Exam 13: Components; Interim Reports; Reporting for the Sec

Exam 1: Ethical Issues in Advanced Accounting33 Questions

Exam 2: Partnerships: Organization and Operation39 Questions

Exam 3: Partnership Liquidation and Incorporation; Joint Ventures40 Questions

Exam 4: Accounting for Branches; Combined Financial Statements39 Questions

Exam 5: Business Combinations25 Questions

Exam 6: Consolidated Financial Statements: on Date of Business Combination39 Questions

Exam 7: Consolidated Financial Statements: Subsequent to Date of Business Combination39 Questions

Exam 8: Consolidated Financial Statements: Intercompany Transactions49 Questions

Exam 9: Consolidated Financial Statements: Income Taxes, Cash Flows, and Installment Acquisitions31 Questions

Exam 10: Consolidated Financial Statements: Special Problems29 Questions

Exam 11: International Accounting Standards; Accounting for Foreign Currency Transactions24 Questions

Exam 12: Translation of Foreign Currency Financial Statements20 Questions

Exam 13: Components; Interim Reports; Reporting for the Sec40 Questions

Exam 14: Bankruptcy: Liquidation and Reorganization30 Questions

Exam 15: Estates and Trusts39 Questions

Exam 16: Nonprofit Organizations35 Questions

Exam 17: Governmental Entities: General Fund34 Questions

Exam 18: Governmental Entities: Other Governmental Funds and Account Groups31 Questions

Exam 19: Governmental Entities: Proprietary Funds, Fiduciary Funds, and Comprehensive Annual Financial Report29 Questions

Select questions type

The standards established in FASB Statement No. 131, "Disclosures about Segments…," provide far less segment information to users of financial reports than was required by FASB Statement No. 14, "Financial Reporting for Segments of a Business Enterprise."

(True/False)

4.8/5  (40)

(40)

For the fiscal year ended June 30, 2006, Disc-Seg Company:

(1) Had income from continuing operations of $1,000,000 before income taxes

(2) Had no temporary differences between pre-tax financial income and taxable income

(3) Was subject to an income tax rate of 40%

(4) Disposed of an operating segment having net assets of $600,000 for $550,000 cash. For the period July 1, 2005, through the disposal date, the discontinued segment had a pre-tax operating loss of $140,000.

Prepare the bottom portion of Disc-Seg Company's income statement for the year ended June 30, 2006, beginning with income from continuing operations before income taxes. Disregard earnings per share data.

(Essay)

4.8/5 (36)

FASB Statement No. 131, "Disclosures about Segments . . . ," defined major customers of a segmented business enterprise as those who provide 15% or more of the enterprise's total revenues.

(True/False)

4.7/5 (36)

Which of the following is not required by APB Opinion No. 28, "Interim Financial Reporting," to be included in public companies' interim financial reports to stockholders?

(Multiple Choice)

4.8/5 (40)

Staff Accounting Bulletins issued by the SEC bear the SEC's official approval.

(True/False)

4.9/5 (44)

Management of a business enterprise has the responsibility for identifying the operating segments of the enterprise.

(True/False)

4.8/5 (35)

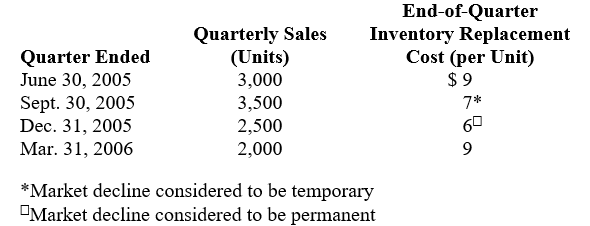

Wasco Company, which has a March 31 fiscal year, issues interim financial reports. Wasco sells a single unit of merchandise; the merchandise inventory, at first-in, first-out cost, was 14,000 units, $112,000, on April 1, 2005. Wasco purchased no merchandise during the year ended March 31, 2006. Quarterly sales and end-of-quarter merchandise replacement costs for the year ended March 31, 2006, were as follows:

Prepare a working paper to compute Wasco Company's cost of goods sold for the four quarters of the year ended March 31, 2006. Use the following headings:

Prepare a working paper to compute Wasco Company's cost of goods sold for the four quarters of the year ended March 31, 2006. Use the following headings:

(Essay)

4.8/5 (33)

The trading of securities on national securities exchanges and over the counter is governed by the Securities Act of 1933.

