Exam 11: Partnerships: Distributions, transfer of Interests, and Terminations

Exam 1: Understanding and Working With the Federal Tax Law72 Questions

Exam 2: Corporations: Introduction and Operating Rules103 Questions

Exam 3: Corporations: Special Situations76 Questions

Exam 4: Corporations: Organization and Capital Structure91 Questions

Exam 5: Corporations: Earnings and Profits and Dividend Distributions82 Questions

Exam 6: Corporations: Redemptions and Liquidations107 Questions

Exam 7: Corporations: Reorganizations138 Questions

Exam 8: Consolidated Tax Returns143 Questions

Exam 9: Taxation of International Transactions142 Questions

Exam 10: Partnerships: Formation, operation, and Basis71 Questions

Exam 11: Partnerships: Distributions, transfer of Interests, and Terminations84 Questions

Exam 12: S Corporations161 Questions

Exam 13: Comparative Forms of Doing Business139 Questions

Exam 14: Exempt Entities159 Questions

Exam 15: Multistate Corporate Taxation169 Questions

Exam 16: Tax Practice and Ethics147 Questions

Exam 17: The Federal Gift and Estate Taxes199 Questions

Exam 18: Family Tax Planning168 Questions

Exam 19: Income Taxation of Trusts and Estates155 Questions

Select questions type

Match the following independent distribution payments in liquidation of a partner's interest in an ongoing partnership with the statements below.

a.A payment for the partner's share of partnership income under § 736(a).

b.A payment for the partner's share of partnership property under § 736(b).

c.The payment includes both a § 736(a) and a § 736(b) element.

-Land held by the partnership for investment purposes.

(Short Answer)

4.9/5  (47)

(47)

A payment to a retiring partner for his or her share of goodwill of a partnership in which capital is a material income-producing factor is classified as a § 736(a)income payment and results in ordinary income to the retiring partner and a current deduction to the partnership.

(True/False)

4.8/5 (33)

Barney,Bob,and Billie are equal partners in the BBB Partnership.The partnership balance sheet reads as follows on December 31 of the current year:

Partner Billie has an adjusted basis of $40,000 for her partnership interest.If Billie sells her entire partnership interest to new partner Janet for $60,000 cash,how much capital gain and ordinary income must Billie recognize from the sale?

Partner Billie has an adjusted basis of $40,000 for her partnership interest.If Billie sells her entire partnership interest to new partner Janet for $60,000 cash,how much capital gain and ordinary income must Billie recognize from the sale?

(Multiple Choice)

4.9/5 (43)

A limited liability company generally provides limited liability for those owners that are not active in the management of the LLC but requires owner-managers of the LLC to have unlimited personal liability for LLC debts.

(True/False)

4.9/5 (37)

Rex and Scott operate a law practice in partnership form.Since Rex and Scott are brothers,the partnership is subject to the family partnership income reallocation rules.

(True/False)

4.7/5 (39)

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

-Section 754

(Short Answer)

4.9/5 (36)

The JIH Partnership distributed the following assets to partner James in a proportionate liquidating distribution in which the partnership also liquidated: $25,000 cash,land parcel A (basis of $5,000,value of $30,000),and land parcel B (basis of $5,000,value of $15,000).James's basis in his partnership interest was $85,000 immediately before the distribution.James will allocate bases of $40,000 to parcel A and $20,000 to parcel B,and he will have no remaining basis in his partnership interest.

(True/False)

4.8/5 (44)

Your client has operated a sole proprietorship for several years,and is now interested in raising capital for expansion.He is considering forming either a C corporation or an LLC.

a.Describe the treatment of an LLC and discuss any advantages the LLC offers over the C corporation.

b.Assume instead the client has previously operated as a C corporation. Describe the tax consequences of converting to an LLC.

(Essay)

4.7/5 (36)

Match the following independent distribution payments in liquidation of a partner's interest in an ongoing partnership with the statements below.

a.A payment for the partner's share of partnership income under § 736(a).

b.A payment for the partner's share of partnership property under § 736(b).

c.The payment includes both a § 736(a) and a § 736(b) element.

-Inventory with a basis of $10,000 and a fair market value of $10,500.

