Exam 29: Property Transactions: Sec1231 and Recapture

Exam 1: Tax Research114 Questions

Exam 2: Corporate Formations and Capital Structure123 Questions

Exam 3: the Corporate Income Tax127 Questions

Exam 4: Corporate Nonliquidating Distributions113 Questions

Exam 5: Other Corporate Tax Levies103 Questions

Exam 6: Corporate Liquidating Distributions107 Questions

Exam 7: Corporate Acquisitions and Reorganizations108 Questions

Exam 8: Consolidated Tax Returns104 Questions

Exam 9: Partnership Formation and Operation116 Questions

Exam 10: Special Partnership Issues107 Questions

Exam 11: S Corporations103 Questions

Exam 12: The Gift Tax105 Questions

Exam 13: The Estate Tax107 Questions

Exam 14: Income Taxation of Trusts and Estates105 Questions

Exam 15: Administrative Procedures104 Questions

Exam 16: Ustaxation of Foreign-Related Transactions97 Questions

Exam 17: An Introduction to Taxation109 Questions

Exam 18: Determination of Tax152 Questions

Exam 19: Gross Income: Inclusions144 Questions

Exam 20: Gross Income: Exclusions116 Questions

Exam 21: Property Transactions: Capital Gains and Losses147 Questions

Exam 22: Deductions and Losses146 Questions

Exam 23: Itemized Deductions130 Questions

Exam 24: Losses and Bad Debts125 Questions

Exam 25: Employee Expenses and Deferred Compensation151 Questions

Exam 26: Depreciation, cost Recovery, amortization, and Depletion106 Questions

Exam 27: Accounting Periods and Methods124 Questions

Exam 28: Property Transactions: Nontaxable Exchanges125 Questions

Exam 29: Property Transactions: Sec1231 and Recapture115 Questions

Exam 30: Special Tax Computation Methods, tax Credits, and Payment of Tax147 Questions

Exam 31: Tax Research133 Questions

Exam 32: Corporations149 Questions

Exam 33: Partnerships and S Corporations150 Questions

Exam 34: Taxes and Investment Planning84 Questions

Select questions type

Installment sales of depreciable property which result in recaptured income under Secs.1245 or 1250 require that the recaptured income be recognized in the year of sale.

(True/False)

4.9/5  (38)

(38)

If the recognized losses resulting from involuntary conversions arising from casualty or theft exceed the recognized gains from such events (i.e.a net loss from the casualty),all of the involuntary conversions are treated as ordinary gains and losses.

(True/False)

5.0/5 (35)

In 2017,Thomas,who has a marginal tax rate of 15%,sells land that is Sec.1231 property at a gain of $4,000.If he has no other 1231 transactions or capital asset transactions and has no nonrecaptured 1231 gain,Thomas will pay no tax on the $4,000 gain.

(True/False)

4.8/5 (39)

Sec.1245 applies to gains on the sale of depreciable personal property,but it generally does not apply to depreciable real property.

(True/False)

4.8/5 (36)

Yelenis,whose tax rate is 28%,sells one Sec.1231 asset this year,resulting in a $50,000 gain.Included in the $50,000 Sec.1231 gain is $30,000 of unrecaptured Sec.1250 gain.A review of Yelenis tax files for the past five years indicates one prior Sec.1231 sale which resulted in a $14,000 loss.The gain will be taxed as

(Multiple Choice)

4.9/5 (39)

Gains and losses from involuntary conversions of property used in a trade or business generally are classified as capital gains and losses.

(True/False)

4.9/5 (37)

Dinah owned land with a FMV of $130,000 (adjusted basis $120,000)which is investment property (a capital asset).Dinah owned a second tract of land,a 1231 asset,with a FMV of $46,000 (adjusted basis $50,000).Both tracts were acquired in 2001 and condemned by the state this year.The state paid an amount equal to FMV.If there are no other transactions involving capital assets or 1231 assets,Dinah must report on her current year return

(Multiple Choice)

4.9/5 (33)

Mark owns an unincorporated business and has $20,000 of Sec.1231 gains and $22,000 of Sec.1231 losses.He must report a net capital loss of $2,000 on his tax return.

(True/False)

4.9/5 (42)

Sec.1231 property must satisfy a holding period of more than one year.

(True/False)

4.8/5 (34)

The additional recapture under Sec.291 is 25% of the difference between the amount that would have been recaptured if the property was Sec.1245 property and the actual recapture under Sec.1250.

(True/False)

4.8/5 (39)

With regard to noncorporate taxpayers,all of the following statements are true regarding Sec.1250 recapture except

(Multiple Choice)

4.8/5 (34)

Maura makes a gift of a van to a local food bank run by a charity.Maura had used the van in her trade or business.The van has a FMV of $6,500; a cost of $31,000; and $27,000 depreciation claimed.What is the amount of Maura's charitable contribution deduction?

(Multiple Choice)

4.8/5 (31)

A taxpayer acquired new machinery costing $50,000 three years ago.The taxpayer had elected Sec.179 expensing to deduct the full cost in the year of acquisition.The taxpayer sells the machinery this year and realizes a $32,000 gain.Sec.1245 will not require any ordinary income recapture on the sale of this asset due to the Sec.179 expensing.

(True/False)

4.8/5 (29)

The amount recaptured as ordinary income under either Sec.1245 or Sec.1250 can never exceed the realized gain.

(True/False)

4.9/5 (41)

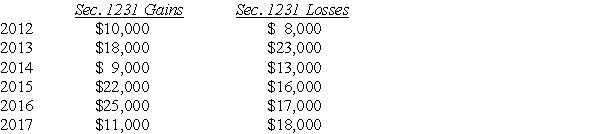

Lucy,a noncorporate taxpayer,experienced the following Sec.1231 gains and losses during the years 2012 through 2017.Her first disposition of a Sec.1231 asset occurred in 2012.Assuming Lucy had no capital gains and losses during that time period,what is the tax treatment in each of the years listed?

(Essay)

4.8/5 (31)

In 1980,Artima Corporation purchased an office building for $400,000 for use in its business.The building is sold during the current year for $550,000.Total depreciation allowed for the building was $390,000; straight-line would have been $360,000.As result of the sale,how much Sec.1231 gain will Artima Corporation report?

(Multiple Choice)

4.8/5 (38)

Daniel recognizes $35,000 of Sec.1231 gains and $25,000 of Sec.1231 losses during the current year.The only other Sec.1231 item was a $4,000 loss three years ago.This year,Daniel must report

(Multiple Choice)

4.8/5 (36)

Any gain or loss resulting from the sale or disposition of depreciable property used in trade or business and held one year or less is considered ordinary.

(True/False)

4.8/5 (38)

The following gains and losses pertain to Arnold's business assets that qualify as Sec.1231 property.Arnold does not have any nonrecaptured net Sec.1231 losses from previous years,and the portion of gain recaptured as ordinary income due to the depreciation recapture provisions has been eliminated.

Describe the specific tax treatment of each of these transactions.

Describe the specific tax treatment of each of these transactions.

(Essay)

4.8/5 (41)

Brian purchased some equipment in 2017 which he intends to use in his trade or business.He approaches you to assist him in planning for the ultimate disposal of the asset-whether it be by sale,charitable contribution to the local university,gift to his sister for use in her business,or some other means.Discuss the tax considerations.

(Essay)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)