(True/False)

4.9/5 (34)

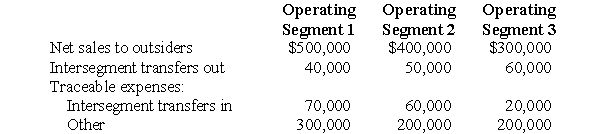

Switzer Company's accounting records for the fiscal year ended May 31, 2006, included the following information for its three operating segments:

Nontraceable expenses of Switzer were $120,000 for the year ended May 31, 2006. Switzer allocates these expenses on the basis of segment sales to outsiders.

Prepare a working paper to compute the profit or loss of each of Switzer's three operating segments for the year ended May 31, 2006.

Nontraceable expenses of Switzer were $120,000 for the year ended May 31, 2006. Switzer allocates these expenses on the basis of segment sales to outsiders.

Prepare a working paper to compute the profit or loss of each of Switzer's three operating segments for the year ended May 31, 2006.

(Essay)

4.8/5 (41)

The nontraceable expenses of Wick Company's corporate (home) office for 2006 amounted to $360,000. The net sales, payroll, and average plant assets and inventories for the two operating segments of Wick were as follows:

Prepare a working paper to compute the amount of corporate (home) office nontraceable expenses to be allocated to Alpha Segment, assuming that such expenses are allocated to the segments on the basis of the arithmetic average of the percentage of net sales, payroll, and average plant assets and inventories applicable to each segment.

Prepare a working paper to compute the amount of corporate (home) office nontraceable expenses to be allocated to Alpha Segment, assuming that such expenses are allocated to the segments on the basis of the arithmetic average of the percentage of net sales, payroll, and average plant assets and inventories applicable to each segment.

(Essay)

4.7/5 (40)

If an operating segment has been discontinued during the year, the gain or loss on disposal:

(Multiple Choice)

4.8/5 (36)

Chan Company's statutory income tax rate is 40%. Chan forecasted pre-tax income of $200,000 for 2006, with no temporary differences between financial income and taxable income. Chan forecasted the following permanent differences between financial income and taxable income for 2006: Dividend received deduction, $40,000; Premiums on officers' life insurance, $30,000.

Prepare a working paper to compute Chan Company's estimated effective income tax rate for 2006.

(Essay)

4.8/5 (43)

On April 30, 2006, Raye Company, which has a fiscal year ending September 30, adopted a plan to discontinue the operations of Bello Division, an operating segment, on November 30, 2006. Bello had contributed a major portion of Raye's sales volume. Raye estimated that Bello would sustain a loss of $460,000 from May 1, 2006, through September 30, 2006, and would sustain an additional loss of $220,000 from October 1, 2006, to November 30, 2006. Raye also estimated that it would realize a gain of $600,000 on the disposal of Bello's net assets. On September 30, 2006, Raye determined that Bello had an operating loss of $1,120,000 for the year ended that date, of which $420,000 represented the loss from May 1 to September 30, 2006.

Disregarding income tax effects, the amount that Raye reports in its September 30, 2006, income statement as gain or loss on disposal of Bello is:

(Multiple Choice)

4.8/5 (36)

If a new effective income tax rate is computed for the second quarter of a business enterprise's fiscal year, the new rate is applied retroactively to restate the income taxes expense for the first quarter of the fiscal year.

(True/False)

4.8/5 (42)

A Form 10-K Annual Report must be filed with the SEC within 60 days after the close of each fiscal year of a company subject to the Securities Exchange Act of 1934.

(True/False)

5.0/5 (33)

The gain or loss on disposal of an operating segment, including the results of operations of the discontinued segment, is reported separately as a component of income before extraordinary items.

(True/False)

4.7/5 (40)

FASB Statement No. 131, "Disclosures about Segments . . . ," replaced the term industry segment with operating segment.

(True/False)

4.7/5 (38)

Lower-of-cost-or-market write-downs of inventories must be provided for interim accounting periods unless the interim date market declines in inventories are considered to be temporary.

(True/False)

4.9/5 (46)

The gross margin method of estimating inventories may be used in the preparation of interim reports; however, the lower-of-cost-or-market rule may not be applied to inventory costs determined by the gross margin method.

(True/False)

4.9/5 (40)

The annual report filed with the SEC within 60 days after the close of each fiscal year is:

(Multiple Choice)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)