(Short Answer)

4.8/5 (39)

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

-Ordering rules

(Short Answer)

4.9/5 (36)

Carl receives a proportionate nonliquidating distribution when the basis of his partnership interest is $60,000.The distribution consists of $20,000 in cash and property with an adjusted basis to the partnership of $35,000 and a fair market value of $45,000.Carl's basis in the noncash property and his remaining basis in the partnership interest are:

(Multiple Choice)

4.8/5 (40)

A § 754 election is made for a tax year in which the partner recognizes gain or loss on a distribution from the partnership or the basis in distributed property is increased or decreased from the inside basis the partnership held in those assets.The election is made by a partner any time it is necessary to adjust his or her share of the inside basis of partnership assets.

(True/False)

4.8/5 (31)

The Crimson Partnership is a service provider.Its assets consist of unrealized receivables (basis $0,value $200,000),cash of $200,000,and land (basis of $280,000,value of $400,000).Assume 25% general partner Jill has a basis in her partnership interest of $130,000.If the ongoing partnership distributes the $200,000 cash to Jill in liquidation of her interest in the partnership,she will recognize ordinary income of $50,000 and a capital gain of $20,000.

(True/False)

4.7/5 (31)

Terry received a proportionate share of partnership inventory in complete liquidation of her partnership interest.If Terry holds the distributed property as a capital asset for six years and sells it for a gain,the gain is taxed as a long-term capital gain.

(True/False)

4.8/5 (36)

The RBD Partnership balance sheet on August 31 of the current year is as follows:

On that date,Rachel sells her one-third partnership interest to Bill for $300,000,including cash and relief of Rachel's share of the nonrecourse debt.The nonrecourse debt is shared equally among the partners.Rachel's outside basis for her partnership interest is $250,000.How much capital gain and/or ordinary income will Rachel recognize on the sale?

On that date,Rachel sells her one-third partnership interest to Bill for $300,000,including cash and relief of Rachel's share of the nonrecourse debt.The nonrecourse debt is shared equally among the partners.Rachel's outside basis for her partnership interest is $250,000.How much capital gain and/or ordinary income will Rachel recognize on the sale?

(Multiple Choice)

4.7/5 (50)

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

-Technical termination

(Short Answer)

4.9/5 (40)

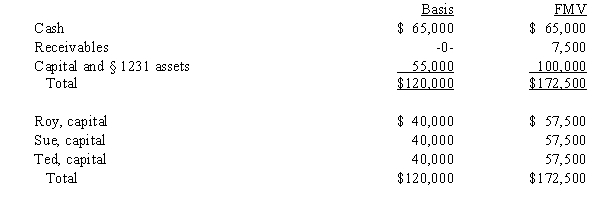

The December 31,2008,balance sheet of the RST General Partnership reads as follows.

The partners share equally in partnership capital,income,gain,loss,deduction and credit.Ted's adjusted basis for his partnership interest is $40,000.On December 31,2008,he retires from the partnership,receiving a $60,000 cash payment in liquidation of his interest.The partnership agreement states that $2,500 of the payment is for goodwill.Which of the following statements about this distribution is false?

The partners share equally in partnership capital,income,gain,loss,deduction and credit.Ted's adjusted basis for his partnership interest is $40,000.On December 31,2008,he retires from the partnership,receiving a $60,000 cash payment in liquidation of his interest.The partnership agreement states that $2,500 of the payment is for goodwill.Which of the following statements about this distribution is false?

(Multiple Choice)

4.7/5 (35)

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

-Limited partner

(Short Answer)

4.8/5 (33)

Matt,a partner in the MB Partnership,receives a proportionate,nonliquidating distribution of property having a fair market value of $16,000 and a partnership basis of $23,000.Matt's basis in the partnership is $10,000 before the distribution.In this situation,Matt will take a $10,000 basis in the property,and his basis in the partnership interest is reduced to zero.

(True/False)

4.7/5 (34)

Suzy owns a 25% capital and profits interest in the calendar-year SJDV Partnership.Her adjusted basis for her partnership interest on July 1 of the current year is $200,000.On that date,she receives a proportionate nonliquidating current distribution of the following assets:

a.Calculate Suzy's recognized gain or loss on the distribution, if any.

b.Calculate Suzy's basis in the inventory received.

c.Calculate Suzy's basis in land received. The land is a capital asset.

d.Calculate Suzy's basis for her partnership interest after the distribution.

a.Calculate Suzy's recognized gain or loss on the distribution, if any.

b.Calculate Suzy's basis in the inventory received.

c.Calculate Suzy's basis in land received. The land is a capital asset.

d.Calculate Suzy's basis for her partnership interest after the distribution.

(Essay)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)