Exam 15: The Term Structure of Interest Rates

Exam 1: The Investment Environment58 Questions

Exam 2: Asset Classes and Financial Instruments86 Questions

Exam 3: How Securities Are Traded69 Questions

Exam 4: Mutual Funds and Other Investment Companies72 Questions

Exam 5: Risk, Return, and the Historical Record85 Questions

Exam 6: Capital Allocation to Risky Assets70 Questions

Exam 7: Optimal Risky Portfolios80 Questions

Exam 8: Index Models87 Questions

Exam 9: The Capital Asset Pricing Model83 Questions

Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return80 Questions

Exam 11: The Efficient Market Hypothesis71 Questions

Exam 12: Behavioral Finance and Technical Analysis54 Questions

Exam 13: Empirical Evidence on Security Returns56 Questions

Exam 14: Bond Prices and Yields129 Questions

Exam 15: The Term Structure of Interest Rates49 Questions

Exam 16: Managing Bond Portfolios84 Questions

Exam 17: Macroeconomic and Industry Analysis90 Questions

Exam 18: Equity Valuation Models130 Questions

Exam 19: Financial Statement Analysis91 Questions

Exam 20: Options Markets: Introduction108 Questions

Exam 21: Option Valuation90 Questions

Exam 22: Futures Markets91 Questions

Exam 23: Futures, Swaps, and Risk Management56 Questions

Exam 24: Portfolio Performance Evaluation83 Questions

Exam 25: International Diversification52 Questions

Exam 26: Hedge Funds49 Questions

Exam 27: The Theory of Active Portfolio Management50 Questions

Exam 28: Investment Policy and the Framework of the Cfa Institute83 Questions

Select questions type

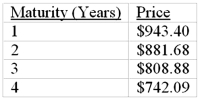

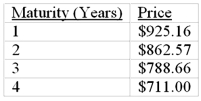

The following is a list of prices for zero-coupon bonds with different maturities and par value of $1,000.  What is, according to the expectations theory, the expected forward rate in the third year

What is, according to the expectations theory, the expected forward rate in the third year

Free

(Multiple Choice)

5.0/5  (43)

(43)

Correct Answer: Verified

Verified

C

The following is a list of prices for zero-coupon bonds with different maturities and par value of $1,000.  What is, according to the expectations theory, the expected forward rate in the third year

What is, according to the expectations theory, the expected forward rate in the third year

Free

(Multiple Choice)

4.9/5 (40)

Correct Answer:Verified

B

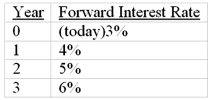

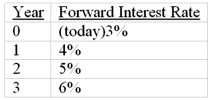

Suppose that all investors expect that interest rates for the 4 years will be as follows:  What is the price of a 2-year maturity bond with a 5% coupon rate paid annually (Par value = $1,000.)

What is the price of a 2-year maturity bond with a 5% coupon rate paid annually (Par value = $1,000.)

Free

(Multiple Choice)

4.7/5 (38)

Correct Answer:Verified

C

The "break-even" interest rate for year n that equates the return on an n-period zero-coupon bond to that of an n - 1 - period zero-coupon bond rolled over into a one-year bond in year n is defined as

(Multiple Choice)

4.8/5 (35)

Term Structure of Interest Rates is the relationship between what variables

What is assumed about other variables

How is term structure of interest rates depicted graphically

(Essay)

4.8/5 (35)

If the value of a Treasury bond was lower than the value of the sum of its parts (STRIPPED cash flows)

(Multiple Choice)

4.9/5 (31)

When computing yield to maturity, the implicit reinvestment assumption is that the interest payments are reinvested at the

(Multiple Choice)

4.9/5 (35)

Explain what the following terms mean: spot rate, short rate, and forward rate.Which of these is(are) observable today

(Essay)

4.8/5 (32)

Suppose that all investors expect that interest rates for the 4 years will be as follows:  If you have just purchased a 4-year zero-coupon bond, what would be the expected rate of return on your investment in the first year if the implied forward rates stay the same (Par value of the bond = $1,000)

If you have just purchased a 4-year zero-coupon bond, what would be the expected rate of return on your investment in the first year if the implied forward rates stay the same (Par value of the bond = $1,000)

(Multiple Choice)

4.9/5 (39)

Suppose that all investors expect that interest rates for the 4 years will be as follows:  What is the price of 3-year zero-coupon bond with a par value of $1,000

What is the price of 3-year zero-coupon bond with a par value of $1,000

(Multiple Choice)

4.8/5 (38)

If the value of a Treasury bond was higher than the value of the sum of its parts (STRIPPED cash flows) you could

(Multiple Choice)

4.8/5 (36)

Discuss the theories of the term structure of interest rates.Include in your discussion the differences in the theories, and the advantages/disadvantages of each.

(Essay)

4.7/5 (43)

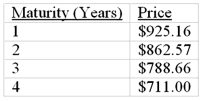

The following is a list of prices for zero-coupon bonds with different maturities and par value of $1,000.  What is the price of a 4-year maturity bond with a 10% coupon rate paid annually (Par value = $1,000.)

What is the price of a 4-year maturity bond with a 10% coupon rate paid annually (Par value = $1,000.)

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)