Exam 13: Comparative Forms of Doing Business

Exam 1: Understanding and Working With the Federal Tax Law72 Questions

Exam 2: Corporations: Introduction and Operating Rules103 Questions

Exam 3: Corporations: Special Situations76 Questions

Exam 4: Corporations: Organization and Capital Structure91 Questions

Exam 5: Corporations: Earnings and Profits and Dividend Distributions82 Questions

Exam 6: Corporations: Redemptions and Liquidations107 Questions

Exam 7: Corporations: Reorganizations138 Questions

Exam 8: Consolidated Tax Returns143 Questions

Exam 9: Taxation of International Transactions142 Questions

Exam 10: Partnerships: Formation, operation, and Basis71 Questions

Exam 11: Partnerships: Distributions, transfer of Interests, and Terminations84 Questions

Exam 12: S Corporations161 Questions

Exam 13: Comparative Forms of Doing Business139 Questions

Exam 14: Exempt Entities159 Questions

Exam 15: Multistate Corporate Taxation169 Questions

Exam 16: Tax Practice and Ethics147 Questions

Exam 17: The Federal Gift and Estate Taxes199 Questions

Exam 18: Family Tax Planning168 Questions

Exam 19: Income Taxation of Trusts and Estates155 Questions

Select questions type

Limited partnerships have a greater potential for raising capital than do general partnerships.

(True/False)

4.9/5  (35)

(35)

The accumulated earnings tax rate in 2008 is the same as that for a C corporation that is classified as a personal holding company.

(True/False)

4.8/5 (38)

The special allocation opportunities that are available to partnerships are not available to S corporations.

(True/False)

4.8/5 (37)

Gus is the general partner and Laura is the limited partner of GL Limited Partnership. Gus contributes $500,000 cash and Laura contributes a building with a fair market value of $600,000 (adjusted basis of $125,000)to the partnership.Gus and Laura share equally in partnership profits and losses.In 2008,the first year in business,GL obtains nonrecourse financing of $200,000 to cover operating expenses and incurs a $1,200,000 loss.How much loss may be passed through to Gus and Laura?

(Multiple Choice)

4.9/5 (34)

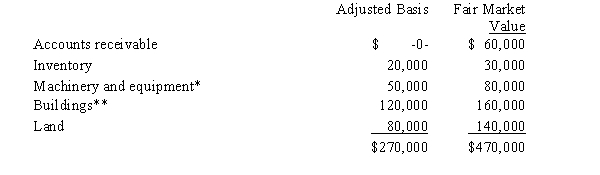

Mr.and Ms.Smith's partnership owns the following assets:

* Potential § 1245 recapture of $30,000.

** Straight-line depreciation was used.

mr.and Ms.Smith each have a basis for their partnership interest of $135,000. Calculate their combined recognized gain or loss and classify it as capital or ordinary if they sell their partnership interests for $470,000.

** Straight-line depreciation was used.

mr.and Ms.Smith each have a basis for their partnership interest of $135,000. Calculate their combined recognized gain or loss and classify it as capital or ordinary if they sell their partnership interests for $470,000.

(Multiple Choice)

4.8/5 (34)

Kirk is establishing a business in 2008 which could have potential environmental liability problems.Therefore,he is trying to decide between the C corporation form and the S corporation form.He projects that the business will generate losses of approximately $100,000 each year for the first 3 years and then will generate profits of at least $200,000 each year thereafter.All profits will be reinvested in the growth of the business.Kirk projects he will be in the 35% bracket in 2008 and thereafter.Advise Kirk on which tax form he should select.

(Essay)

4.9/5 (42)

Kristine owns all of the stock of a C corporation which owns the following assets:

* Potential § 1245 recapture of $30,000.

** Straight-line depreciation was used.

Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $470,000.

* Potential § 1245 recapture of $30,000.

** Straight-line depreciation was used.

Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $470,000.

(Multiple Choice)

4.8/5 (34)

Nevada is the only state that does not permit the limited liability company (LLC)form of ownership.

