Exam 12: Set-Off and Extinguishment of Debt

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

Pump It Up Ltd owes Under Ground Oil $170 000 and Under Ground Oil owes Pump It Up Ltd $350 000.Pump It Up Ltd's financial position before these amounts are set-off is:  What is the debt/equity ratio for Pump It Up Ltd before and after set-off?

What is the debt/equity ratio for Pump It Up Ltd before and after set-off?

Free

(Multiple Choice)

4.9/5  (33)

(33)

Correct Answer: Verified

Verified

A

In AASB 132,the ability to set off makes reference to:

Free

(Multiple Choice)

4.7/5 (38)

Correct Answer:Verified

B

When a debt is forgiven the accounting treatment is to:

Free

(Multiple Choice)

4.9/5 (41)

Correct Answer:Verified

B

What is the AASB 132 requirement in relation to debt set-off?

(Multiple Choice)

4.7/5 (34)

Insubstance debt defeasance refers to an arrangement where assets are placed in trust,meaning that the creditor has now been paid in full:

(True/False)

4.8/5 (40)

Businesses may be prepared to incur a loss on the defeasance of debt because:

(Multiple Choice)

4.7/5 (39)

In relation to applying an amount due from a third party in a "set-off" situation,AASB 132 notes:

(Multiple Choice)

4.7/5 (46)

If the conditions for set off were initially met,and in a later period cease to be met,the debt remaining is to be:

(Multiple Choice)

4.9/5 (38)

AASB 132 only allows assets and liabilities to be offset against one another if a legally recognised right to set-off exists for these items:

(True/False)

4.8/5 (31)

AASB 132 "Financial Instruments: Presentation" supports a substance over from approach in the accounting treatment for Insubstance Debt Defeasance (ISDD).

(True/False)

4.9/5 (40)

The term defeasance means the setting off of one thing against another:

(True/False)

4.8/5 (42)

Release from the primary obligation of a debt may theoretically be achieved by:

(Multiple Choice)

4.7/5 (30)

Cartoons and Co's balance sheet is shown below.  Assuming a right to set-off exist with Ink Drawings Ltd,the balance sheet after set-off will be:

Assuming a right to set-off exist with Ink Drawings Ltd,the balance sheet after set-off will be:

(Multiple Choice)

4.9/5 (36)

Release from the primary obligation for a debt may be achieved by replacement by another debt:

(True/False)

4.7/5 (37)

A right of set-off may still be applied in the case of Insubstance Debt Defeasance (ISDD)if the entity intends to settle on a net basis,or to realise the asset and settle the liability simultaneously.

(True/False)

4.8/5 (34)

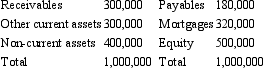

Claudia Ltd's statement of financial position is shown below.  The above balances include a receivable from Jeremy Ltd for an amount of $100,000 and a payable to Jeremy Ltd for $50,000.A debt contract with ABC Bank signed by Claudia Ltd requires a debt equity ratio of no more than 50%.

Assuming a right to set-off exists with Jeremy Ltd,what is the debt to equity ratio of Claudia Ltd?

The above balances include a receivable from Jeremy Ltd for an amount of $100,000 and a payable to Jeremy Ltd for $50,000.A debt contract with ABC Bank signed by Claudia Ltd requires a debt equity ratio of no more than 50%.

Assuming a right to set-off exists with Jeremy Ltd,what is the debt to equity ratio of Claudia Ltd?

(Multiple Choice)

4.7/5 (39)

The effect of setting off on the gearing ratio of the reporting entity is to:

(Multiple Choice)

4.8/5 (28)

The changes under AASB 132 have removed the need for creditors to be involved in the defeasance process:

(True/False)

4.9/5 (27)

The definition of a set-off is that an asset is reduced by the amount of a liability and a net liability remains:

(True/False)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)