Exam 8: Risk and Return

Exam 1: The Role of Managerial Finance133 Questions

Exam 2: The Financial Market Environment91 Questions

Exam 3: Financial Statements and Ratio Analysis209 Questions

Exam 4: Cash Flow and Financial Planning185 Questions

Exam 5: Time Value of Money173 Questions

Exam 6: Interest Rates and Bond Valuation224 Questions

Exam 7: Stock Valuation188 Questions

Exam 8: Risk and Return190 Questions

Exam 9: The Cost of Capital137 Questions

Exam 10: Capital Budgeting Techniques167 Questions

Exam 11: Capital Budgeting Cash Flows and Risk Refinements195 Questions

Exam 12: Leverage and Capital Structure217 Questions

Exam 13: Payout Policy130 Questions

Exam 14: Working Capital and Current Assets Management340 Questions

Exam 15: Current Liabilities Management171 Questions

Select questions type

The goal of an efficient portfolio is to

Free

(Multiple Choice)

4.9/5  (34)

(34)

Correct Answer: Verified

Verified

D

Nico wants to invest all of his money in just two assets: the risk free asset and the market portfolio. What is Nico's portfolio beta if he invests a quarter of his money in the market portfolio and the rest in the risk free asset?

Free

(Multiple Choice)

4.8/5 (30)

Correct Answer:Verified

B

Nondiversifiable risk reflects the contribution of an asset to the risk, or standard deviation, of the portfolio.

Free

(True/False)

4.8/5 (27)

Correct Answer:Verified

True

The capital asset pricing model (CAPM) links together unsystematic risk and return for all assets.

(True/False)

4.7/5 (39)

In general, widely accepted expectations of hard times ahead tend to cause investors to become less risk-averse.

(True/False)

4.7/5 (27)

In the capital asset pricing model, the beta coefficient is a measure of ________ risk and an index of the degree of movement of an asset's return in response to a change in ________.

(Multiple Choice)

4.8/5 (30)

The more certain the return from an asset, the less variability and therefore the less risk.

(True/False)

4.7/5 (32)

The ________ is a measure of relative dispersion used in comparing the risk of assets with differing expected returns.

(Multiple Choice)

4.9/5 (34)

The security market line (SML) reflects the required return in the marketplace for each level of nondiversifiable risk (beta).

(True/False)

4.8/5 (37)

A given change in inflationary expectations will be fully reflected in a corresponding change in the returns of all assets and will be reflected graphically in a parallel shift of the SML.

(True/False)

4.9/5 (44)

Nico bought 100 shares of Cisco Systems stock for $24.00 per share on January 1, 2002. He received a dividend of $2.00 per share at the end of 2002 and $3.00 per share at the end of 2003. At the end of 2004, Nico collected a dividend of $4.00 per share and sold his stock for $18.00 per share. What was Nico's realized holding period return? What was Nico's compound annual rate of return?

(Multiple Choice)

4.9/5 (41)

Greater risk aversion results in lower required returns for each level of risk, whereas a reduction in risk aversion would cause the required return for each level of risk to increase.

(True/False)

4.8/5 (29)

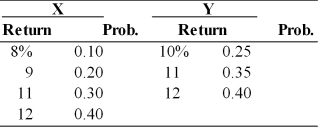

Given the following probability distribution for assets X and Y, compute the expected rate of return, variance, standard deviation, and coefficient of variation for the two assets. Which asset is a better investment?

(Essay)

4.8/5 (26)

Assume your firm produces a good which has high sales when the economy is expanding and low sales during a recession. This firm's overall risk will be higher if it invests in another product which is counter cyclical.

(True/False)

4.8/5 (29)

Diversifiable risk is the relevant portion of risk attributable to market factors that affect all firms.

(True/False)

4.8/5 (31)

Coefficient of variation is a measure of relative dispersion used in comparing the expected returns of assets with differing risks.

(True/False)

4.7/5 (31)

What is Nico's portfolio beta if he invests an equal amount in asset X with a beta of 0.60, asset Y with a beta of 1.60, the risk-free asset, and the market portfolio?

(Multiple Choice)

4.8/5 (30)

An investment banker has recommended a $100,000 portfolio containing assets B, D, and F. $20,000 will be invested in asset B, with a beta of 1.5; $50,000 will be invested in asset D, with a beta of 2.0; and $30,000 will be invested in asset F, with a beta of 0.5. The beta of the portfolio is

(Multiple Choice)

4.9/5 (39)

Event risk is the chance that a totally unexpected event will have a significant effect on the value of the firm or a specific investment.

(True/False)

4.7/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)