(True/False)

4.8/5 (36)

Ashley contributes property to the TCA Partnership which was formed 7 years ago by Clark and Tara.Ashley's basis for the property is $70,000 and the fair market value is $150,000.Ashley receives a 25% interest for his contribution.Because the TCA Partnership is unsuccessful in having the property rezoned from agricultural to commercial,it sells the property 12 months later for $210,000.

a.Determine the tax consequences to Ashley and to the partnership on the contribution of the property to the partnership.

b.Determine the tax consequences to Ashley and the other partners on the sale of the property.

b. differ if the entity were an S corporation?

c.Would the tax consequences in

(Essay)

4.9/5 (39)

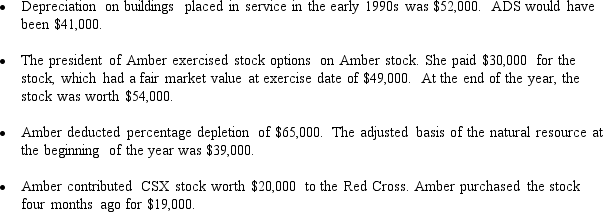

Amber,Inc.,has taxable income of $212,000.In addition,Amber accumulates the following information which may affect its AMT.

What is Amber's AMTI?

What is Amber's AMTI?

(Multiple Choice)

4.8/5 (35)

Discuss the tax consequences to the corporation and to the shareholder/employee of having part of the shareholder/employee's salary and bonus classified as being unreasonable.

(Essay)

5.0/5 (38)

If a taxpayer contributes an appreciated asset to a business entity and the realized gain is not recognized,there is a carryover basis for the taxpayer's ownership interest and a carryover basis to the entity for the asset.

(True/False)

4.9/5 (40)

Match the following statements:

a.Status applies only if elected by the taxpayer.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 20%.

d.Subject to double taxation.

e.Eligible for special allocations.

-C corporations.

(Short Answer)

5.0/5 (43)

A limited partner in a limited partnership has limited liability whereas a general partner in a limited partnership has unlimited liability unless the limited partners agree that the general partner will have limited liability.

(True/False)

4.8/5 (32)

Match the following statements:

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.Subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 subject to ordinary income potential under § 751.

e.Not subject to double taxation on the sale of corporate stock.

-Sale of corporate stock by the S corporation shareholders.

(Short Answer)

4.9/5 (37)

Parrot,Inc.,a C corporation,distributes $50,000 to its shareholder,Jerome,and land worth $50,000 (adjusted basis of $30,000)to its shareholder,Peggy.Parrot has earnings and profits of $300,000.Determine the tax consequences to Parrot,Jerome,and Peggy.

(Essay)

4.9/5 (42)

Match the following statements:

a.Status applies only if elected by the taxpayer.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 20%.

d.Subject to double taxation.

e.Eligible for special allocations.

-Technique for minimizing double taxation.

(Short Answer)

4.9/5 (47)

Kirby,the sole shareholder of Falcon,Inc.,leases a building to the corporation.The taxable income of the corporation for 2008,before deducting the lease payments,is projected to be $500,000.

a.What are the tax consequences to Kirby and to Falcon if Kirby leases a building to the corporation for $500,000?

b.Is there a potential pitfall? How would it change the tax consequences to Kirby and to Falcon?

(Essay)

4.9/5 (41)

Lee owns all the stock of Vireo,Inc.,a C corporation for which he has an adjusted basis of $150,000.The assets of Vireo,Inc.,are as follows:

Lee sells his stock to Katrina for $200,000.

a.Determine the tax consequences to Lee.

b.Determine the tax consequences to Katrina.

c.Determine the tax consequences to Vireo, Inc.

a.Determine the tax consequences to Lee.

b.Determine the tax consequences to Katrina.

c.Determine the tax consequences to Vireo, Inc.

(Essay)

4.8/5 (33)

Match the following:

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an 80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

-General partnership.

(Short Answer)

4.7/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)