Exam 8: Flexible Budgets, Overhead Cost Variances, and Management Control

Exam 1: The Manager and Management Accounting195 Questions

Exam 2: An Introduction to Cost Terms and Purposes224 Questions

Exam 3: Cost-Volume-Profit Analysis211 Questions

Exam 4: Job Costing203 Questions

Exam 5: Activity-Based Costing and Activity-Based Management176 Questions

Exam 6: Master Budget and Responsibility Accounting226 Questions

Exam 7: Flexible Budgets, Direct-Cost Variances, and Management Control181 Questions

Exam 8: Flexible Budgets, Overhead Cost Variances, and Management Control176 Questions

Exam 9: Inventory Costing and Capacity Analysis210 Questions

Exam 10: Determining How Costs Behave192 Questions

Exam 11: Decision Making and Relevant Information218 Questions

Exam 12: Strategy, Balanced Scorecard, and Strategic Profitability Analysis172 Questions

Exam 13: Pricing Decisions and Cost Management210 Questions

Exam 14: Cost Allocation, Customer-Profitability Analysis, and Sales-Variance Analysis167 Questions

Exam 15: Allocation of Support-Department Costs, Common Costs, and Revenues150 Questions

Exam 16: Cost Allocation: Joint Products and Byproducts151 Questions

Exam 17: Process Costing149 Questions

Exam 18: Spoilage, Rework, and Scrap153 Questions

Exam 19: Balanced Scorecard: Quality and Time150 Questions

Exam 20: Inventory Management, Just-in-Time, and Simplified Costing Methods150 Questions

Exam 21: Capital Budgeting and Cost Analysis151 Questions

Exam 22: Management Control Systems, Transfer Pricing, and Multinational Considerations151 Questions

Exam 23: Performance Measurement, Compensation, and Multinational Considerations150 Questions

Select questions type

The accounting for 3-variance analysis is simpler than the 4-variance analysis, but some

information is lost because the variable and fixed overhead spending variances are combined

into a single total overhead spending variance.

(True/False)

4.9/5  (30)

(30)

List the four steps to develop budgeted variable overhead cost-allocation.

(Essay)

4.8/5 (34)

All of the following are possible causes of actual machine hours exceeding budgeted machine hours except:

(Multiple Choice)

4.9/5 (41)

The production-volume variance is a component of the sales-volume variance.

(True/False)

4.8/5 (35)

When fixed overhead spending variance is unfavorable, it can be safely assumed that ________.

(Multiple Choice)

4.9/5 (36)

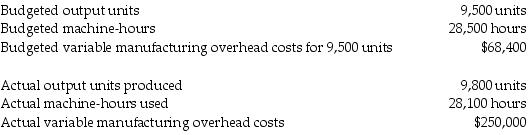

Lancelot Corporation manufactures tennis gear and uses budgeted machine-hours to allocate variable manufacturing overhead. The following information relates to the company's manufacturing overhead data:

What is the amount of the budgeted variable manufacturing overhead cost per unit?

What is the amount of the budgeted variable manufacturing overhead cost per unit?

(Multiple Choice)

4.9/5 (40)

The variable overhead efficiency variance measures the difference between the ________, multiplied by the budgeted variable overhead cost per unit of the cost-allocation base.

(Multiple Choice)

4.7/5 (36)

Lump-sum fixed costs of acquiring capacity decrease automatically if the capacity needed turns out to be less than the capacity acquired.

(True/False)

4.9/5 (39)

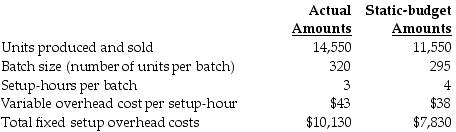

Raposa, Inc., produces a special line of plastic toy racing cars. Raposa, Inc., produces the cars in batches. To manufacture a batch of the cars, Raposa, Inc., must set up the machines and molds. Setup costs are batch-level costs because they are associated with batches rather than individual units of products. A separate Setup Department is responsible for setting up machines and molds for different styles of car.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to the number of setup-hours. The following information pertains to June 2015:

Calculate the spending variance for variable overhead setup costs. (Round all intermediary calculations two decimal places and your final answer to the nearest whole number.)

Calculate the spending variance for variable overhead setup costs. (Round all intermediary calculations two decimal places and your final answer to the nearest whole number.)

(Multiple Choice)

4.9/5 (33)

The variable overhead efficiency variance is computed ________ and interpreted ________ the direct-cost efficiency variance.

(Multiple Choice)

4.9/5 (36)

Davidson Corporation manufactured 53,400 units during September. The following fixed overhead data relates to September:

What is the fixed overhead spending variance?

What is the fixed overhead spending variance?

(Multiple Choice)

4.9/5 (44)

Radon Corporation manufactured 37,500 units during March. The following fixed overhead data pertain to March:

What is the fixed overhead production-volume variance?

What is the fixed overhead production-volume variance?

(Multiple Choice)

5.0/5 (40)

At the start of the budget period, management will have made most decisions regarding the level of fixed overhead costs to be incurred.

(True/False)

4.7/5 (41)

Hockey Accessories Corporation manufactured 21,400 duffle bags during March. The following fixed overhead data pertain to March:

What is the amount of fixed overhead spending variance?

What is the amount of fixed overhead spending variance?

(Multiple Choice)

4.7/5 (40)

Which of the following is the correct mathematical expression to calculate the fixed overhead production-volume variance?

(Multiple Choice)

4.8/5 (36)

An unfavorable price variance for materials-handling labor indicates that the actual cost per materials-handling labor-hour is less than the budgeted cost per materials-handling labor-hour.

(True/False)

4.8/5 (37)

The major challenge when planning fixed overhead is ________.

(Multiple Choice)

4.9/5 (39)

Service-sector companies have no use of variance analysis as only few costs can be traced to their outputs in a cost effective way.

(True/False)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)