Exam 17: The Statement of Comprehensive Income and Statement of Changes in E

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

Total comprehensive income for the year is profit for the year plus comprehensive income.

Free

(True/False)

4.9/5  (37)

(37)

Correct Answer: Verified

Verified

True

Profit is not defined in the AASB Framework:

Free

(Multiple Choice)

4.8/5 (36)

Correct Answer:Verified

A

AASB 101 requires profit or loss and the total comprehensive income for the period reported on the face of the statement of comprehensive income to be disaggregated between the non-controlling interest and the owners of the parent.

(True/False)

4.9/5 (42)

AASB 2 requires that the fair value of the option issued as a share-based payment to an employee,be determined and this value be deemed to be the cost of the options:

(True/False)

4.9/5 (31)

According to AASB 101,the income statement provides a total profit figure to which opening retained earnings is added and from which dividends are deducteD.

(True/False)

4.8/5 (37)

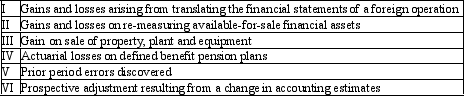

Following are the items of income and expense recognised during the period by Gordon Field LtD.  Which of the following combinations identify all items permitted in AASB 101 "Presentation of Financial Statements" to be presented under other comprehensive income?

Which of the following combinations identify all items permitted in AASB 101 "Presentation of Financial Statements" to be presented under other comprehensive income?

(Multiple Choice)

4.9/5 (32)

Which of the following statements is not in accordance with AASB 101 "Presentation of Financial Statements" with respect to the statement of comprehensive income?

(Multiple Choice)

4.9/5 (39)

Discovery of an error from a prior period corrected retrospectively is an example of an item reportable under other comprehensive income.

(True/False)

4.7/5 (39)

An income statement that includes the following items: Revenue

Other Income

Employee Benefits and Costs

Motor Vehicle Expenses

Would have been prepared using the:

(Multiple Choice)

4.8/5 (46)

Which of the following items does not give rise to a reclassification adjustment from components of other comprehensive income to profit and loss?

(Multiple Choice)

4.8/5 (46)

Government departments are now required to report in accordance with AAS 29 'Financial reporting by government departments'.The broad effect of the requirements of this standard is to:

(Multiple Choice)

4.8/5 (41)

All expenses from operating activities must be classified according to either their nature or function:

(True/False)

4.9/5 (41)

Comprehensive income includes dividend payments to shareholders.

(True/False)

4.9/5 (38)

Profit is calculated as the difference between income and expenses as defined by the AASB Framework.As a result:

(Multiple Choice)

4.8/5 (37)

The problem with a "blanket rule" requiring all expenditure of a particular type to be written off as incurred (e.g.,expenditure on research),is:

(Multiple Choice)

4.8/5 (36)

AASB 118 'Revenue' requires a number of disclosures,including information about:

(Multiple Choice)

4.9/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)