Exam 5: Interest Rate Risk Measurement: The Repricing Model

Exam 1: Why Are Financial Institutions Special67 Questions

Exam 2: The Financial Services Industry: Depository Institutions66 Questions

Exam 3: The Financial Services Industry: Other Financial Institutions56 Questions

Exam 4: Risk of Financial Institutions67 Questions

Exam 5: Interest Rate Risk Measurement: The Repricing Model69 Questions

Exam 6: Interest Rate Risk Measurement: the Duration Model65 Questions

Exam 7: Managing Interest Rate Risk Using Off Balance Sheet Instruments62 Questions

Exam 8: Credit Risk I: Individual Loan Risk65 Questions

Exam 9: Market Risk55 Questions

Exam 10: Credit Risk I: Individual Loan Risk65 Questions

Exam 11: Credit Risk II: Loan Portfolio and Concentration Risk50 Questions

Exam 12: Sovereign Risk65 Questions

Exam 13: Foreign Exchange Risk64 Questions

Exam 14: Liquidity Risk64 Questions

Exam 15: Liability and Liquidity Management65 Questions

Exam 16: Off-Balance-Sheet Activities65 Questions

Exam 17: Technology and Other Operational Risk67 Questions

Exam 18: Capital Management and Adequacy66 Questions

Select questions type

Because the repricing model ignores the market value effect of changing interest rates, the repricing gap is an incomplete measure of the true interest rate risk exposure of an FI.

(True/False)

4.8/5  (33)

(33)

The repricing model ignores information regarding the distribution of assets and liabilities within maturity buckets. This limitation of the model refers to:

(Multiple Choice)

4.9/5 (34)

The Reserve Bank of Australia's (RBA) undertook actions in regards to their open market operation in the post global financial crisis environment to move financial markets towards greater stability. This was achieved by:

(Multiple Choice)

4.9/5 (34)

If the spread between rate sensitive assets and rate sensitive liabilities increases for a bank, future changes in interest rates will lead to an increase in net interest income.

(True/False)

4.9/5 (38)

Over-aggregation and runoffs are the major problems associated with the repricing gap.

(True/False)

4.8/5 (40)

What is meant by the 'run-off' problem and how can bank managers deal with this problem?

(Essay)

4.8/5 (34)

An FI with a positive gap of $30 million suffers a $0.15 million decrease in its net interest income if interest rates increase by 0.5 per cent.

(True/False)

4.7/5 (28)

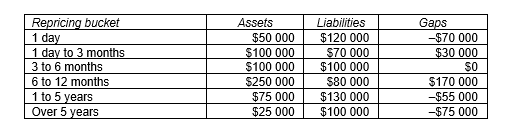

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?

(Multiple Choice)

4.9/5 (33)

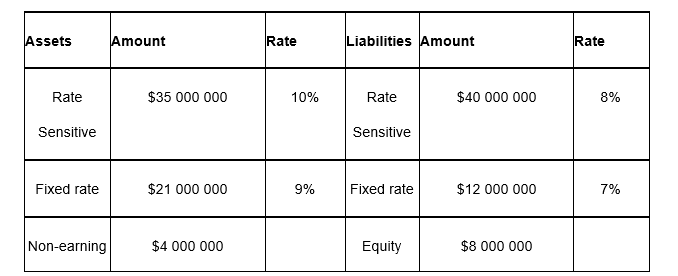

Consider the following information to answer the question:  What is the repricing gap for the FI?

What is the repricing gap for the FI?

(Multiple Choice)

4.8/5 (28)

Would you consider the repricing model to be a good and well-founded interest rate risk measurement and management tool? Why or why not?

(Essay)

4.8/5 (36)

How do you interpret the position of an FI with a positive on-balance-sheet gap and a negative off-balance sheet gap?

(Multiple Choice)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)