Exam 5: Interest Rate Risk Measurement: The Repricing Model

Exam 1: Why Are Financial Institutions Special67 Questions

Exam 2: The Financial Services Industry: Depository Institutions66 Questions

Exam 3: The Financial Services Industry: Other Financial Institutions56 Questions

Exam 4: Risk of Financial Institutions67 Questions

Exam 5: Interest Rate Risk Measurement: The Repricing Model69 Questions

Exam 6: Interest Rate Risk Measurement: the Duration Model65 Questions

Exam 7: Managing Interest Rate Risk Using Off Balance Sheet Instruments62 Questions

Exam 8: Credit Risk I: Individual Loan Risk65 Questions

Exam 9: Market Risk55 Questions

Exam 10: Credit Risk I: Individual Loan Risk65 Questions

Exam 11: Credit Risk II: Loan Portfolio and Concentration Risk50 Questions

Exam 12: Sovereign Risk65 Questions

Exam 13: Foreign Exchange Risk64 Questions

Exam 14: Liquidity Risk64 Questions

Exam 15: Liability and Liquidity Management65 Questions

Exam 16: Off-Balance-Sheet Activities65 Questions

Exam 17: Technology and Other Operational Risk67 Questions

Exam 18: Capital Management and Adequacy66 Questions

Select questions type

When repricing all interest sensitive assets and all interest sensitive liabilities in a balance sheet, the cumulative gap will be:

(Multiple Choice)

4.9/5  (29)

(29)

An FI with a neutral repricing gap in its three to six month bucket is hedged against any interest rate changes at all points in time.

(True/False)

4.9/5 (37)

How do you interpret the position of an FI with a negative on-balance-sheet gap and a positive off-balance-sheet gap?

(Multiple Choice)

5.0/5 (41)

The Reserve Bank of Australia's (RBA) monetary policy can reduce an FI's interest rate risk:

(Multiple Choice)

5.0/5 (29)

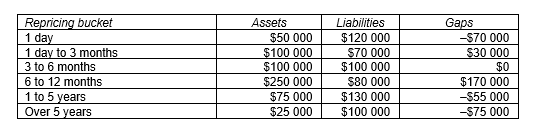

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is an increase of 100 basis points?

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is an increase of 100 basis points?

(Multiple Choice)

4.9/5 (37)

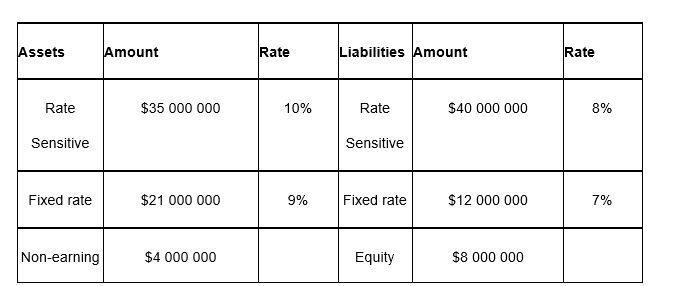

Consider the following information to answer the question:  What will be the FI's net interest income at year-end if interest rates do not change?

What will be the FI's net interest income at year-end if interest rates do not change?

(Multiple Choice)

4.8/5 (36)

An FI with a negative gap of $20 million suffers a $0.2 million decrease in its net interest income if interest rates decrease by 1 per cent.

(True/False)

4.8/5 (40)

Convexity is the major problem associated with the repricing gap.

(True/False)

4.8/5 (40)

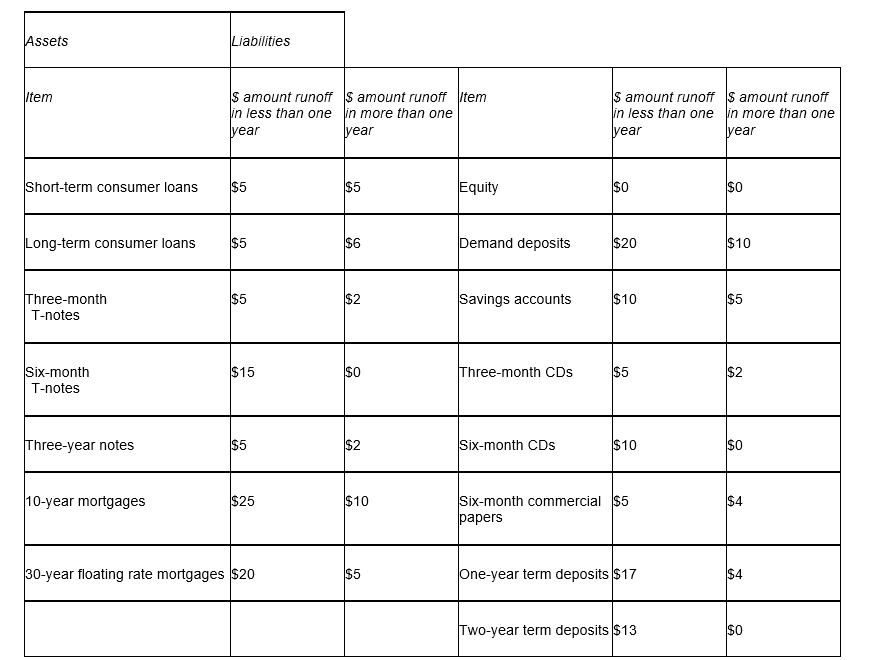

Consider the following table:  How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income ?

How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income ?

(Multiple Choice)

4.9/5 (29)

The unbiased expectations theory of the term structure of interest rates:

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)