Exam 6: Capital Allocation to Risky Assets

Exam 1: The Investment Environment58 Questions

Exam 2: Asset Classes and Financial Instruments86 Questions

Exam 3: How Securities Are Traded69 Questions

Exam 4: Mutual Funds and Other Investment Companies72 Questions

Exam 5: Risk, Return, and the Historical Record85 Questions

Exam 6: Capital Allocation to Risky Assets70 Questions

Exam 7: Optimal Risky Portfolios80 Questions

Exam 8: Index Models87 Questions

Exam 9: The Capital Asset Pricing Model83 Questions

Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return80 Questions

Exam 11: The Efficient Market Hypothesis71 Questions

Exam 12: Behavioral Finance and Technical Analysis54 Questions

Exam 13: Empirical Evidence on Security Returns56 Questions

Exam 14: Bond Prices and Yields129 Questions

Exam 15: The Term Structure of Interest Rates49 Questions

Exam 16: Managing Bond Portfolios84 Questions

Exam 17: Macroeconomic and Industry Analysis90 Questions

Exam 18: Equity Valuation Models130 Questions

Exam 19: Financial Statement Analysis91 Questions

Exam 20: Options Markets: Introduction108 Questions

Exam 21: Option Valuation90 Questions

Exam 22: Futures Markets91 Questions

Exam 23: Futures, Swaps, and Risk Management56 Questions

Exam 24: Portfolio Performance Evaluation83 Questions

Exam 25: International Diversification52 Questions

Exam 26: Hedge Funds49 Questions

Exam 27: The Theory of Active Portfolio Management50 Questions

Exam 28: Investment Policy and the Framework of the Cfa Institute83 Questions

Select questions type

You invest $100 in a risky asset with an expected rate of return of 0.12 and a standard deviation of 0.15 and a T-bill with a rate of return of 0.05. What percentages of your money must be invested in the risk-free asset and the risky asset, respectively, to form a portfolio with a standard deviation of 0.06

Free

(Multiple Choice)

4.8/5  (40)

(40)

Correct Answer: Verified

Verified

C

You are considering investing $1,000 in a T-bill that pays 0.05 and a risky portfolio, P, constructed with two risky securities, X and Y.The weights of X and Y in P are 0.60 and 0.40, respectively.X has an expected rate of return of 0.14 and variance of 0.01, and Y has an expected rate of return of 0.10 and a variance of 0.0081. What would be the dollar value of your positions in X, Y, and the T-bills, respectively, if you decide to hold a portfolio that has an expected outcome of $1,120

Free

(Multiple Choice)

4.8/5 (39)

Correct Answer:Verified

B

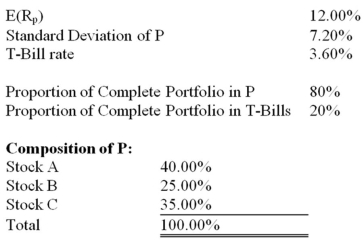

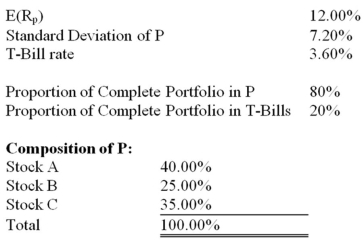

Your client, Bo Regard, holds a complete portfolio that consists of a portfolio of risky assets (P) and T-Bills.The information below refers to these assets.  What are the proportions of stocks A, B, and C, respectively, in Bo's complete portfolio

What are the proportions of stocks A, B, and C, respectively, in Bo's complete portfolio

Free

(Multiple Choice)

4.9/5 (30)

Correct Answer:Verified

C

You invest $100 in a risky asset with an expected rate of return of 0.11 and a standard deviation of 0.21 and a T-bill with a rate of return of 0.045. What percentages of your money must be invested in the risky asset and the risk-free asset, respectively, to form a portfolio with an expected return of 0.13

(Multiple Choice)

4.9/5 (45)

The change from a straight to a kinked capital allocation line is a result of

(Multiple Choice)

4.8/5 (33)

Which of the following statements is(are) true

I. Risk-averse investors reject investments that are fair games.

II. Risk-neutral investors judge risky investments only by the expected returns.

III. Risk-averse investors judge investments only by their riskiness.

IV. Risk-loving investors will not engage in fair games.

(Multiple Choice)

4.8/5 (35)

An investor invests 35% of his wealth in a risky asset with an expected rate of return of 0.18 and a variance of 0.10 and 65% in a T-bill that pays 4%.His portfolio's expected return and standard deviation are __________ and __________, respectively.

(Multiple Choice)

4.8/5 (25)

What is a fair game

Explain how the term relates to a risk-averse investor's attitude toward speculation and risk and how the utility function reflects this attitude.

(Essay)

4.7/5 (34)

To build an indifference curve we can first find the utility of a portfolio with 100% in the risk-free asset, then

(Multiple Choice)

4.8/5 (33)

You invest $1,000 in a risky asset with an expected rate of return of 0.17 and a standard deviation of 0.40 and a T-bill with a rate of return of 0.04. What percentages of your money must be invested in the risk-free asset and the risky asset, respectively, to form a portfolio with a standard deviation of 0.20

(Multiple Choice)

4.9/5 (34)

You invest $100 in a risky asset with an expected rate of return of 0.11 and a standard deviation of 0.20 and a T-bill with a rate of return of 0.03. What percentages of your money must be invested in the risky asset and the risk-free asset, respectively, to form a portfolio with an expected return of 0.08

(Multiple Choice)

4.8/5 (41)

Which of the following statements regarding risk-averse investors is true

(Multiple Choice)

4.9/5 (37)

In the mean-standard deviation graph an indifference curve has a ________ slope.

(Multiple Choice)

5.0/5 (38)

Draw graphs that represent indifference curves for the following investors: Harry, who is a risk-averse investor; Eddie, who is a risk-neutral investor; and Ozzie, who is a risk-loving investor.Discuss the nature of each curve and the reasons for its shape.

(Essay)

4.8/5 (40)

You invest $100 in a risky asset with an expected rate of return of 0.11 and a standard deviation of 0.20 and a T-bill with a rate of return of 0.03. The slope of the capital allocation line formed with the risky asset and the risk-free asset is equal to

(Multiple Choice)

4.9/5 (38)

Your client, Bo Regard, holds a complete portfolio that consists of a portfolio of risky assets (P) and T-Bills.The information below refers to these assets.  What is the expected return on Bo's complete portfolio

What is the expected return on Bo's complete portfolio

(Multiple Choice)

4.9/5 (37)

Consider a T-bill with a rate of return of 5% and the following risky securities:

Security A: E(r) = 0.15; Variance = 0.04

Security B: E(r) = 0.10; Variance = 0.0225

Security C: E(r) = 0.12; Variance = 0.01

Security D: E(r) = 0.13; Variance = 0.0625

From which set of portfolios, formed with the T-bill and any one of the four risky securities, would a risk-averse investor always choose his portfolio

(Multiple Choice)

5.0/5 (32)

In the utility function: U = E(r) - [-0.005As2], what is the significance of "A"

A.

A.This variable, as such, is not presented in most investments texts and it is important that the student understands how the investment advisor assigns a value to

(Essay)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)