answer:Verified

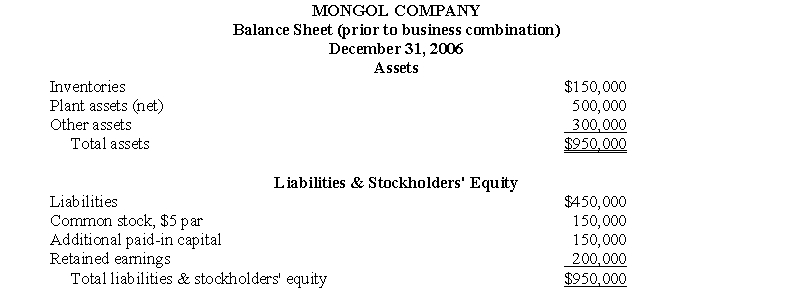

The balance sheet of Mongol Company on December 31, 2006, prior to its merger with Solway Corporation, was as follows:

On December 31, 2006, Solway issued 60,000 of its $10 par (current fair value $15) common stock for all the outstanding common stock of Mongol, which was then liquidated. Also on December 31, 2006, Solway paid $60,000 out-of-pocket costs in connection with the business combination, of which $25,000 were finder's, accounting, and legal fees directly related to the combination, and $35,000 were costs of registering and issuing the common stock to effect the combination. Current fair values of Mongol's inventories and plant assets were $180,000 and $620,000, respectively; other assets and liabilities had current fair values equal to their carrying amounts.

Prepare journal entries on December 31, 2006, for Solway Corporation to record the business combination with Mongol Company. Disregard income taxes.

On December 31, 2006, Solway issued 60,000 of its $10 par (current fair value $15) common stock for all the outstanding common stock of Mongol, which was then liquidated. Also on December 31, 2006, Solway paid $60,000 out-of-pocket costs in connection with the business combination, of which $25,000 were finder's, accounting, and legal fees directly related to the combination, and $35,000 were costs of registering and issuing the common stock to effect the combination. Current fair values of Mongol's inventories and plant assets were $180,000 and $620,000, respectively; other assets and liabilities had current fair values equal to their carrying amounts.

Prepare journal entries on December 31, 2006, for Solway Corporation to record the business combination with Mongol Company. Disregard income taxes.

(Essay)

4.9/5 (42)

Paragraph 43 of FASB Statement No. 141, "Business Combination," reads in part as follows:

The excess of the cost of an acquired entity over the net of the amounts assigned to assets acquired and liabilities assumed shall be recognized as an asset referred to as goodwill.

What deficiencies, if any, do you perceive in the foregoing definition of goodwill? Explain.

(Essay)

4.7/5 (34)

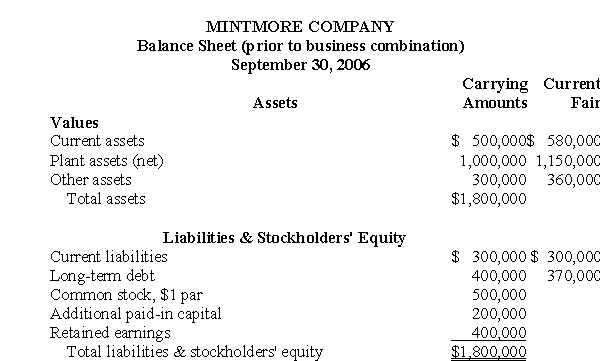

The balance sheet of Mintmore Company on September 30, 2006, with related current fair values for assets and liabilities, is shown as follows:

On September 30, 2006, Spooner Corporation paid $1,560,000 to Mintmore Company for all the Mintmore assets except its cash of $50,000, and assumed all liabilities of Mintmore, in a business combination that had been approved by the boards of directors and stockholders of both companies. Also on September 30, 2006, Spooner paid legal fees of $20,000 incurred to implement the business combination.

Prepare journal entries for Spooner Corporation on September 30, 2006, to record the business combination with Mintmore Company. Disregard income taxes.

On September 30, 2006, Spooner Corporation paid $1,560,000 to Mintmore Company for all the Mintmore assets except its cash of $50,000, and assumed all liabilities of Mintmore, in a business combination that had been approved by the boards of directors and stockholders of both companies. Also on September 30, 2006, Spooner paid legal fees of $20,000 incurred to implement the business combination.

Prepare journal entries for Spooner Corporation on September 30, 2006, to record the business combination with Mintmore Company. Disregard income taxes.

(Essay)

4.8/5 (38)

A bargain purchase excess in a business combination is credited to the Paid-in Capital in Excess of Par ledger account of the combined enterprise.

(True/False)

4.7/5 (46)

The issuer of common stock in a business combination always is the combinor.

(True/False)

4.8/5 (41)

In a business combination, the appropriate accounting for an excess of current fair values the combinee's identifiable net assets over the combinor's cost is to:

(Multiple Choice)

4.8/5 (44)

Carrying amounts of the combinee's identifiable net assets are disregarded in accounting for a business combination.

(True/False)

4.8/5 (35)

Direct out-of-pocket costs of a business combination that are part of the cost of the combinee do not include:

(Multiple Choice)

4.7/5 (42)

Two methods for arranging business combinations that begin with similar transactions by the combinor are:

(Multiple Choice)

4.7/5 (32)

A combinee in a business combination may have preacquisition contingencies to which a value is assigned during the allocation period.

(True/False)

4.8/5 (38)

Subsequent to the date of a business combination, is goodwill recognized in the combination subject to:

(Multiple Choice)

4.8/5 (40)

The defense against a hostile takeover known as a poison pill involves the amendment of the target company's articles of incorporation or bylaws to make it more difficult to obtain stockholder approval for a takeover.

(True/False)

4.7/5 (36)

A business combination may be effected through the combinor's tender offer for the combinee's common stock.

(True/False)

4.9/5 (34)

All out-of-pocket costs of a business combination are recognized as expenses by the combinor.

(True/False)

4.9/5 (29)

On March 1, 2006, Selig Corporation acquired for $1,400,000 (including out-of-pocket costs of the business combination) all the net assets of Maree Company. On the date of the combination, the carrying amount of Maree's identifiable net assets was $1,150,000. The current fair value of Maree's inventories was $200,000 less than their carrying amount, and the current fair value of Maree's plant assets was $400,000 larger than their carrying amount. The current fair values of all other identifiable net assets of Maree were equal to their carrying amounts. The journal entry prepared by Selig to record the business combination includes:

(Multiple Choice)

4.8/5 (35)

Goodwill acquired in a business combination is amortized over its economic life.

(True/False)

4.8/5 (33)

On May 31, 2006, Combinor Corporation issued $4,000,000 face amount of 20-year, 16% bonds to yield 20%, interest payable each May 31 and November 30, for all the net assets of Combinee Company. Also on May 31, 2006, Combinor paid the following out-of-pocket costs in connection with the combination:

The separate balance sheet of Combinee on May 31, 2006, prior to the business combination included the following:

The separate balance sheet of Combinee on May 31, 2006, prior to the business combination included the following:

Prepare journal entries for Combinor Corporation on May 31, 2006, to record the business combination with Combinee Company. Appropriate present value factors are as follows:

Prepare journal entries for Combinor Corporation on May 31, 2006, to record the business combination with Combinee Company. Appropriate present value factors are as follows:

(Essay)

4.7/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)