Exam 28: Accounting for Group Structures

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

'Control' exists when the parent owns less than half of the voting power of an entity when:

Free

(Multiple Choice)

4.9/5  (39)

(39)

Correct Answer: Verified

Verified

D

Which of the following statements is not correct?

Free

(Multiple Choice)

4.9/5 (43)

Correct Answer:Verified

D

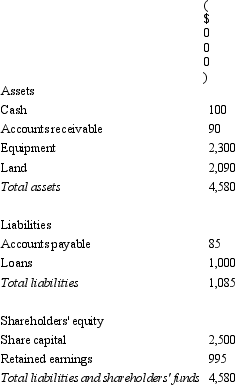

Banderas Ltd acquires all the issued capital of Ryan Ltd for a cash payment of $2,900,000 on 30 June 2004.The balance sheet of Ryan Ltd at purchase date is:  Assuming the assets are at fair value,what is the consolidation entry to eliminate the investment in Ryan Ltd?

Assuming the assets are at fair value,what is the consolidation entry to eliminate the investment in Ryan Ltd?

(Multiple Choice)

4.7/5 (34)

Which of the following statements is not in accordance with AASB 3 "Business Combinations"?

(Multiple Choice)

4.7/5 (35)

In the consolidated financial statements of the parent entity and its controlled entities only transactions with assets and liabilities relating to parties external to the economic entity will be reflected.

(True/False)

4.8/5 (37)

AASB 127 requires the parent company to have control of another entity in order for that entity's consolidation into the group accounts to be required.

(True/False)

4.9/5 (39)

A consolidated entity is defined in the Corporations Act 2001 as:

(Multiple Choice)

4.7/5 (41)

Goodwill arises at acquisition date when the purchase price exceeds the identifiable assets acquired and the liabilities assumed.

(True/False)

4.8/5 (31)

It is possible for one entity to control another entity under the AASB 3 definition without the controlling entity having any equity-ownership interest in the other entity:

(True/False)

4.8/5 (38)

A company may own more than 50 per cent of the capital of another entity and not have effective control of that entity as defined in AASB 3:

(True/False)

4.9/5 (30)

The factors that are taken into consideration in determining whether or not an entity should be consolidated under AASB 127 include:

(Multiple Choice)

4.8/5 (35)

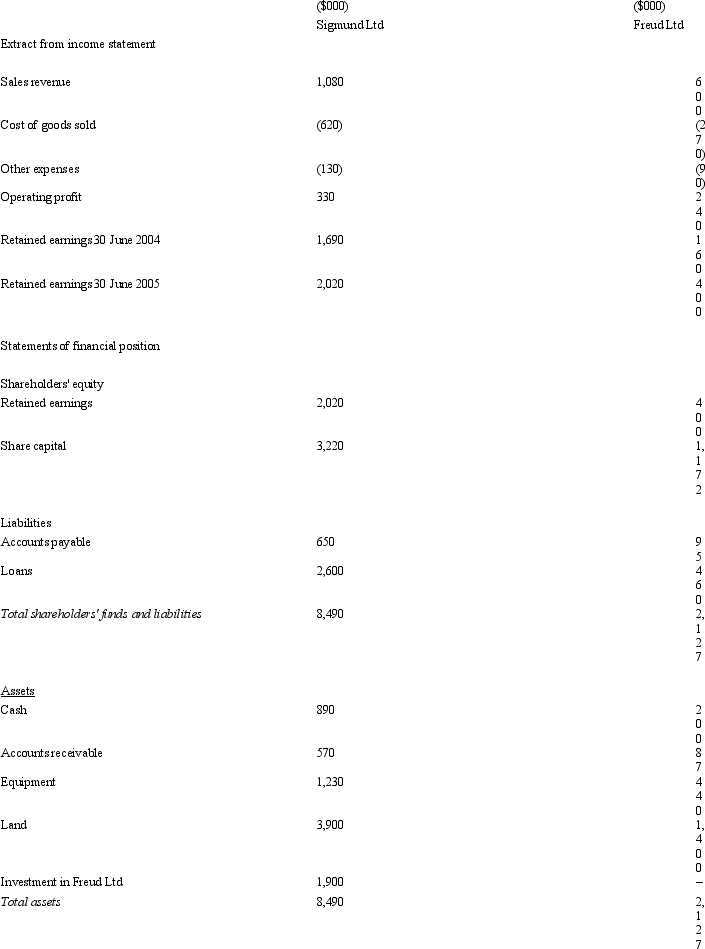

Sigmund Ltd acquires all the issued capital of Freud Ltd for a cash payment of $1,900,000 on 30 June 2004.The financial statements of both entities on 30 June 2005 are:  The fair value of the net tangible assets of Freud Ltd on 30 June 2004 was $1,332,000.The equity of Freud at that time was made up of share capital of $1,172,000 and retained earnings of $160,000.Goodwill had been determined to have been impaired by $56,800 during the period.During the period ended 30 June 2005 there were no intragroup transactions.Which of the following consolidated financial statements is correct?

The fair value of the net tangible assets of Freud Ltd on 30 June 2004 was $1,332,000.The equity of Freud at that time was made up of share capital of $1,172,000 and retained earnings of $160,000.Goodwill had been determined to have been impaired by $56,800 during the period.During the period ended 30 June 2005 there were no intragroup transactions.Which of the following consolidated financial statements is correct?

(Multiple Choice)

4.7/5 (34)

Where separate entities in a group do not apply the same accounting methods,AASB 127 "Consolidated and Separate Financial Statements" prescribes adjustments to be made on consolidation to remove the impacts of different accounting policies.

(True/False)

4.7/5 (35)

The consolidation concept adopted in AASB 127 is to include all the assets and liabilities of the parent entity and subsidiaries in the consolidation and to treat minority interests as part of the equity of the group:

(True/False)

4.7/5 (31)

Where the controlled entity's non-current assets were not at fair value at the date of purchase and they have not been revalued in the controlled entity's accounts,the treatment in the consolidation entry may include which of the following entries?

(Multiple Choice)

4.8/5 (33)

After initial recognition,goodwill is measured in which of the following ways?

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)